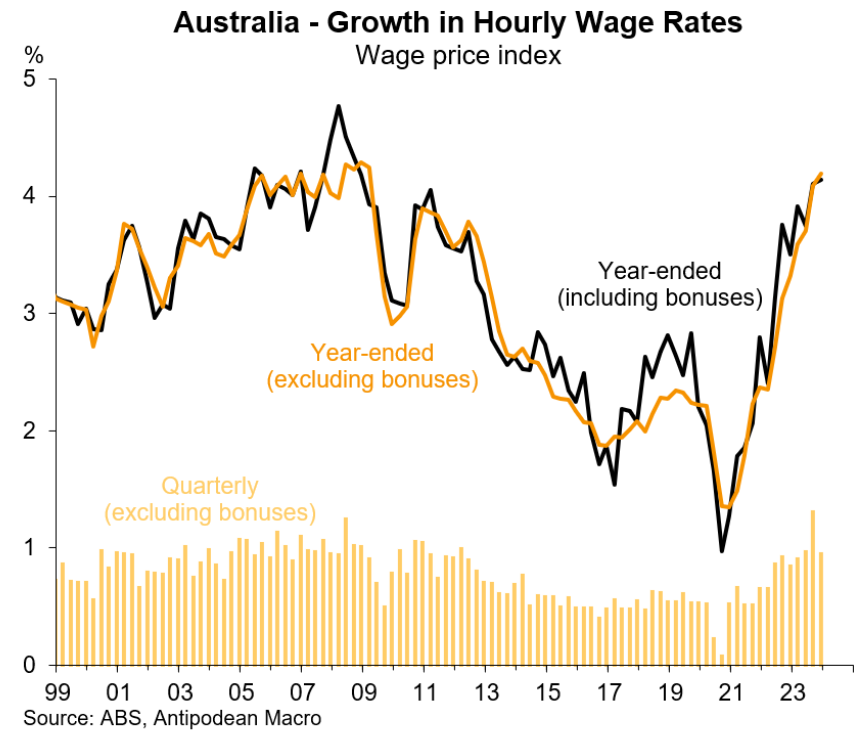

Justin Fabo at Antipodean Macro has published a series of charts assessing Wednesday’s wage price index data from the Australian Bureau of Statistics (ABS), which posted the strongest annual nominal growth since March 2009.

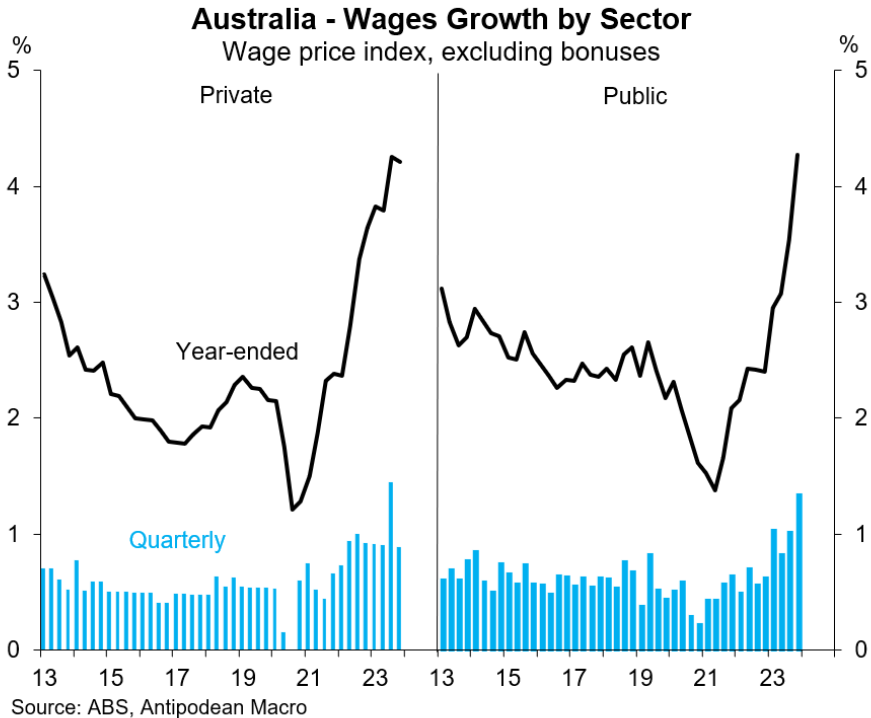

“Private-sector wages growth was +0.9% q/q while public-sector wages growth of +1.3% q/q was boosted by pay outcomes for health workers and teachers”, noted Fabo:

