Late last month, the weaker-than-expected Q4 CPI inflation print flamed expectations that the Reserve Bank of New Zealand may soon cut the official cash rate (OCR).

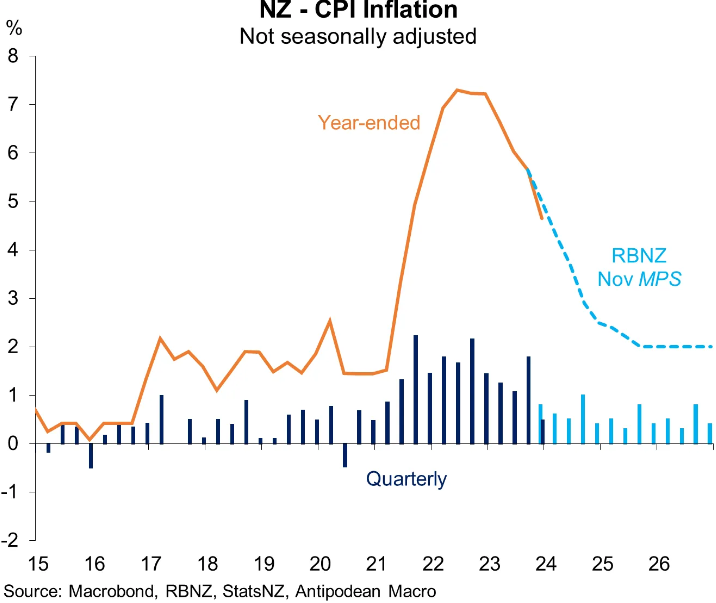

Headline CPI inflation fell quicker than the Reserve Bank’s projections in Q4:

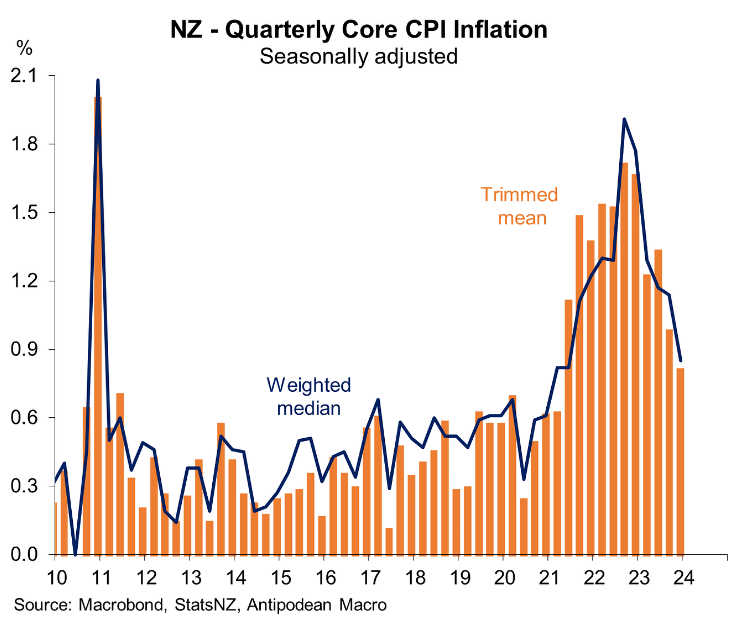

Core Inflation also fell swiftly:

.

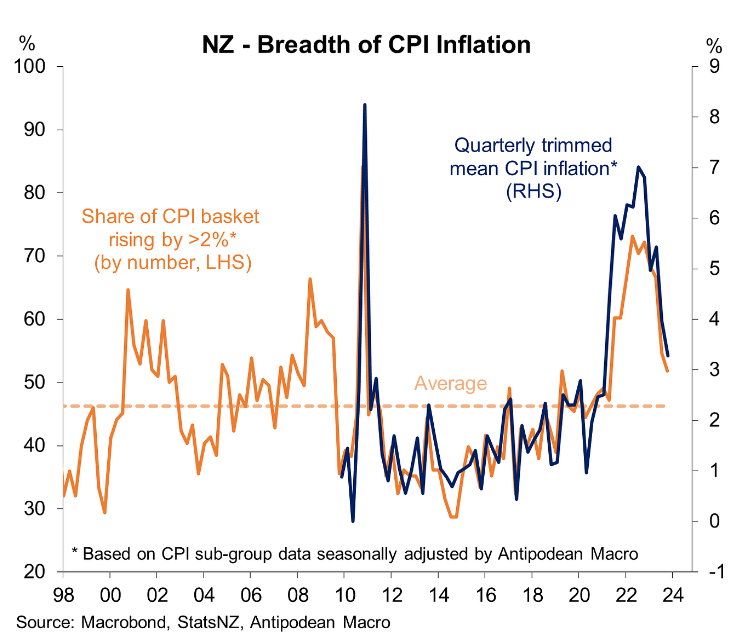

. While the breadth of inflation plummeted:

