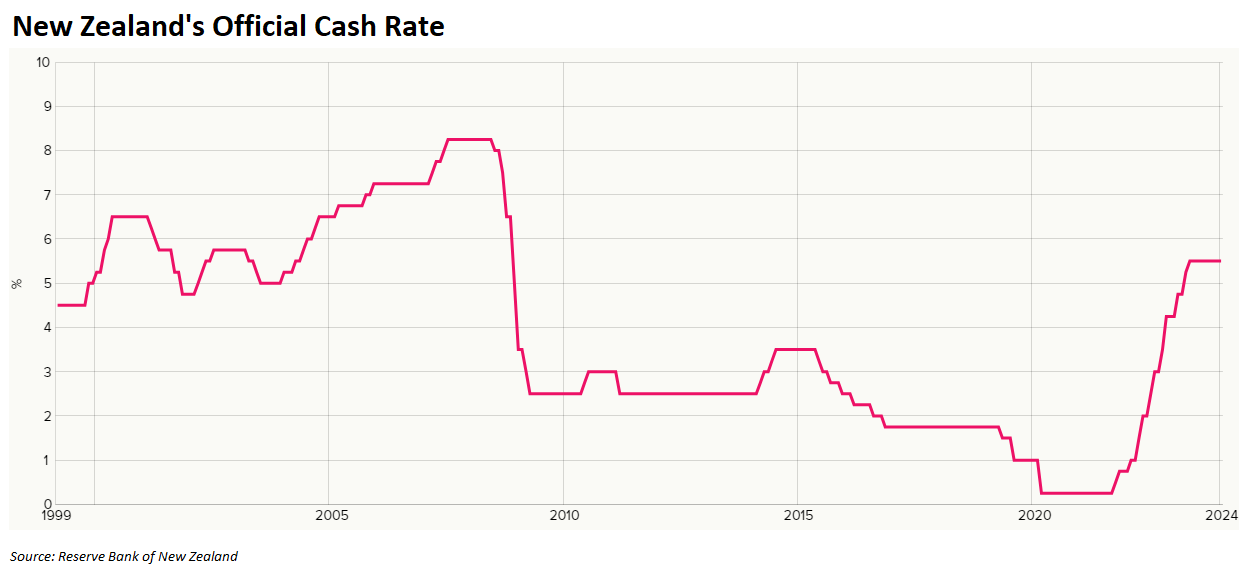

The Reserve Bank of New Zealand was one of the world’s most aggressive central banks, commencing its interest rate tightening cycle in October 2021 and hiking the official cash rate (OCR) by 5.25% over this cycle:

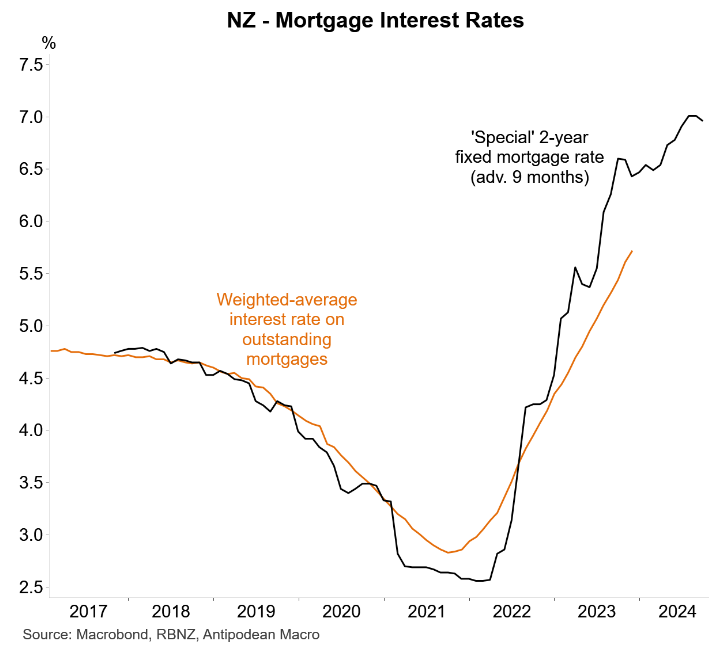

As illustrated in the below chart from Justin Fabo at Antipodean Macro, average New Zealand mortgage rates continue to rise, reflecting the rollover of fixed-rate mortgages to variable:

