Westpac with the note.

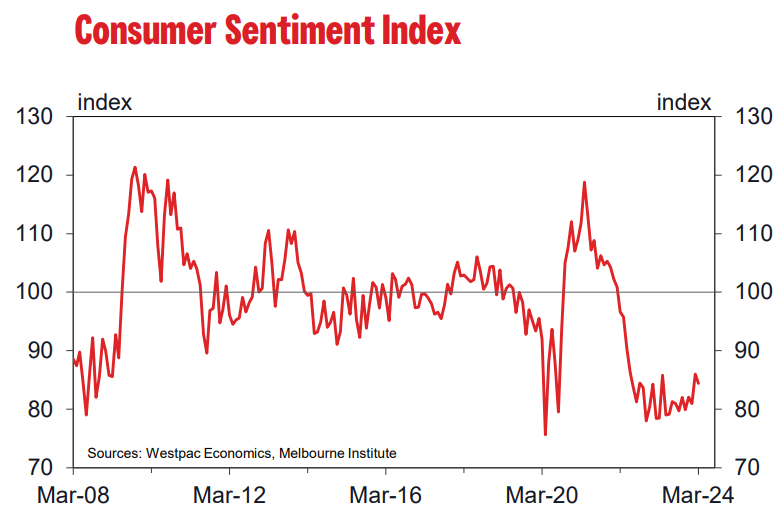

The Westpac Melbourne Institute Consumer Sentiment Index declined 1.8% to 84.4 in March, from 86 in February.

Last month we saw some promising signs that the consumer gloom that has dominated over the last two years might finally be starting to lift.

The March survey update shows that progress continues to be slow at best. Consumers are still deeply pessimistic and becoming more concerned about the economy’s near-term outlook.

There are still some signs of improvement, particularly in consumer responses to questions on news recall.

Our March, June, September and December surveys include additional questions about which news topics consumers recall and how favourable or unfavourable these were viewed.

Inflation continues to dominate the news cycle, but responses suggest the cost-of-living ‘crisis’ is become less acute.

Recall levels have eased back to 43% from the 60%+ highs seen last year when the issue was effectively drowning out everything else.

The negativity is also less intense, with a net 51% of consumers assessing inflation news as unfavourable compared to a net 74% this time last year.

The news on most other major topics is also viewed as less unfavourable than in December, including ‘budget and taxation’ news (likely reflecting recently announced changes to the Stage 3 tax cuts) and recent news on employment and interest rates.

The big exception is news about ‘economic conditions’ which was viewed as having deteriorated slightly; the soft December quarter national accounts were likely behind the result.

The component mix of the overall sentiment result also highlights renewed concerns about the economic outlook.

Four of the five sub-indexes recorded declines in March, with the biggest move a 4.5% fall in ‘economic outlook, next 12mths’ sub-index, which gave back just over half of last month’s gain.

Assessments of family finances and ‘time to buy a major household item’ also retraced some of their February gains, with all still well below long run average levels despite some modest net improvement over the last six months.

The only positive was around the ‘economic outlook, next 5 years’ sub-index which edged up 1.1% to be at 94, slightly above the long run average of 92.

Responses over the course of the survey week suggest sentiment made another sharp turnaround following the RBA decision.

Sentiment amongst those surveyed prior to the decision came in at a much stronger 94.9 compared to 79.3 amongst those surveyed post-decision – almost identical to the swing recorded in February.

The implication is that while few would have been expecting rates to be cut, many consumers may have been hoping for a more positive message on inflation and the interest rate outlook.

However, the RBA Governor was still not ruling out the possibility of further rate rises following the March meeting.

The RBA’s commentary looks to be tempering consumer expectations for interest rates as well, with fears of rate hikes easing but few expecting rate cuts any time soon.

The WestpacMelbourne Institute Mortgage Rate Expectations Index, which tracks consumer expectations for variable mortgage rates over the next 12 months, dipped 0.5% to 120.9.

The mix of responses shows 40% of consumers are still bracing for rate increases, 22% expect\ no change, 22% expect declines and 15% simply “don’t know.

Consumers remain relatively comfortable about the outlook for jobs. The Westpac-Melbourne Institute Unemployment Expectations Index rose slightly, by 1%, in February but at 128.1 is still in line with the long run average of 129.

Readings remain consistent with a softening in labour market conditions rather than a sharp rise in job losses.

Housing-related sentiment improved slightly overall with another lift in assessments of time to buy and price expectations holding at optimistic levels.

The ‘time to buy a dwelling’ index rose 4.9% to 77.8, a fifteen month high but still in a relatively weak, pessimistic range.

Buyer sentiment is notably stronger in Victoria (84.3) where Melbourne dwelling prices have seen some slight slippage over the last four months. In contrast, the NSW index is at just 73.3.

Continued gains in Sydney dwelling prices and the associated deterioration in affordability are clearly weighing more heavily.

The Westpac Melbourne Institute Index of House Price Expectations was essentially unchanged, dipping very slightly by 0.2% to 161.1. Nearly 70% of consumers expect housing prices to continue rising in the year ahead.

Consumer risk aversion eased slightly between December and March but remains high by historical standards.

Updates on our ‘wisest place for savings’ questions, run every three months, show ‘safe-haven’ options continue to dominate with three out of five consumers nominating either ‘pay down debt’ or ‘bank deposits’.

The mix showed a slight shift away from bank deposits and towards ‘real estate’ although the 8.4% favouring the latter remains very low compared to the long run average of 24%.

The Reserve Bank Board next meets on May 6–7. We expect the Board to again leave the official cash rate unchanged, provided inflation continues to track towards a return to the RBA’s 2–3% target over a reasonable time frame.

The extended period of weak consumer sentiment reads – added to with this latest update – and the associated flattening in demand are key to ensuring the cooling in inflation occurs in a timely way.

For consumers, the inflation and cost-of-living crisis may be becoming less acute but it will likely remain the dominant concern for some time yet.