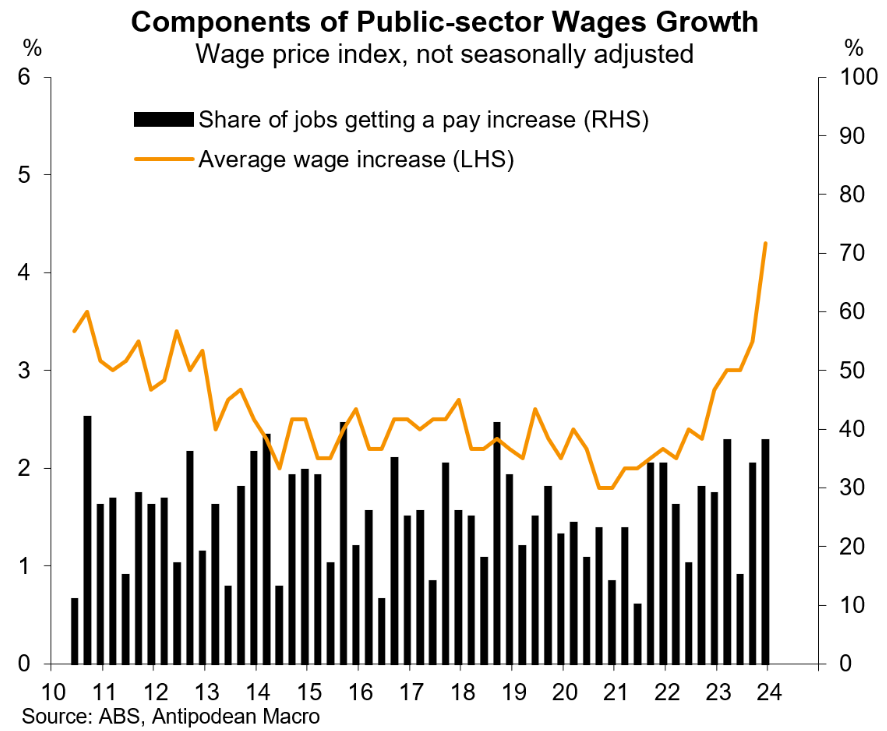

Interestingly, “the share of public-sector jobs getting a pay increase in Q4 was the highest for a December quarter in at least 14 years”, according to Fabo:

