God save us from the iMSM and Ronald Mizen:

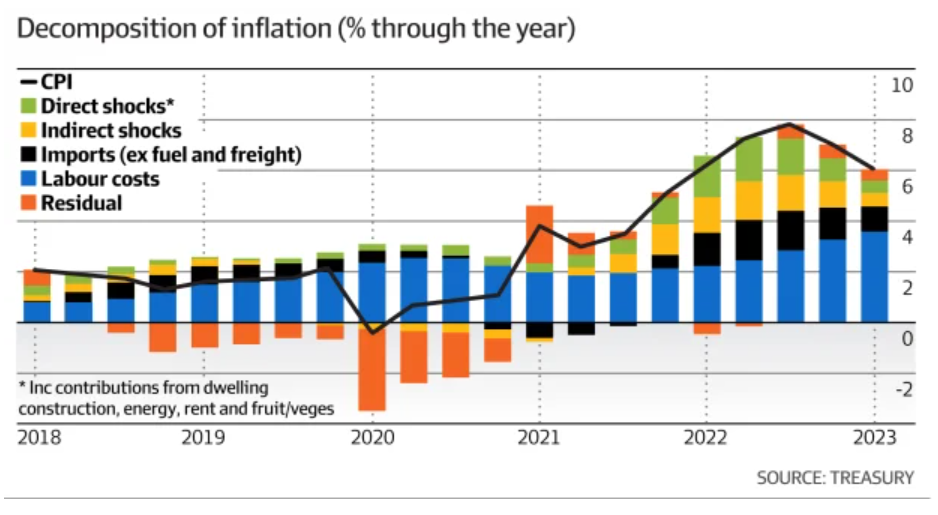

Confidential Treasury analysis shows decade high wages growth that has pushed the average fulltime salary above $100,000 is now the biggest driver of consumer price inflation, undercutting claims widespread corporate profit gouging is to blame.

Pay rises overtook import prices and supply shocks to form the lion’s share of headline CPI in the June quarter last year, according to Treasury analysis obtained by The Australian Financial Review under freedom of information, a trend economists expect continued to the end of 2023 and into 2024.

The analysis undercuts claims from the Greens, unions and former ACCC chairman Allan Fels that widespread price gouging has been causing price rises. Those claims have sparked a wave of inquiries, including a Greens-led Senate probe into supermarket pricing, a year-long inquiry led by the ACCC, and a review of the voluntary grocery code by Craig Emerson.

Blind Freddy can see that the lion’s share of the post-COVID inflation shock was not from wages. All of those other “shocks” can be rebadged “profits”. Sure, not all Aussie profits, but profits nonetheless.

As wages are finally growing, only just in real terms, they have become a larger component of inflation, and so what?

At under 4%, wage growth is still soft and within the scope of the RBA’s 2-3% inflation band so long as productivity rises.

The good news is Peak Fat and AI will deliver some productivity gains to the economy over the next few years.

The bad news is that this rising and healthier labour supply will collide with the mass-immigration economy to deliver all the productivity income gains to increased corporate margins.

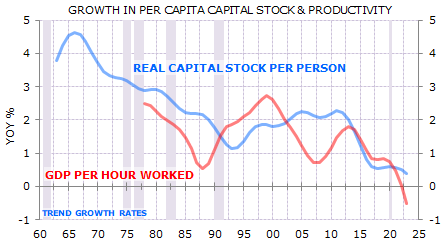

Before then, there is nothing for Treasury to worry about, either. The immigration-led economy does not do productivity owing to the failure of the capital stock to keep pace per capita:

Nor does it do wage growth, thanks to the permanent cheap foreign supply shock.

What will happen instead is what has happened since the mass immigration economy was birthed post-mining boom: productivity and wages will both be suppressed, and rentier profits will be gouged by the chosen industries that benefit: property, retail and banks.

This is also why the RBA is once again misreading the economy, having learned nothing from a decade-long wages scare campaign pre-COVID:

“As supply shocks subside and inflation dynamics normalise, wages growth will again become the main driver of inflation, given that labour costs are, ordinarily, the largest cost for business,” said Dr Sarah Hunter, Treasury’s former head of macroeconomics and now chief economist at the RBA.

Get ready to be surprised by falling wage growth and rate cut rates to feed the beast.