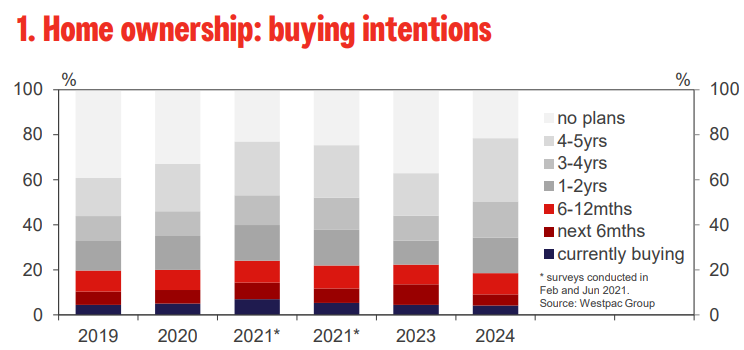

Westpac’s Home Ownership Housing Pulse shows Australians still yearn to own a home, with buying intentions over the next five years rising markedly from 2019.

However, affordability has become increasingly stretched by a “combination of high prices and interest rates,” pushing the dream of home ownership further out of reach.

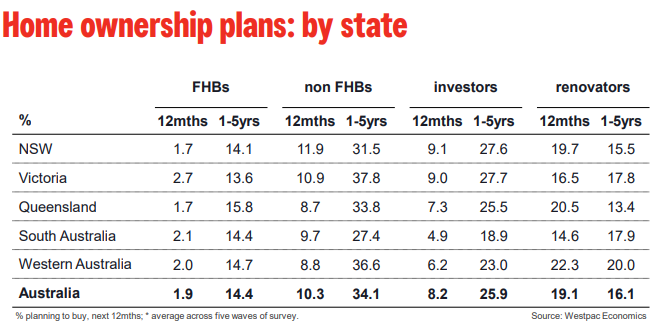

The prospective flow of first home buyers is showing the biggest response to these pressures, planned purchases down materially on last year. Just 2% of those surveyed expecting to become a first time owner in the next year.

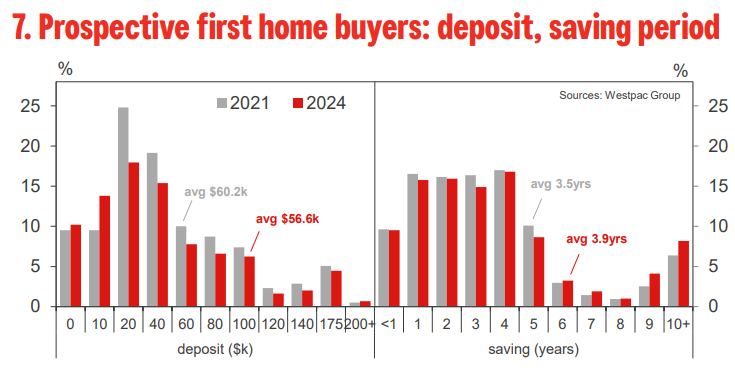

Compared to 2021, these prospective buyers expect it to take six months longer to raise a deposit that is nearly $4k smaller.

That said, they remain determined to achieve their goals and are open to adapting where and what type of house they buy.

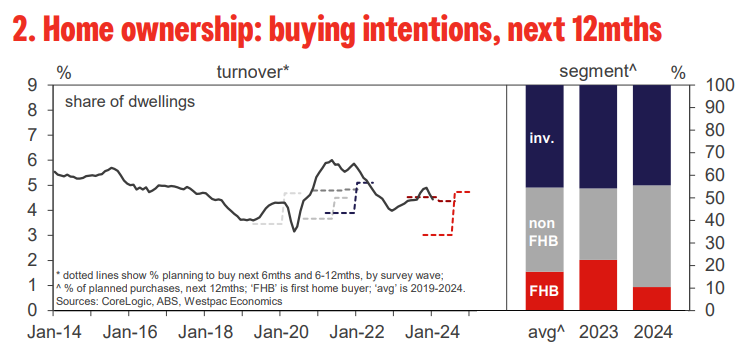

The stand-out message in 2024 is that purchase plans are being delayed. Just 9.1% of respondents expect to purchase a home in the next 6mths, down from 13.6% last year and the lowest result across all surveys.

However, the delay is expected to be relatively short-lived with 9.5% expecting to transact in 6-12mths (up on 8.7% last year) and a remarkable 60% planning to buy a home over the next 1-5yrs, well above the previous 53.5% high in mid-2021.

The segment detail suggests this profile reflects a variety of factors: affordability weighing heavily on some segments near term, but a degree of ‘pent-up’ demand starting to emerge elsewhere and signs that an expected ‘pivot’ in the interest rate cycle may be a more important factor for some buyer groups, investors in particular.

Prospective FHBs are at the pointy end of affordability and cost-of-living difficulties and appear to be the most ‘priced-out’ near term.

