The Reserve Bank of Australia (RBA) might be done raising the official cash rate (OCR). But that doesn’t mean that the pain is over for Australian mortgage holders.

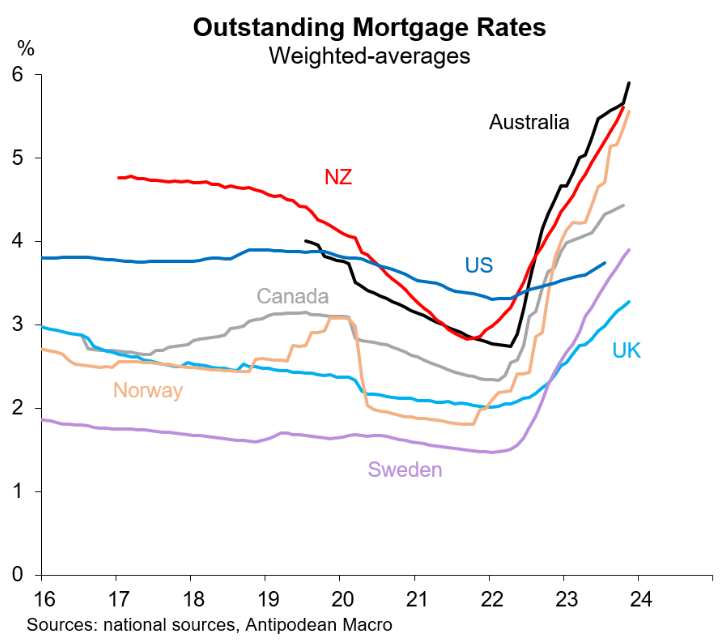

Justin Fabo at Antipodean Macro has posted the below chart showing how actual mortgage rates paid by Australians (blue line) continue to rise as cheap pandemic fixed-rate mortgages expire:

That said, the weighted average interest rate on outstanding housing loans has risen by about 1% less that the OCR since the RBA commenced its rate hiking cycle in early May 2022.

The gap between the average interest rate paid on outstanding housing loans (fixed and variable) is slowly closing with outstanding variable-rate loans as cheap fixed-rate mortgages expire.

However, this process has further to play out, meaning average mortgage rates will continue to rise even if the RBA keeps the OCR on hold.

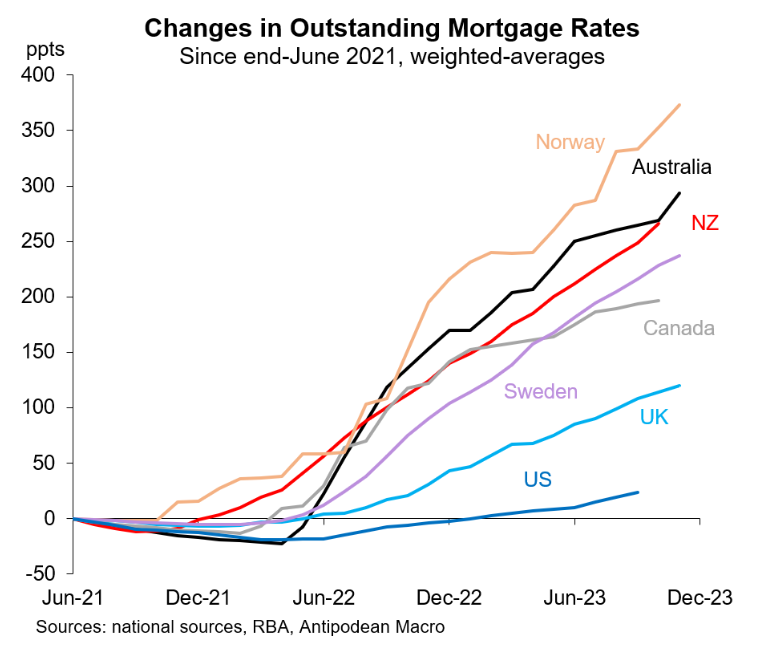

The following chart from Fabo shows that the increase in interest rates in Australia has been especially harsh, exceeded only by Norway:

The average outstanding mortgage interest rate in Australia is likewise relatively high:

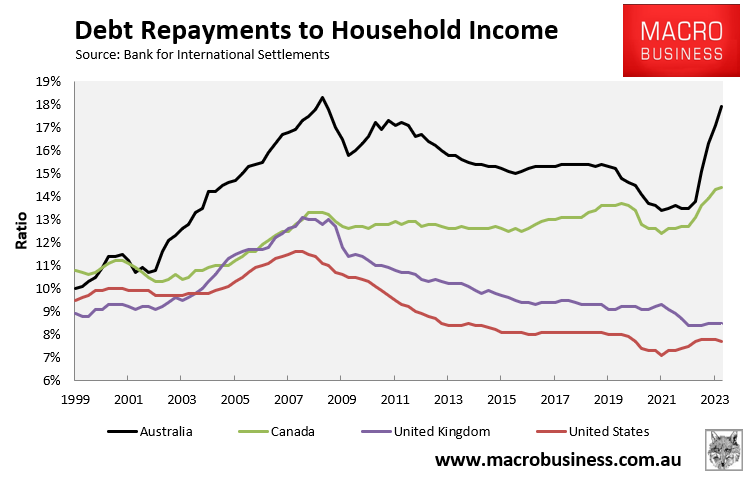

Separate data from the Bank for International Settlements (BIS) reveal that the aggregate share of household income going to debt repayments (i.e. both principal and interest) has risen especially quickly in Australia:

The data above show that Australia has one of the largest concentrations of variable-rate mortgages in the world.

This means that, while Australia’s OCR has risen less than in some other countries (such as New Zealand and the United States), the prevalence of variable-rate mortgages has resulted in Australia’s OCR being passed on to mortgage holders more swiftly.

These charts also explain why the RBA does not need to hike interest rates as aggressively to reduce demand and inflation.

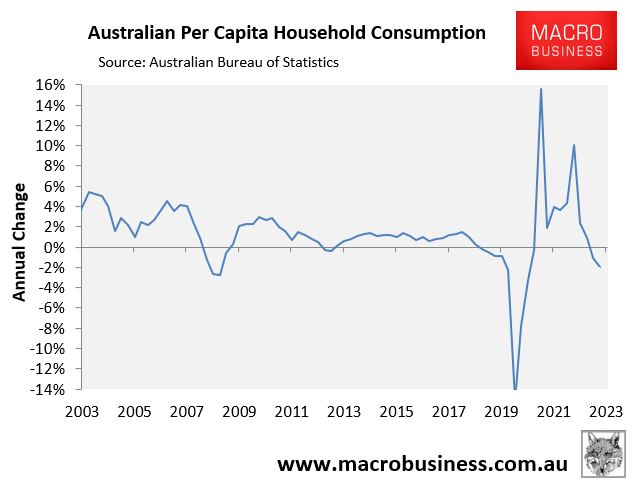

Australian households are already being hit hard, as evidenced by the BIS data above, as well as the national accounts data showing falling household consumption.