Australian house prices smash into affordability ceiling

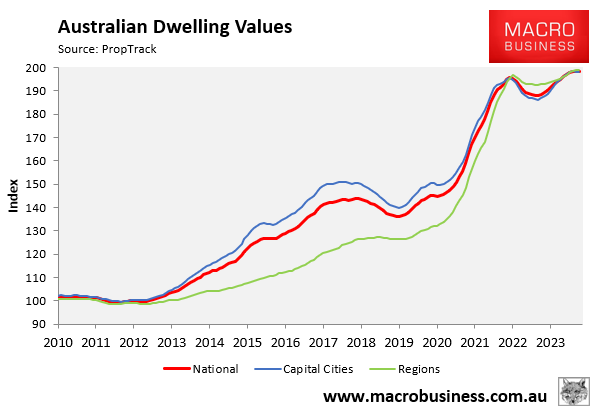

The latest dwelling results from PropTrack showed that Australian median home values retraced slightly from their record high to $823,000 across the combined capital cities and $760,000 nationally:

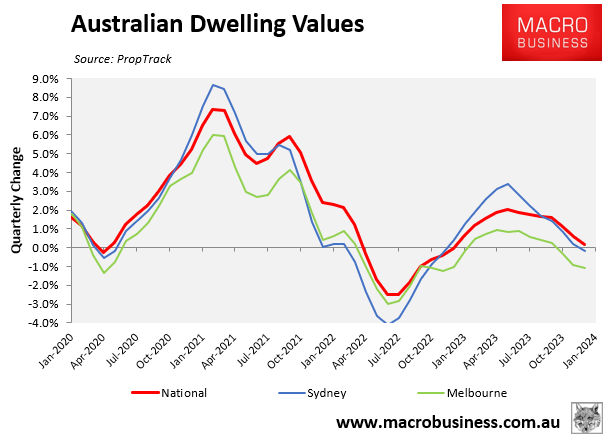

As shown in the next chart, quarterly dwelling value growth has fallen since the Reserve Bank of Australia (RBA) hiked the official cash rate (OCR) another 0.25% in early November, with national prices relatively unchanged since then:

PropTrack noted that “strained affordability – which sits at its worst level in at least 30 years – is likely weighing on home prices”.

However, PropTrack still “expect prices in 2024 will still grow, albeit at a slower pace than in 2023”.

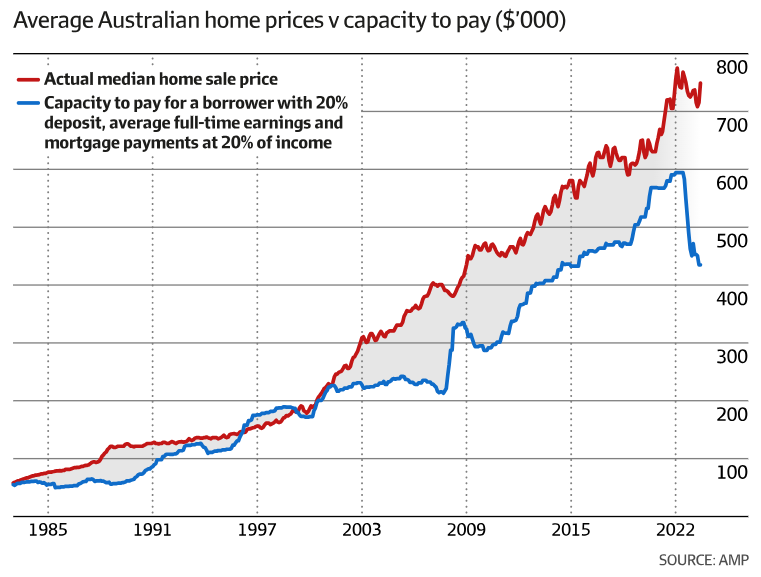

This strained affordability is illustrated in the next chart from AMP (published in The AFR), shows the record gap between median home prices and capacity to pay at the end of 2023:

This obviously reflects the combination of record dwelling prices and the sharp rise in interest rates, which has dramatically lifted mortgage serviceability requirements.

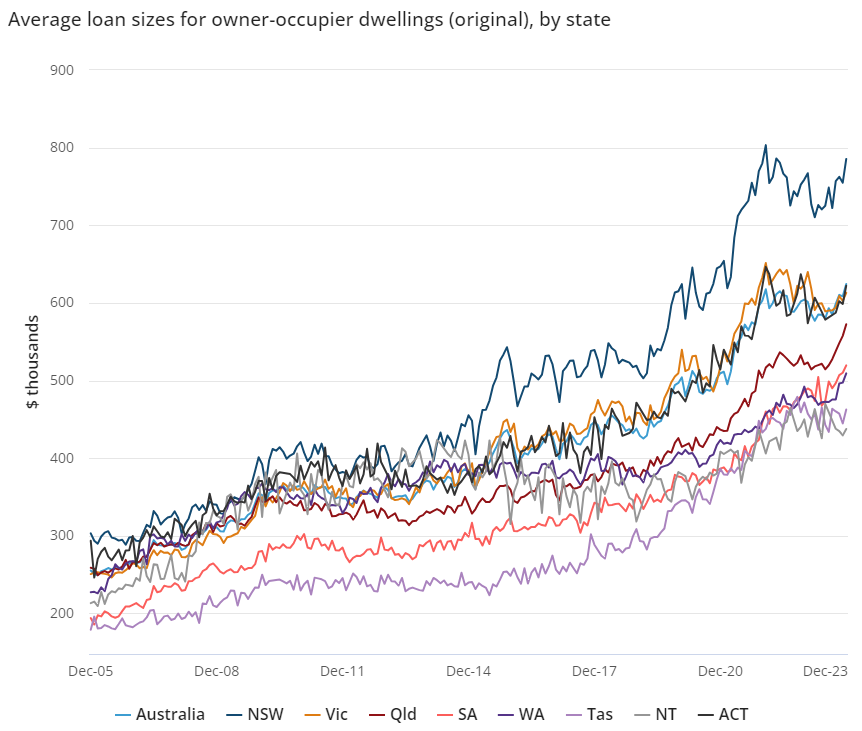

Friday’s Australian Bureau of Statistics’ (ABS) housing finance data also demonstrated stretched affordability.

The ABS presented the below chart, showing that average loan sizes for owner-occupier dwellings hit a record high $624,400 nationally in December, led by Sydney ($785,400):

Source: ABS

This $624,400 average loan size infers a monthly mortgage repayment on a 30-year loan of around $3,750 a month.

A borrower without lenders’ mortgage insurance would also need to provide an average deposit of around $150,000 to purchase the above home, which would take many years without parental help.

Despite historically high population growth and squeezed supply, this lack of affordability explains why Australian home values are likely to track sideways this year.

Prices probably won’t get a kick along until the RBA commences an easing cycle in the second half of this year, easing mortgage serviceability.

If you are looking to save thousands of dollars in mortgage repayments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute.

And if you choose to refinance, Compare n Save will handle the process.