DXY eased:

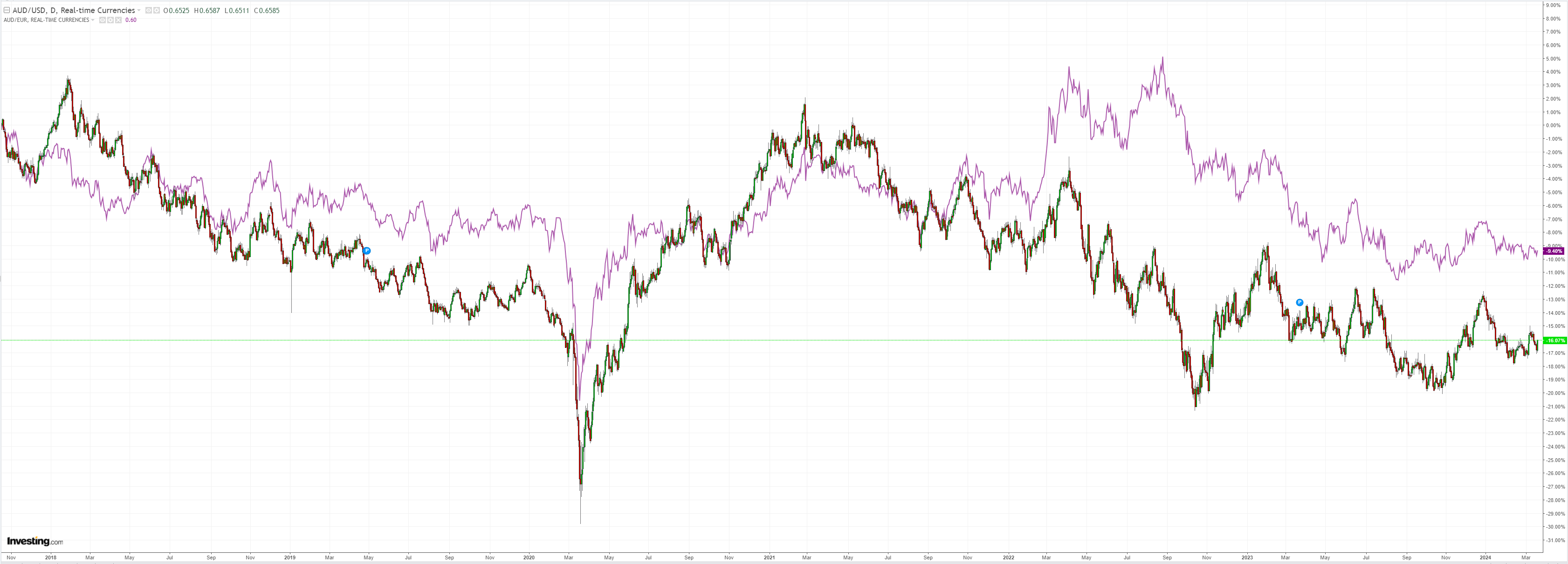

AUD popped:

North Asia sagged:

Oil and gold traded places:

Metals meh:

