Westpac with the note.

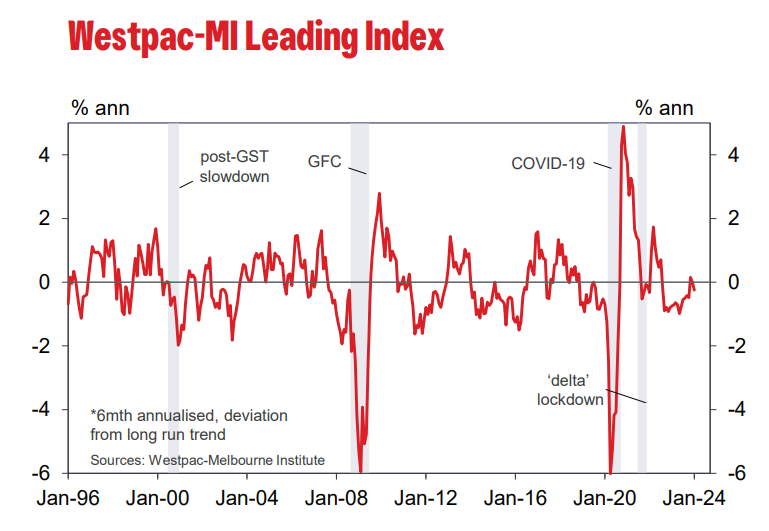

The six-month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, declined to –0.25% in January from–0.01% in December.

The Australian economy remains stuck in a below trend growth rut. While the Leading Index growth rate has improved on the weak reads seen through most of last year, it remains in negative territory overall implying the economy will continue to see sub-par growth well into 2024.

Westpac expects Australia’s economic growth to track a 1.3% annnualised pace in the first half of this year, lifting from a weak 0.8% pace over the second half of 2023 but still well below trend, which is around 2.5%yr. The latest Leading Index reads are consistent with this sluggish near-term growth profile.

Momentum looks set to remain subdued near-term but the growth pulse has definitely improved on a year ago. Over the first half of 2023, the Leading Index growth rate ranged between –0.75 and –1%, well below the –0.25% pace recorded in January.

However, the detail continues to suggest that this improvement is still, at best, a tentative stabilisation rather than the beginning of a move into a new cyclical upswing. The latest month has again seen mixed results across the eight components, half recording improvements and the other half deteriorations. Some of the monthly weakness is likely to be transitory with seasonal issues and noise exaggerating recent declines in hours worked and dwelling approvals. However, some of the positives are also not expected to sustain, a rally in commodity prices in particular.

Over the last six months, the Index growth rate has improved from –0.54% in July to –0.25%, a lift of 0.30ppts. Commodity prices (measured in AUD terms) have been the standout driver of the improvement, posting a strong 12.3% lift over the six months after dropping 17% over the previous six months. The turnaround has seen the Index growth rate contribution from this component swing from –0.43pts to +0.17pts – a 0.60ppt turnaround.

Where there have been other supports these have tended to be due to stabilisations or tentative recoveries rather than convincing upturns. The stabilising yield spread for example has effectively added a further 0.21ppts to the index growth rate since July but mainly reflects the end of rate hikes and growing market expectations of an easing cycle. A milder downtrend in dwelling approvals over the six months has added a further 0.14ppts represents a slower decline rather than a nascent recovery. Rallies in the S&P/ASX200 and in consumer sentiment-based measures have also added 0.20ppts to the

Index growth rate, on a combined basis, but both still look to be relatively tentative.

Meanwhile these positives have been significantly offset by a sharp deterioration in aggregate hours worked since mid-2023, which has effectively taken 0.74ppts off the index growth rate.

Even if the latest monthly weakness proves to be overstated, this component is still picking up a genuine softening in labour market conditions and activity that has further to run.

The Reserve Bank Board next meets on March 18-19. The latest Leading Index read suggests the patchy, sub-par growth momentum of 2023 is carrying into 2024.

High inflation remains the RBA’s primary concern. The minutes to the Board’s February meeting show that while there has been good progress towards bringing inflation back down to the Bank’s 2-3% target, it would take some time yet before the Board could be sufficiently confident that this would occur within a reasonable time frame – a view that led the Governor to be explicit in not ruling out the potential need for a further rate hike.

Economic updates between now and the March meeting are expected to underscore the weak growth and demand= environment domestically and give the RBA more comfort= on the inflation path. That points to rates again being left on hold at the Board’s March meeting. However, it’s likely to be some time yet before the Board adopts a more firmly ‘on hold’ position, and longer still before it may start to see the need and scope for interest rate cuts.