The latest data from the Reserve Bank of New Zealand shows that mortgage demand remains moribund:

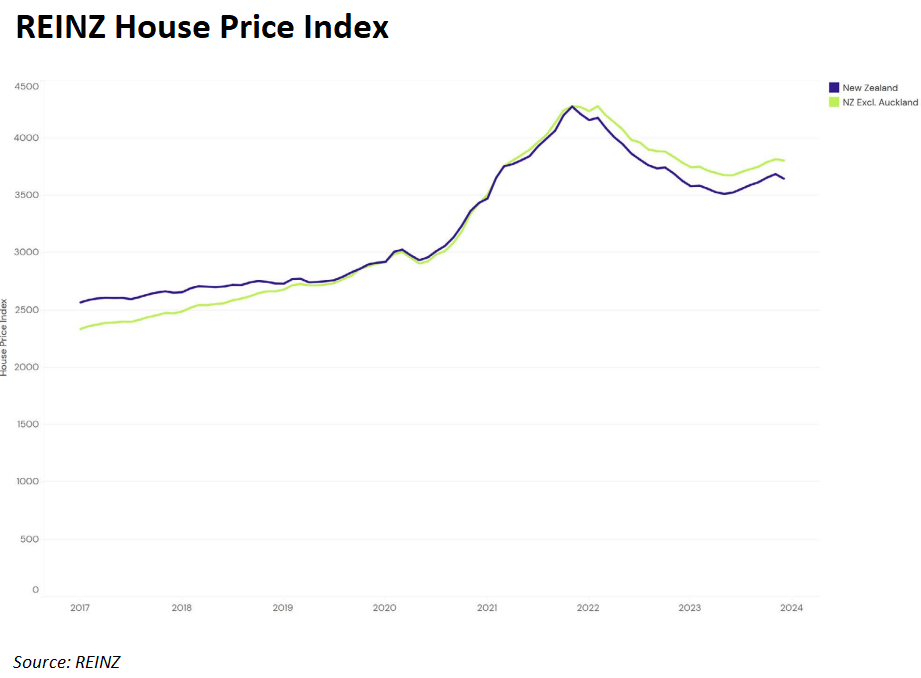

The latest results from the Real Estate Institute of New Zealand reported that house prices dipped 1.1% over the month to be 0.5% higher year-on-year:

Meanwhile, Auckland’s leading real estate agency, Barfoot and Thompson, reported rising new listings, sluggish sales, and falling prices in January.

The agency sold 504 residential properties in January – well below the long term average for the month and down 37% on January 2022 and down 54% on January 2021, according to Interest.co.nz.

New listings at Barfoot and Thompson were up by a third compared to January last year and were the second highest for the month of January in the last 10 years.

Prices of homes sold by the agency also plummeted.

“The average price of the residential properties the agency sold in January was $1,083,487, down by $97,812 (-8.3%) compared to December last year, and down by $195,160 (-15.3%) from its December 2021 peak”, Interest.co.nz reported.

“The median selling price in January was $966,500, down by $73,500 (-7.1%) compared to December and down by $273,500 (-22.1%) from its November 2021 peak”.

“The high level of stock on hand means potential buyers are starting the year with plenty to choose from and the weaker prices that were evident last month suggest they should be able to negotiate a good deal”.

The Reserve Bank’s aggressive interest rate hikes are clearly weighing on the housing market and are another reason why the central bank is poised to cut rates later this year.