Markets and economists have a tendency to look backwards and on the bright side. This is usually a good idea. An economy is not an easy thing to knock off course.

But sometimes it happens. Today is one of those times.

The RBA hiked in November and the economy hit a brick wall in both December and January.

We now have two labour market reports, multiple private-sector jobs reports, two NAB surveys and a CPI report, plus PMIs all pointing in the same direction: hard down.

One can pick holes in all data but all of this together is telling us something. And that something is the economy is at a standstill.

Westpac has lost its edge with the departure of Bill Evans. He was the one that made the big pivot calls. But even without him it is starting to mull the obvious.

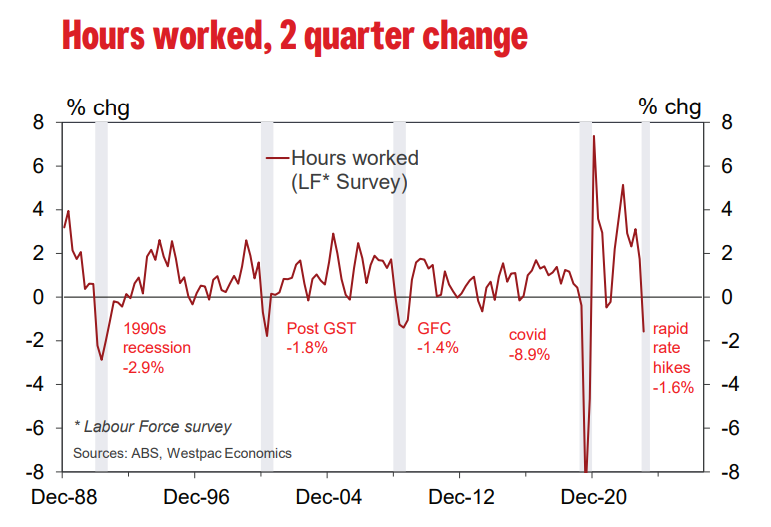

Here we provide an update on quarterly hours worked and consider the possible implications for quarterly economic activity.

As occurred last month, the ABS downgraded recent history for hours worked in the Labour Force Survey (LFS).

The LFS now reports that for the December quarter hours worked declined by -0.7%. That is downgraded from -0.4%, or to two decimal places, lowered to -0.66% from -0.44%.

In the September quarter, hours worked is now -0.9% in the LFS, rounded down from -0.8%. Recall that the National Accounts printed less weak hours worked for the period, at -0.6%, which was associated with a tepid 0.2% rise in output.

As for the December quarter National Accounts, potentially they will report a larger decline in hours worked than the -0.7% in the LFS.

The pattern over recent years is that the National Accounts December quarter estimate for hours worked is a little softer than the LFS – the reverse of the September quarter relationship. Whether this December quarter pattern continues in 2023 is a source of uncertainty.

Declining hours worked for Q4 point to a further rebound in labour productivity, but how large a bounce is unclear.

Westpac Economics is forecasting GDP growth of +0.2% for the December quarter. The expectation is that growth went sideways, after printing a 0.2% for the September quarter, which represented a material slowing from 0.5% and 0.4% for the two prior quarters.

On the available partial information, the risks to our Q4 GDP forecast are tilting to the downside.

As discussed here, we are mindful of disappointing goods trade data and a softening of private business surveys.

Ahead of the December quarter National Accounts release on March 6, there are still a raft of unknowns and the potential for further and material surprises – which could shift the balance of risks around our Q4 GDP forecast of 0.2%.

We would identify public demand as a wild card and potential source of upside surprise, which may be sufficient to keep the economy expanding in the final months of 2023.

Who cares if public investment saved Q4 from contraction? Deloitte this week made it clear that it is peaking now after Albo’s recent cut backs. The consumer is in a deep recession, which will drag business investment down in due course.

Labor supply is still booming as well.

If the RBA doesn’t hard pivot soon, it is going to shove the labour market into an unemployment overshoot.

You don’t fatten the pig on market day.