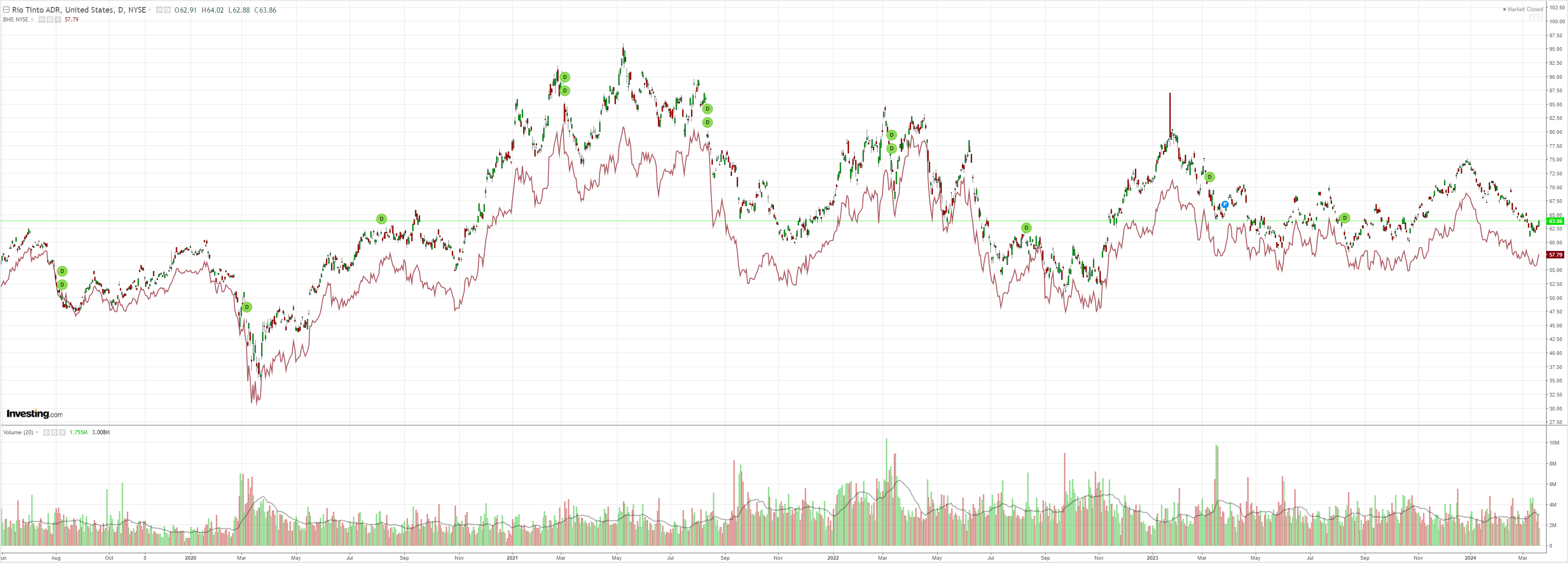

Miners are dead cat bouncing:

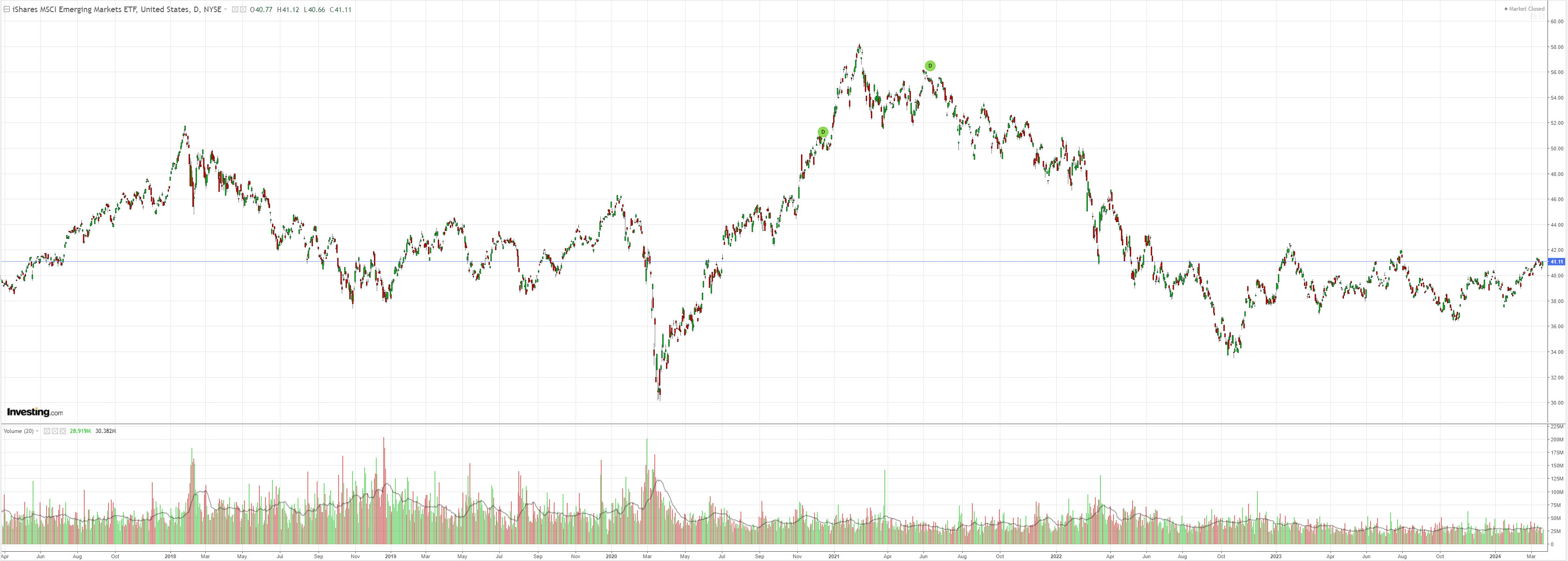

EM warmed up:

