The Reserve Bank of New Zealand has gone against the forecasts of ANZ and TD Securities and chosen to hold the official cash rate (OCR) at 5.50% at Wednesday’s monetary policy meeting.

In its statement accompanying its decision, the Reserve Bank noted that “core inflation and most measures of inflation expectations have declined, and the risks to the inflation outlook have become more balanced”.

“Restrictive monetary policy and lower global growth have contributed to aggregate demand slowing to better match the supply capacity of the New Zealand economy”, the statement reads.

“With high immigration and weaker demand growth, capacity constraints in the New Zealand labour market have eased”.

However, the Reserve Bank also acknowledges that strong immigration is “supporting aggregate spending, as evident in upward pressure on dwelling rents, for example”.

The Reserve Bank also hosed down suggestions that it would lift the OCR further in the near term, instead indicating that it would remain on hold “for a sustained period of time”.

“The Committee remains confident that the current level of the OCR is restricting demand”, the statement reads.

“However, a sustained decline in capacity pressures in the New Zealand economy is required to ensure that headline inflation returns to the 1 to 3%”.

“The OCR needs to remain at a restrictive level for a sustained period of time to ensure this occurs”, the Reserve Bank warns.

This outcome should have been obvious to any economist.

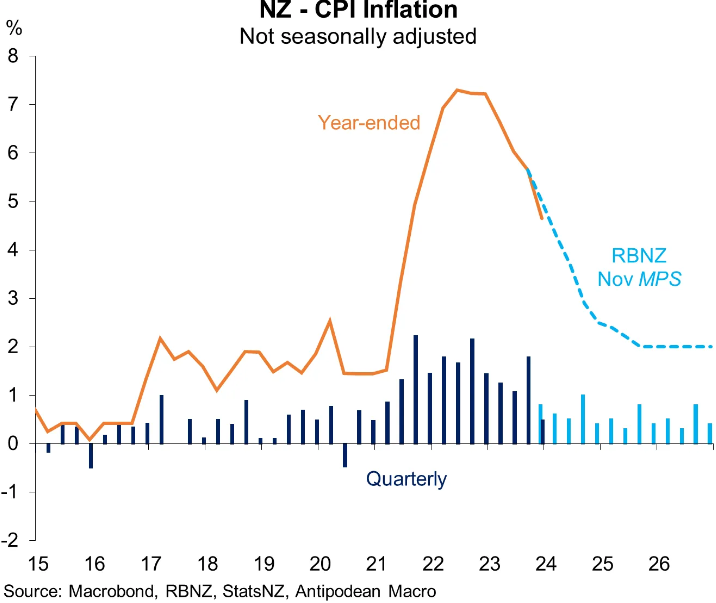

New Zealand CPI inflation has fallen faster than the Reserve Bank’s forecasts:

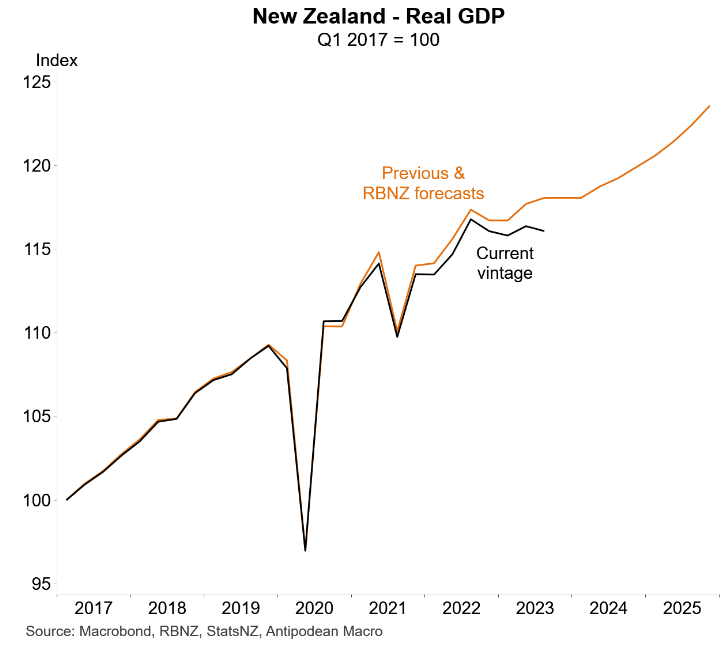

The economy is mired in a deeper recession than forecast by the Reserve Bank:

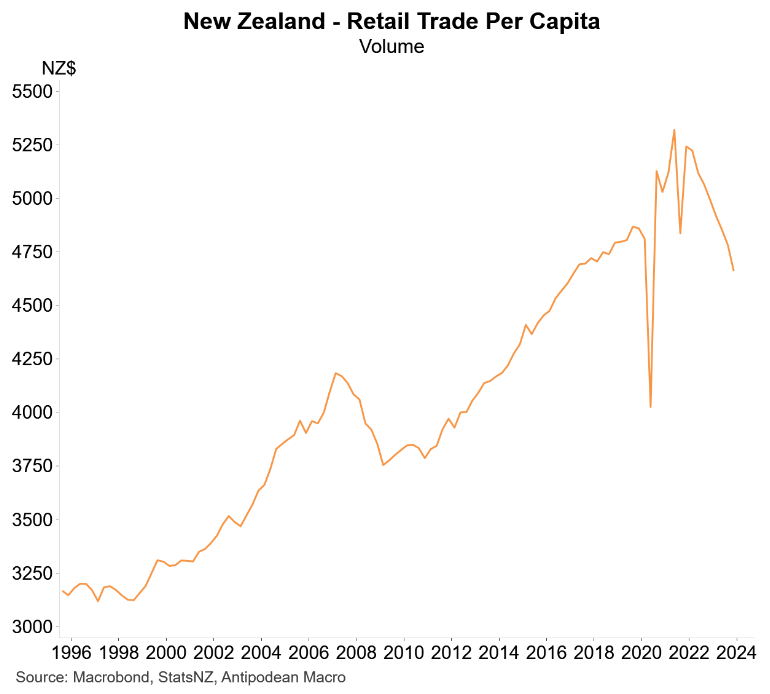

Consumption spending, as measured by retail sales, have collapsed:

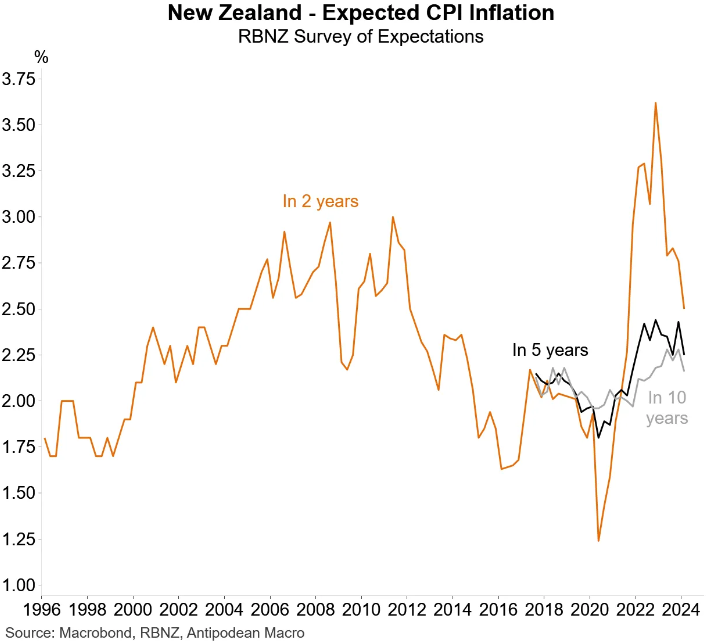

Finally, inflation expectations have fallen:

These are not the types of macroeconomic conditions conducive to interest rate hikes.

To the contrary, the next move in the OCR will be down, most likely late this year.