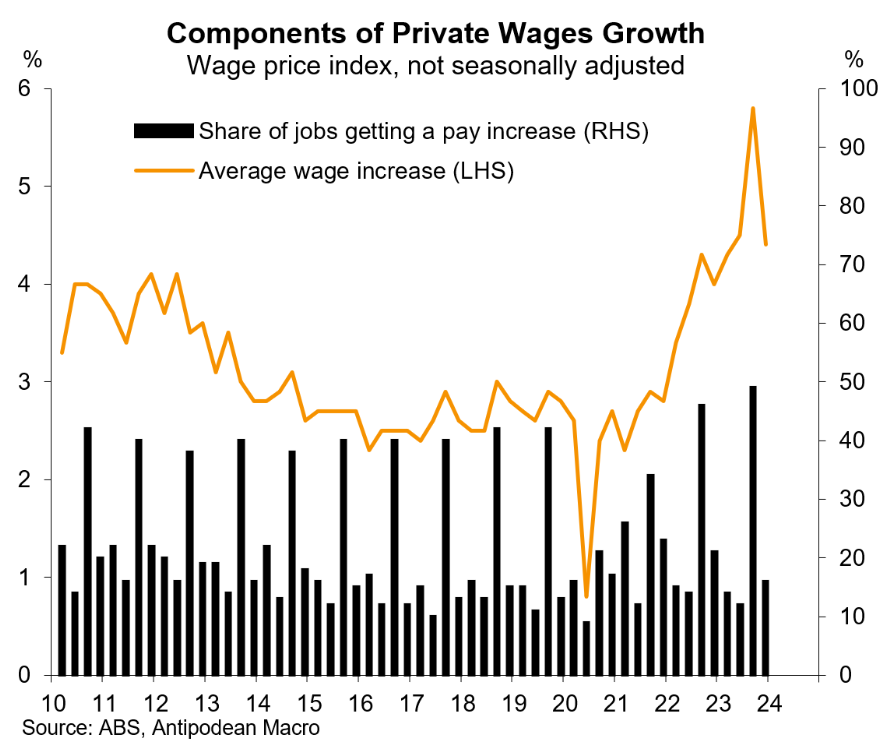

By contrast, wage pressures across the private sector are abating fast. The next chart shows that just “16% of private-sector jobs in Australia received a pay increase in Q4 (of 4.4%), down from 21% a year earlier and the lowest share since Q4 2019”;

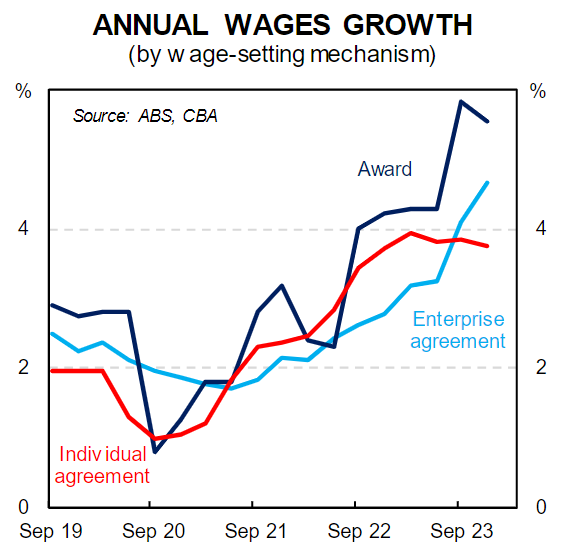

CBA senior economist, Belinda Allen noted that “individual agreements recorded growth of 3.7%/yr to Q4 23, the slowest since December 2022”.

“Jobs set by individual agreements are generally more tied to demand for labour. The loosening of the labour market seen in recent months is dampening wages growth pressure in individual agreements”.

“The slowdown in individual agreements and the loosening in the labour market suggests that wages growth should be peaking at current rates and should start to slow over 2024. Individual agreements account for 38% of wage setting agreements and as underutilisation rises in the labour market, private sector wages growth should slow”.

“Our expectation is that wages growth moderates from current levels to 3.6% by year-end. Near-term pressure will still occur from enterprise agreements, but a slowing economy, rising labour market spare capacity, and disinflation will gradually weigh on nominal wage increases”, Allen said.

