DXY eased last night:

AUD bounced:

North Asia meh:

Brent looks like it is coiling:

Dirt yawn:

Miners yawn:

EM yawn:

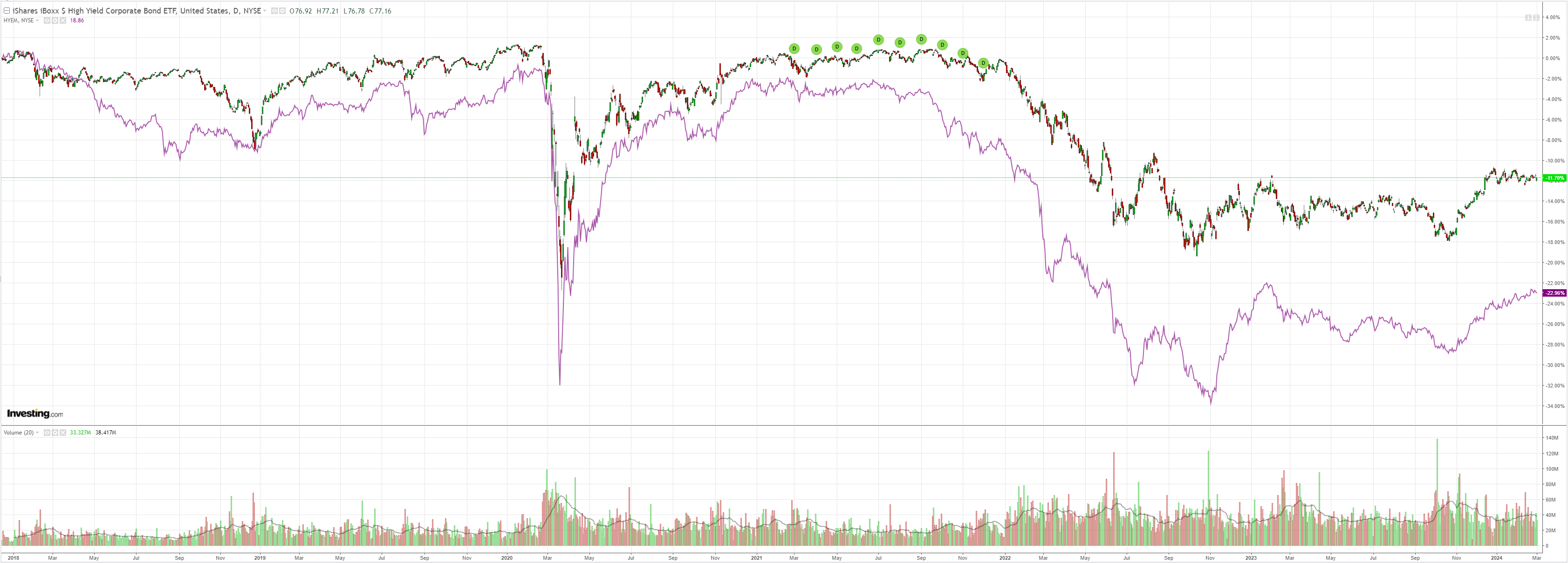

Junk meh:

