The Reserve Bank of Australia (RBA) held the official cash rate (OCR) at 4.35%, as expected by analysts.

In its statement, the RBA noted that inflation is easing but remains high.

It also noted that the outlook is uncertain and that it would await further data before changing its tightening bias.

Below are highlights from the statement.

Inflation continues to moderate but remains high.

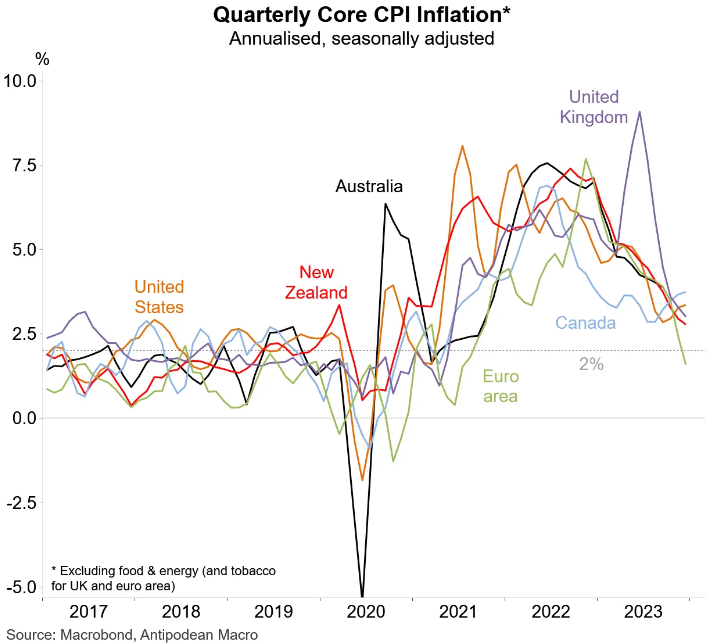

Inflation continued to ease in the December quarter. Despite this progress, inflation remains high at 4.1%.

Goods price inflation was lower than the RBA’s November forecasts. It has continued to ease, reflecting the resolution of earlier global supply chain disruptions and a moderation in domestic demand for goods.

Services price inflation, however, declined at a more gradual pace in line with the RBA’s earlier forecasts and remains high. This is consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs.

Higher interest rates are working to establish a more sustainable balance between aggregate demand and supply in the economy.

Accordingly, conditions in the labour market continue to ease gradually, although they remain tighter than is consistent with sustained full employment and inflation at target.

Wages growth has picked up but is not expected to increase much further and remains consistent with the inflation target, on the assumption that productivity growth increases to around its long-run average.

Inflation is still weighing on people’s real incomes and household consumption growth is weak, as is dwelling investment.

The outlook is still highly uncertain.

While there are encouraging signs, the economic outlook is uncertain and the Board remains highly attentive to inflation risks.

The central forecasts are for inflation to return to the target range of 2%–3% in 2025, and to the midpoint in 2026.

Services price inflation is expected to decline gradually as demand moderates and growth in labour and non-labour costs eases.

Employment is expected to continue to grow moderately and the unemployment rate and the broader underutilisation rate are expected to increase a bit further.

While there have been favourable signs on goods price inflation abroad, services price inflation has remained persistent and the same could occur in Australia.

There also remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts in Ukraine and the Middle East.

Domestically, there are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while the labour market remains tight.

The outlook for household consumption also remains uncertain.

Returning inflation to target is the priority.

Returning inflation to target within a reasonable timeframe remains the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment.

The Board needs to be confident that inflation is moving sustainably towards the target range. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

While recent data indicate that inflation is easing, it remains high. The Board expects that it will be some time yet before inflation is sustainably in the target range.

The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks, and a further increase in interest rates cannot be ruled out.

The Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market.

The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

With inflation falling globally (including in Australia), I still expect rate cuts in the second half of the year as the data weakens.