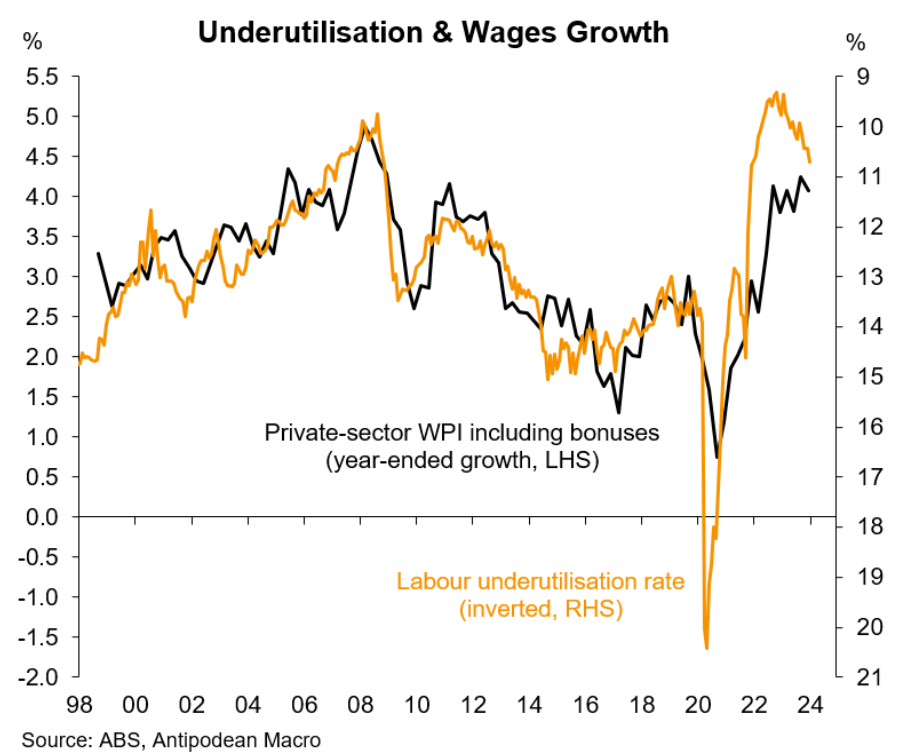

Justin Fabo noted that the “easing in Australian labour market conditions, and lower inflation expectations, are starting to show up in slightly less robust private-sector wages growth”.

This is evidenced when plotting the labour underutilisation rate against wage growth:

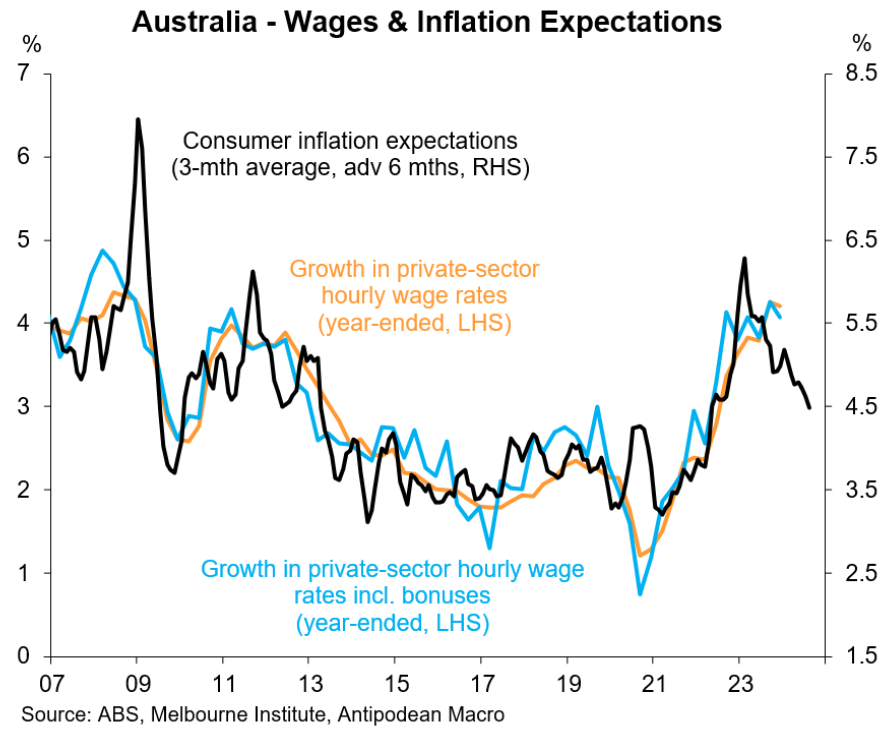

It is also evident when wages are plotted against inflation expectations:

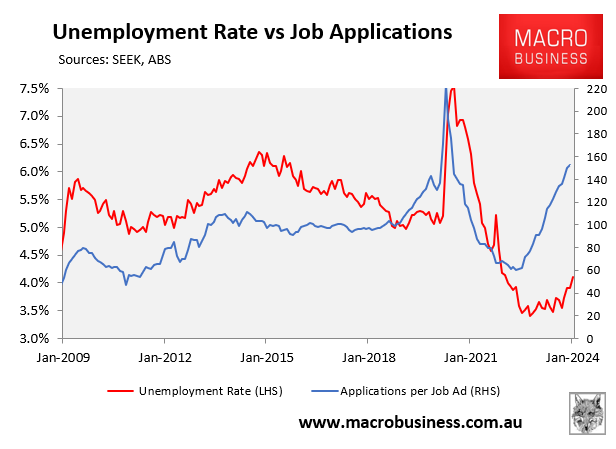

Australia’s labour market is not generating enough jobs or hours to soak up the historically strong growth in the labour supply brought about by high immigrations and Peter Costello’s early 2000s “Baby Bonus” kids hitting working age.