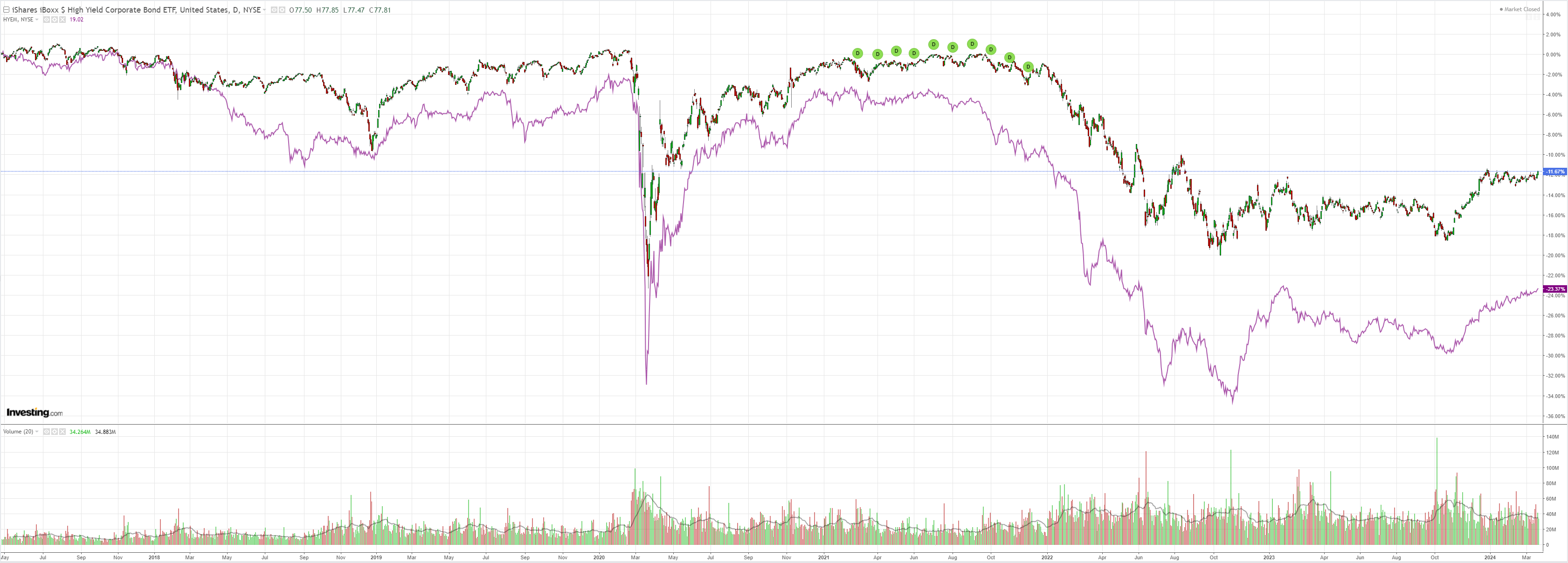

Junk is bullish:

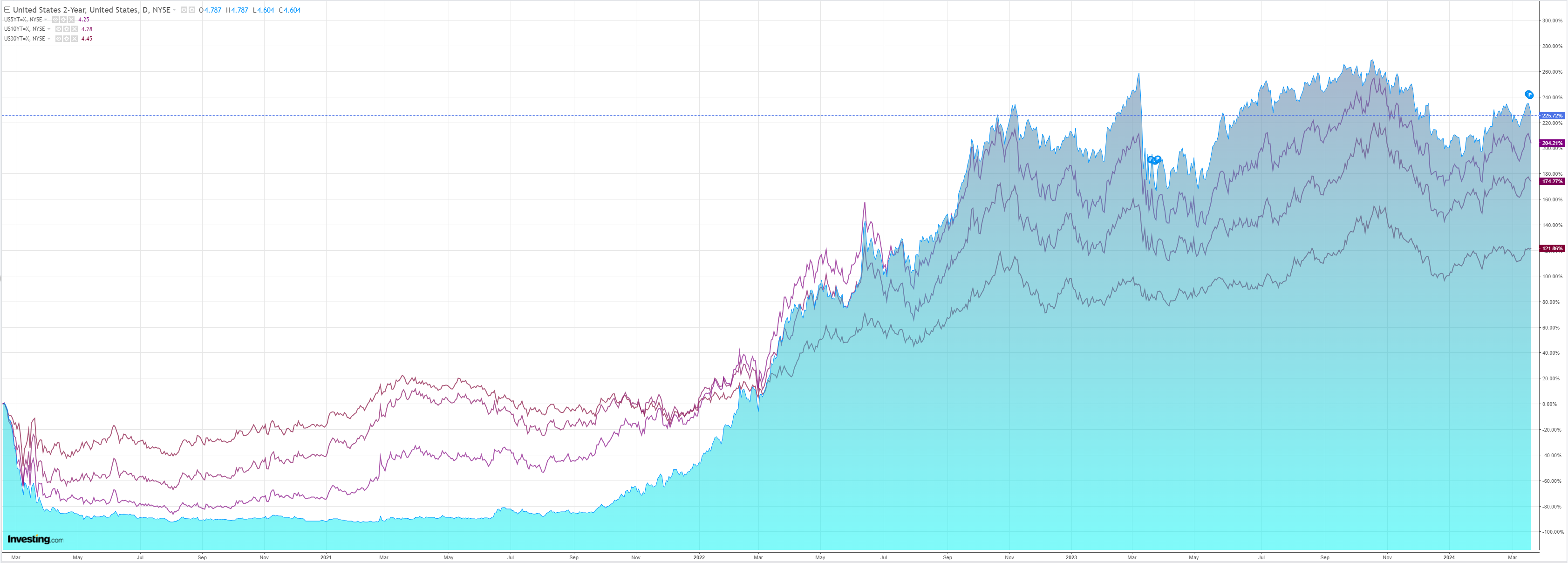

Curve steepened:

Stocks only go up:

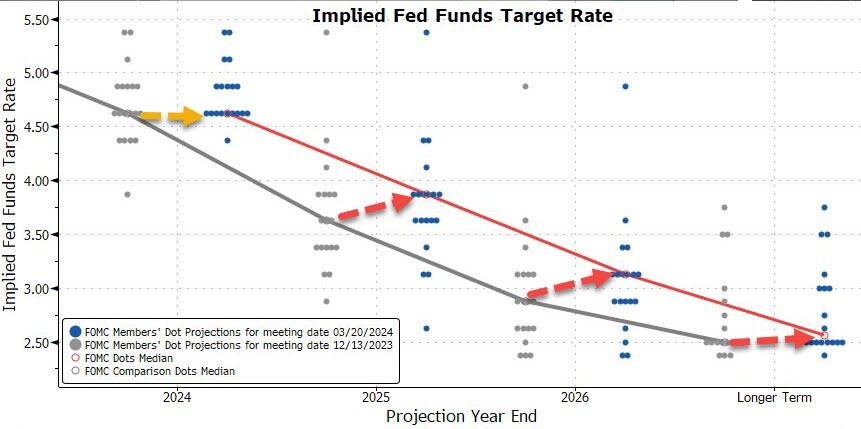

The Fed is going to cut regardless of recent jitters. The forecast “dots” got less dovish but Chair Powell was clear:

Powell calls the longer-run interest rate change “pretty modest”.

“I don’t think we know that,” Powell says about whether this will be a lasting trend.

However, Powell did admit rates are unlikely to be going ZIRP anytime soon:

“I don’t see rates going back down to that level but I think there’s tremendous uncertainty on that.”

If the Fed eases too much or too soon, he says, we could see inflation come back.

And if we ease too late, we could do unnecessary harm to employment.

“We want to be careful,” Powell says, stressing that “the risks are really two-sided here.”

Powell signaled balance sheet reduction will slow (less QT >> more QE):

“We did not make any decisions today. The general sense of the committee is that it’ll be appropriate to slow the pace of runoff fairly soon, consistent with the plans we previously issued.”

Powell also rather dismissed the recent jump in inflation:

“There’s reason to think that there could be seasonal effects there,” Powell says about the January CPI and PCE figures, and then says that February PCE wasn’t “terribly high.”

AUD will be off to the races for a while when the Fed cuts but not for very long and not for very far.

The US neutral interest rate is rising, while the Australian neutral interest rate is falling as Peak Human, Peak Fat, and Peak China converge.

Need help with forex? MB recommends OFX, with whom we have negotiated no fees and cheap transfer rates for MB readers. Click the logo for more.