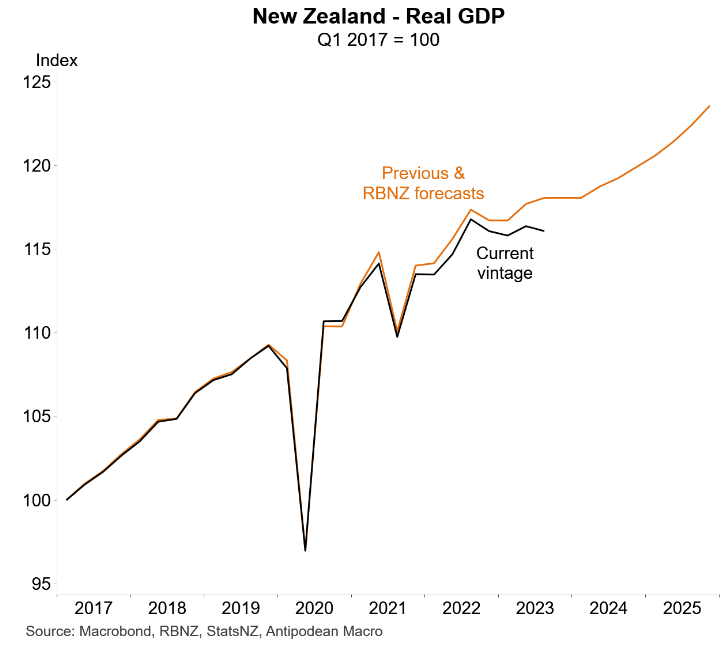

The New Zealand economy has also slowed faster than the Reserve Bank projected, with the economy mired in recession:

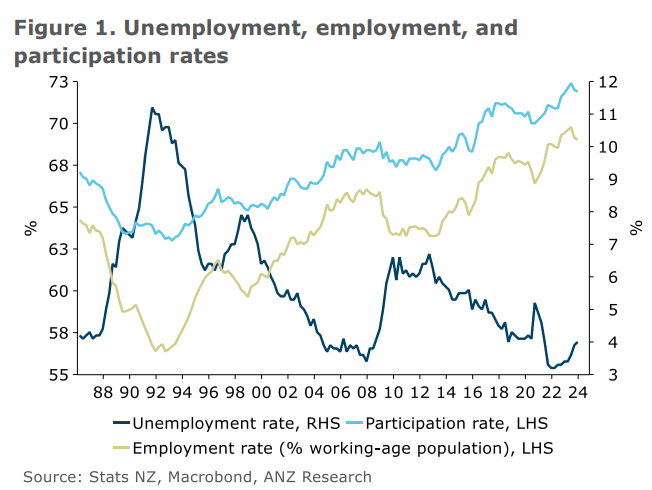

But then came last week’s stronger-than-expected labour market print. This saw New Zealand’s unemployment rate rise from 3.9% to 4.0% in Q4, below the Reserve Bank’s forecast of 4.2%:

Employment increased by 0.4% over Q4, stronger than the Reserve Bank’s expectation of a 0.2% quarterly increase:

Annual wage growth also eased, but by less than what the Reserve Bank expected.

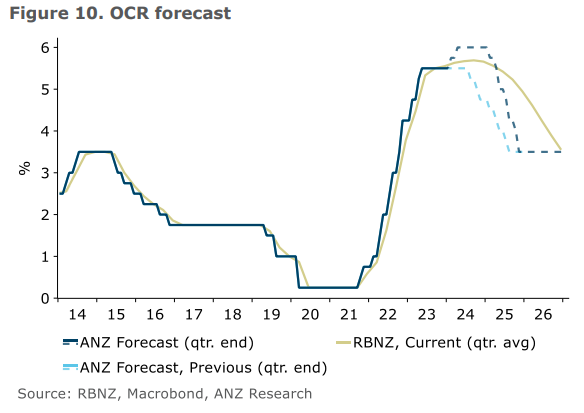

Following this labour force data and hawkish commentary from the Reserve Bank staff, ANZ flipped to “forecasting 25bp hikes in both February and April, taking the OCR to 6%. We are now forecasting cuts from February 2025, ultimately taking the OCR back to 3.5% as before”:

Westpac has now entered the fold and while it is not tipping further rate hikes, it also is not tipping any rate cutes in 2024:

“We continue to think the OCR will remain at 5.5% at the February Monetary Policy Statement”.

“Resilience in domestic inflation pressures and the labour market will be of concern to the RBNZ”.

“But very weak economic momentum, lower headline inflation and a flatter housing market of late are important mitigants”.

“We see another hawkish Statement that even might bring forward potential tightening and continues to lean heavily against expectations of policy easing this year”.

“Data on inflation, the labour and housing markets, together with the details of the Budget, will be important in making the case for further tightening, if required”.

“We don’t see scope for interest rate cuts in 2024″…

“We think the RBNZ will be on edge. The RBNZ will likely threaten further tightening and may ultimately deliver action this year should inflation pressures not recede fast enough”…

“But we do think the RBNZ has time to let the data talk. Economic momentum is very weak, and the possibility of a rapid labour market adjustment remains real as firms react to the weakness in demand seen in the last six months of last year”…

“Hence, we see another hawkish Statement later this month, that could potentially threaten policy tightening sooner than indicated in November. We see that as consistent with continuing with the “longer” strategy while managing the risks that the current OCR might not deliver sufficient disinflation”.

“A sudden switch in strategy to one of higher interest rates seems dangerous this late in the cycle. And in the context of likely developments in interest rates in other advanced economies over the second half of this year, a further hike in domestic interest rates would inevitably put upward pressure on the exchange rate – at least in the near term”.

“We don’t think the RBNZ will panic just yet. But forget about easings in 2024 – it just isn’t happening based on what we see now. And we might be back to tightening should conditions prove necessary”.

Much like Australia, the economic data will do the talking.

If New Zealand’s economy weakens materially, the Reserve Bank will cut. If the economy strengthens, it will hike. Otherwise, it will remain on hold.