The Australian’s Patrick Commins published a detailed analysis of how different age groups in Australia have been impacted by the Reserve Bank of Australia’s (RBA) interest rate hikes, which have lifted the official cash rate by 4.25% since April 2022.

The most recent national accounts data for Australia show that households’ interest income increased from $7.7 billion in the September 2021 quarter to a record $21.1 billion, which has increased the wealth of many Australians, particularly those who have bank savings and no mortgage.

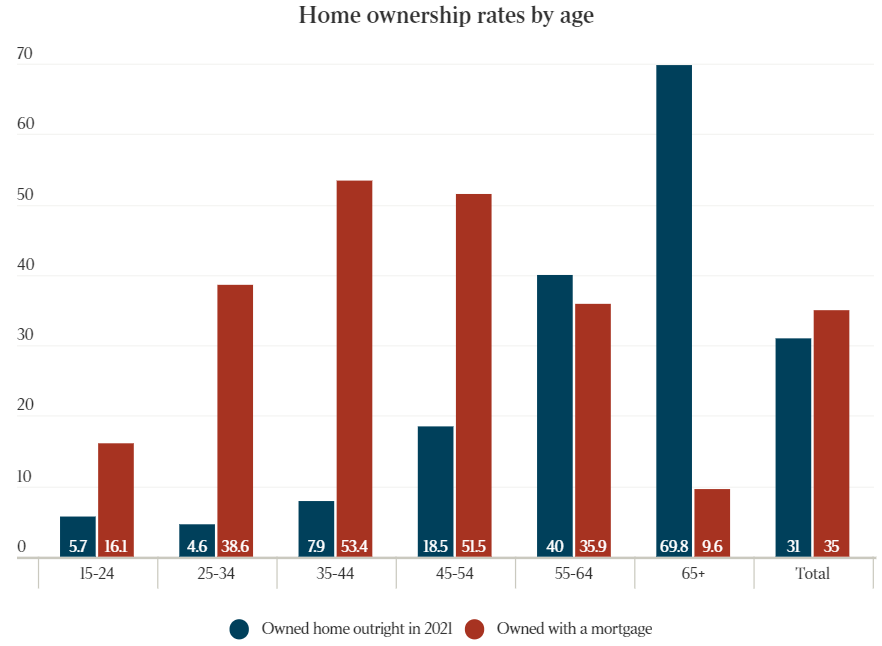

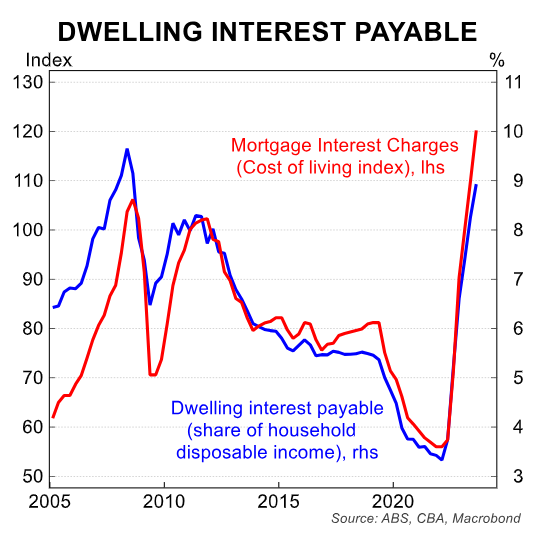

By contrast, younger people who rent or have a mortgage have been hardest hit by the 13 interest rate hikes in less than two years. They have suffered a 40% jump in mortgage interest payments through 2023. They also tend to have less savings than older people.

“There’s a stark contrast between the experiences of older generations with younger ones – although you have to be careful not to over-generalise, as some older Australians are still working and are hit with higher inflation and are under the pump”, said Warren Hogan, Judo Bank economic adviser.

“What it (rapid rise in borrowing costs) seems to be doing is putting a small proportion of the household sector under extreme pressure, a significant proportion under mild stress and belt tightening, and there are others feeling very little stress”.

“They are adding to demand in the economy now, but longer term, it’s also a major generational pressure point”, he said.

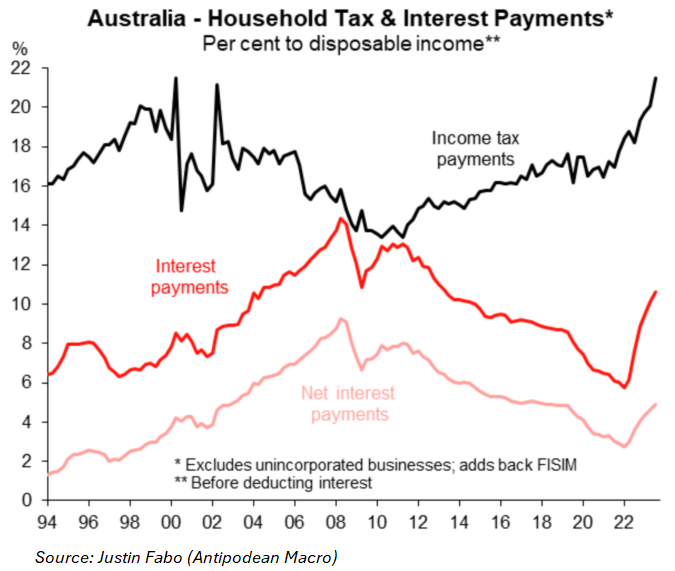

I will also add that older Australians tend to be retired. Most do not work. Therefore, this cohort has been largely unaffected by the surge in income tax payments and bracket creep, which are smashing working Australians.