Accordingly, the number of applicants per job advertisement has soared, pointing to higher unemployment in the period ahead:

The higher competition for jobs inevitably means that wage growth will slow.

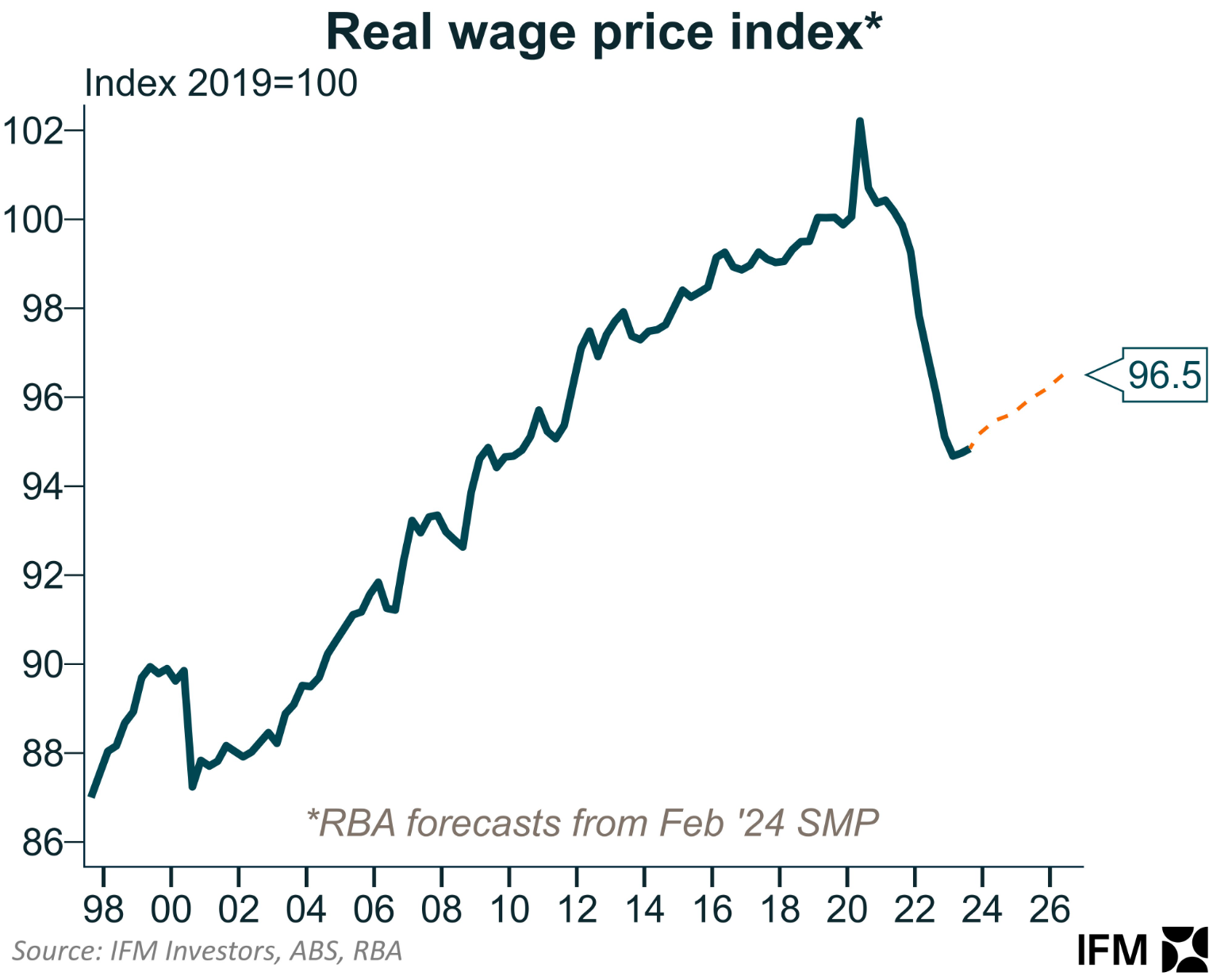

On a related note, Alex Joiner at IFM Investors has created the next chart showing that Australian real wages will be 3.5% below their 2019 level by 2026, based on the RBA’s projections:

Thus, it will be a long road back to rising living standards for Australian workers.