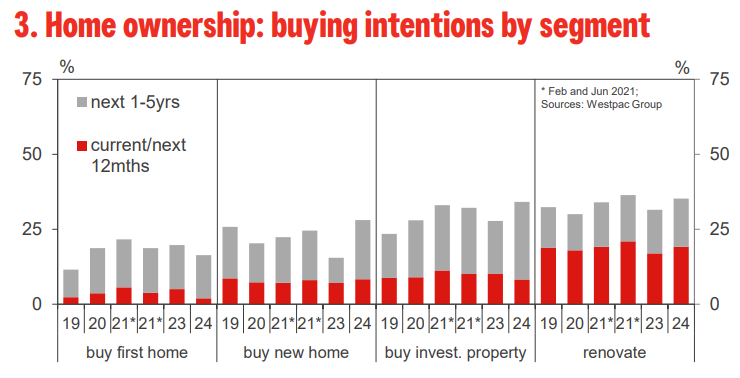

However, a relatively high proportion still plan to purchase over the next 5yrs, 16.3% vs 11.6% in 2019.

The segment remains determined to become homeowners with signs they are adapting their approach in order to achieve these goals (see below for more discussion).

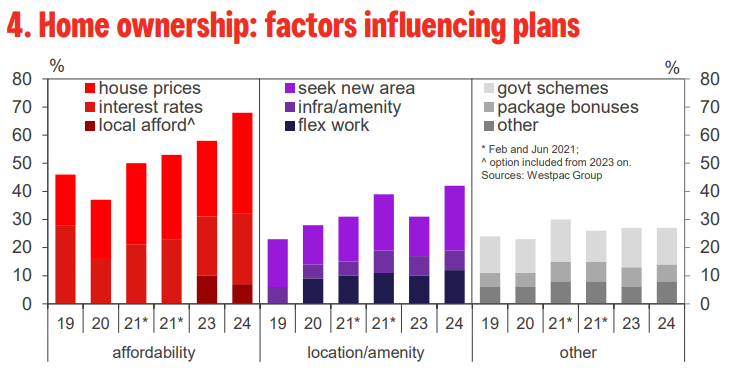

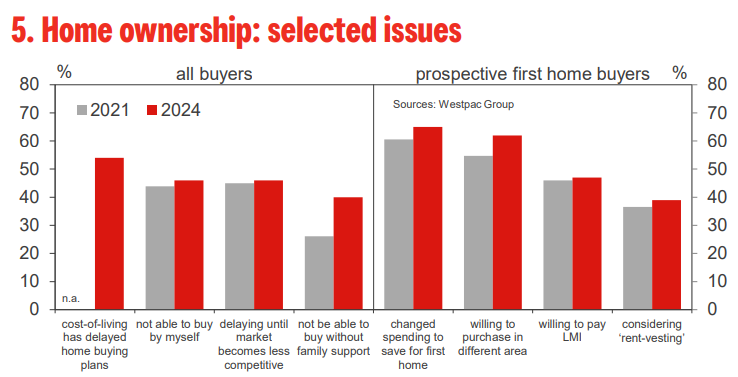

Charts 4, 5 provide some more colour around the factors influencing plans and views on specific issues.

Affordability related factors dominate, cited as an influence by 68% of respondents compared to 58% last year and an avg of 44% over the previous three surveys.

Notably, flexible work considerations remain a prominent consideration as well.

Cost of living issues were cited by over half of respondents as a key reason for delaying purchase plans. It has clearly become more difficult to raise funds for purchasing.

Indeed, 40% of respondents said they would be unable to buy without family support, up sharply from 26% in 2021.

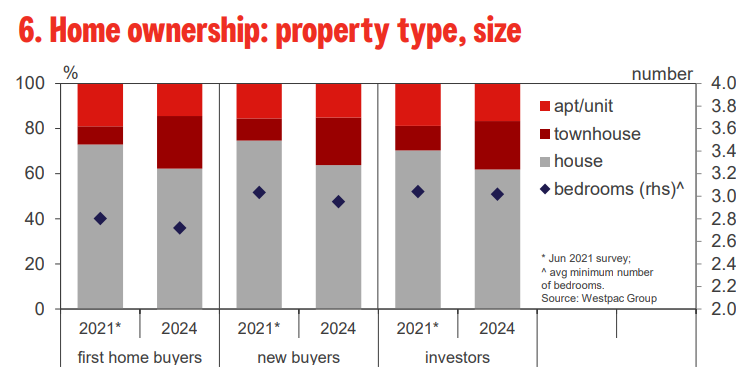

Chart 6 shows how these pressures are affecting the sort of dwellings prospective buyers are intending to purchase.

Nearly a quarter of prospective FHBs are now looking to buy townhouses, up from 8% in 2021, with similar but slightly less pronounced shifts across other segments.

In contrast, only 14-16% are planning to by apartments/units, down slightly on 2021. The avg mix in terms of bedroom size has also been creeping lower.

The bigger shift in the specs of intended property purchases amongst prospective FHBs reflects the more difficult environment for this buyer group.

Chart 7 shows how much of a deposit this group expects to have when they come to buy and how long they expect it will take to accumulate these funds. Both speak to intense pressures.

On avg, deposits are expected to be $3.6k smaller than prospective buyers had been planning for in 2021 and the timeline for saving about 6mths longer.

The proportion of prospective FHBs anticipating a 5yr+ savings slog has risen to 18.5% from 14.3% three years ago, with around half of that group expecting it to take a decade or more.

Nearly a quarter expect to have only accumulated a deposit of less than $20k, compared to 19% in 2021.