Australians on the aged pension also have their payments linked to inflation (unlike workers’ wages), meaning their purchasing power was maintained as prices rose.

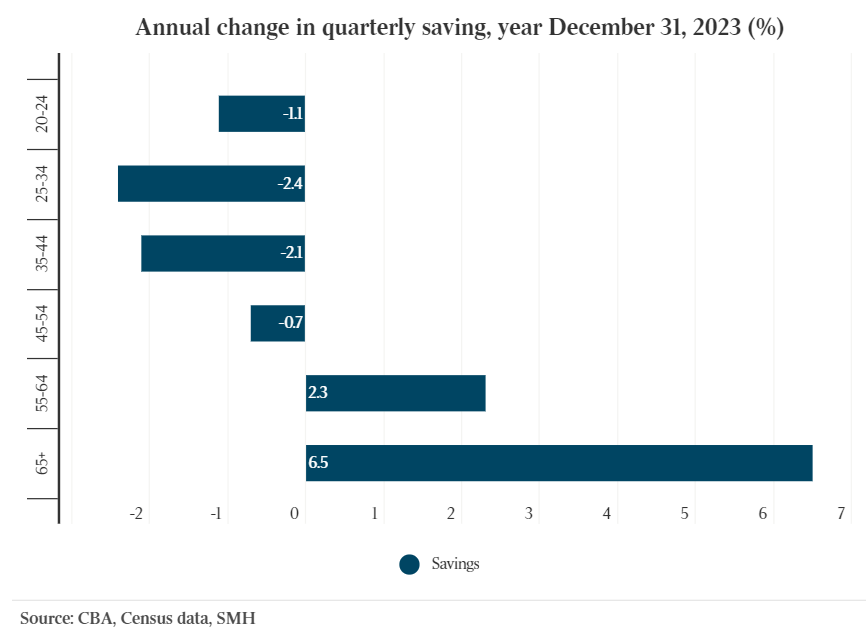

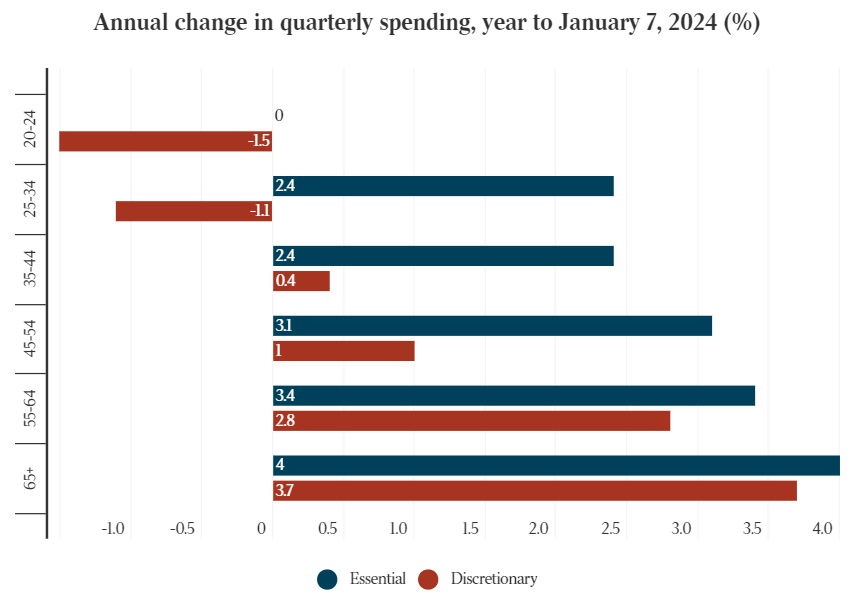

The increase in savings and wealth flowing to the older generations has seen them spend up large while the younger generations cut back. This is illustrated clearly in the next chart published in The Australian:

As shown above, Australians aged 65-plus increased their discretionary and essential spending the most in the year to 7 January 2024.

By contrast, Australians aged under 35 cut their discretionary spending hard while also increasing their spending on essentials by far less.

The above data and analysis highlight why Australia needs fundamental tax reform that broadens the base away from taxing work and towards more efficient sources, such as resources, land, and consumption.

It is unsustainable, inefficient, and inequitable for the tax system to be overly reliant on a shrinking share of workers while the proportion of taxes gained from indirect sources (e.g., GST and fuel excise) continues to decline.

This is especially so given that the older generation is expanding and paying less tax than ever before, despite holding the majority of the nation’s wealth.