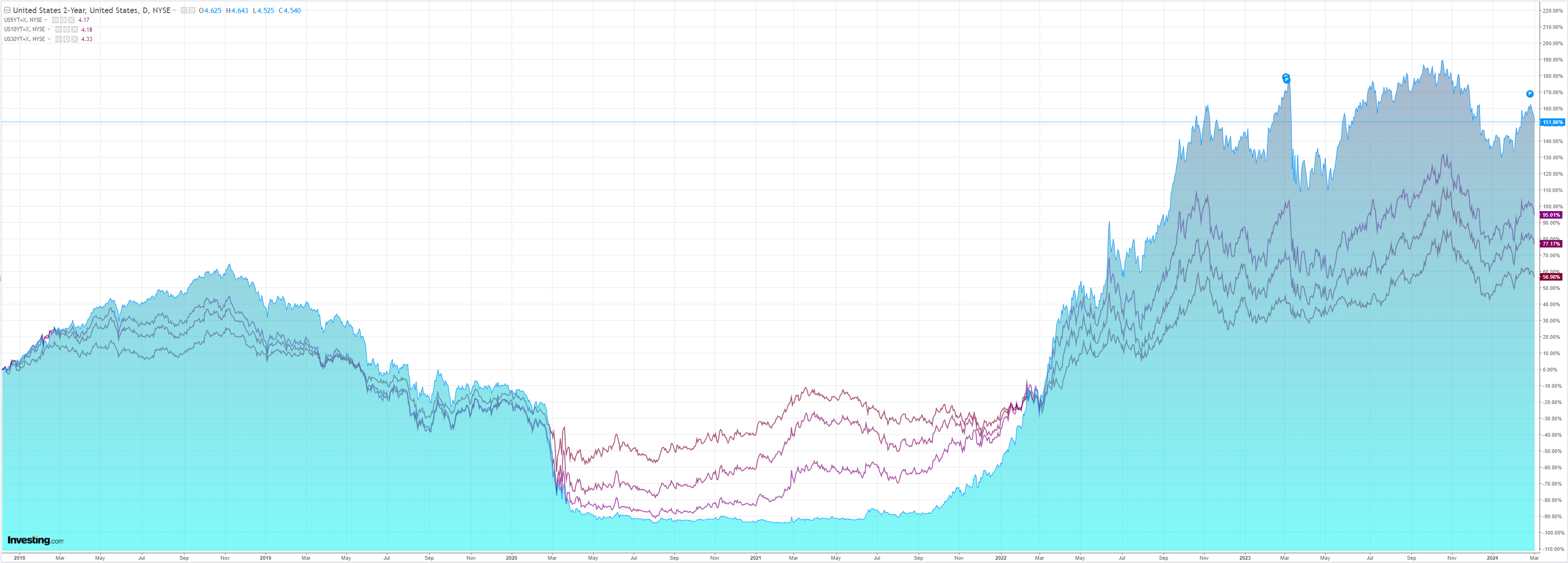

Yields dumped:

Stocks flew:

The ISM was perfectly weak:

“The Manufacturing PMI® registered 47.8 percent in February, down 1.3 percentage points from the 49.1 percent recorded in January. The overall economy continued in expansion for the 46th month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.5 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index moved back into contraction territory at 49.2 percent, 3.3 percentage points lower than the 52.5 percent recorded in January.

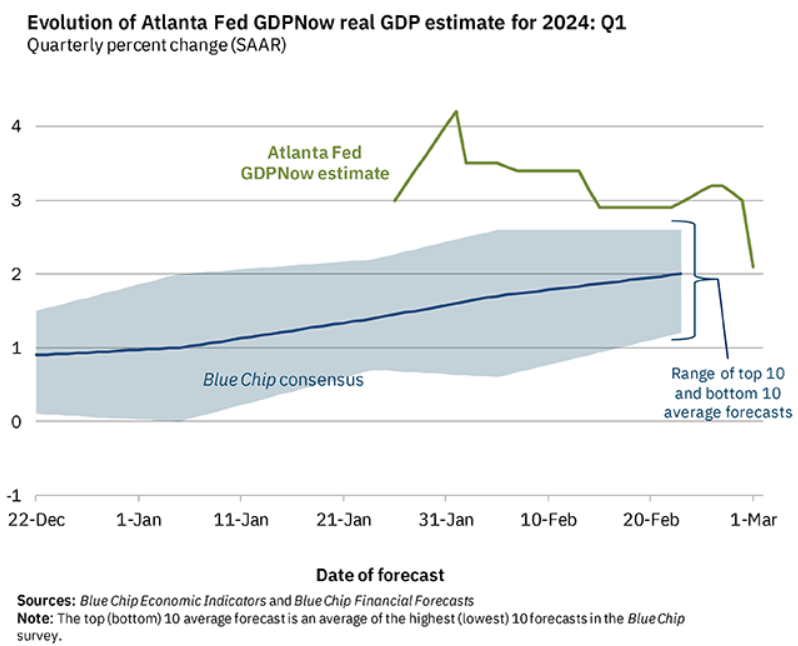

Q1 GDPNow is falling fast:

Which liquidity-loving risk loved. Then came Nirvana from Fed Governor Christopher Waller:

First, I would like to see the Fed’s agency MBS holdings go to zero. Agency MBS holdings have been slow to run off the portfolio, at a recent monthly average of about $15 billion, because the underlying mortgages have very low interest rates and prepayments are quite small. I believe it is important to see a continued reduction in these holdings.

Second, I would like to see a shift in Treasury holdings toward a larger share of shorter-dated Treasury securities. Prior to the Global Financial Crisis, we held approximately one-third of our portfolio in Treasury bills. Today, bills are less than 5 percent of our Treasury holdings and less than 3 percent of our total securities holdings. Moving toward more Treasury bills would shift the maturity structure more toward our policy rate – the overnight federal funds rate – and allow our income and expenses to rise and fall together as the FOMC increases and cuts the target range. This approach could also assist a future asset purchase program because we could let the short-term securities roll off the portfolio and not increase the balance sheet. This is an issue the FOMC will need to decide in the next couple of years.

You might recall that it was the US Treasury’s pivot to short-end bonds (bills) late last year that kicked off the current rally in risk, as fears of a long-end deluge driving interest rates even higher evaporated.

Now, the Fed is mulling buying the bills in perfect union.

I expect a short-term AUD rally when the Fed begins easing, and this modest move towards QE could be the start of it.

Let’s see what China does with the latest round of yawnulus this week.