Oddly, DXY fell after a red hot PPI:

The entire market pivoted back to value over growth. AUD pumped:

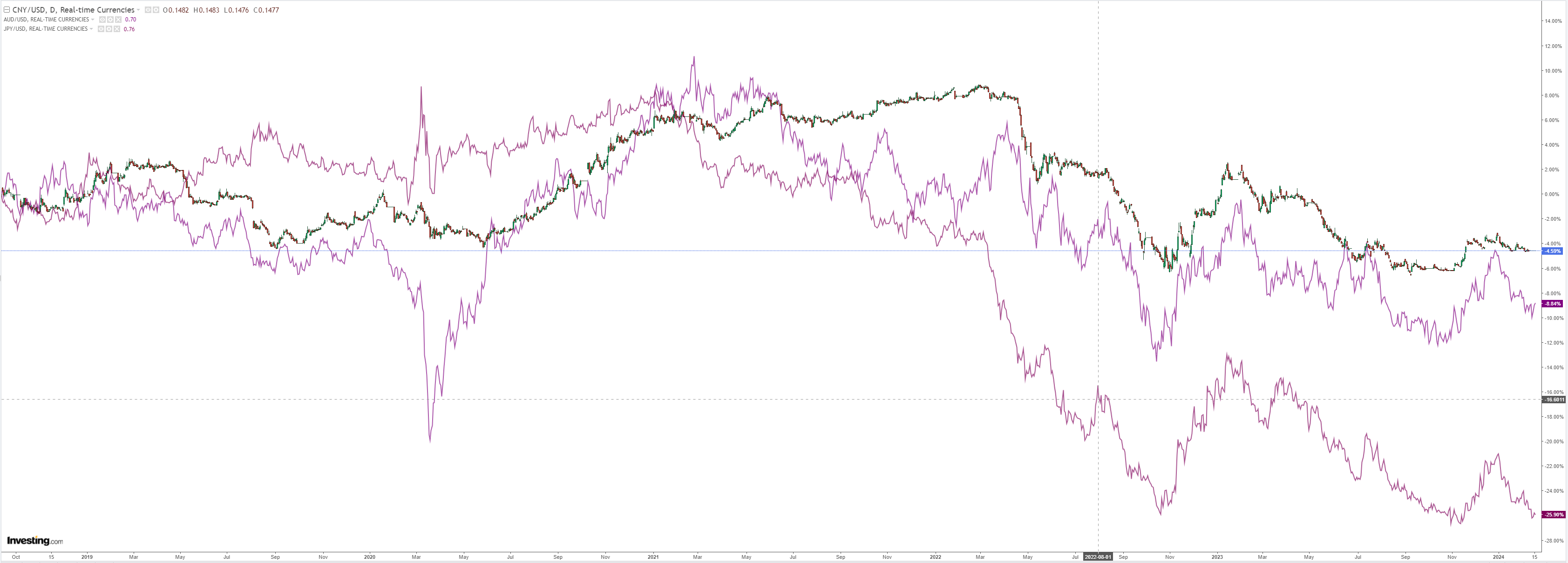

North Asia sleepy:

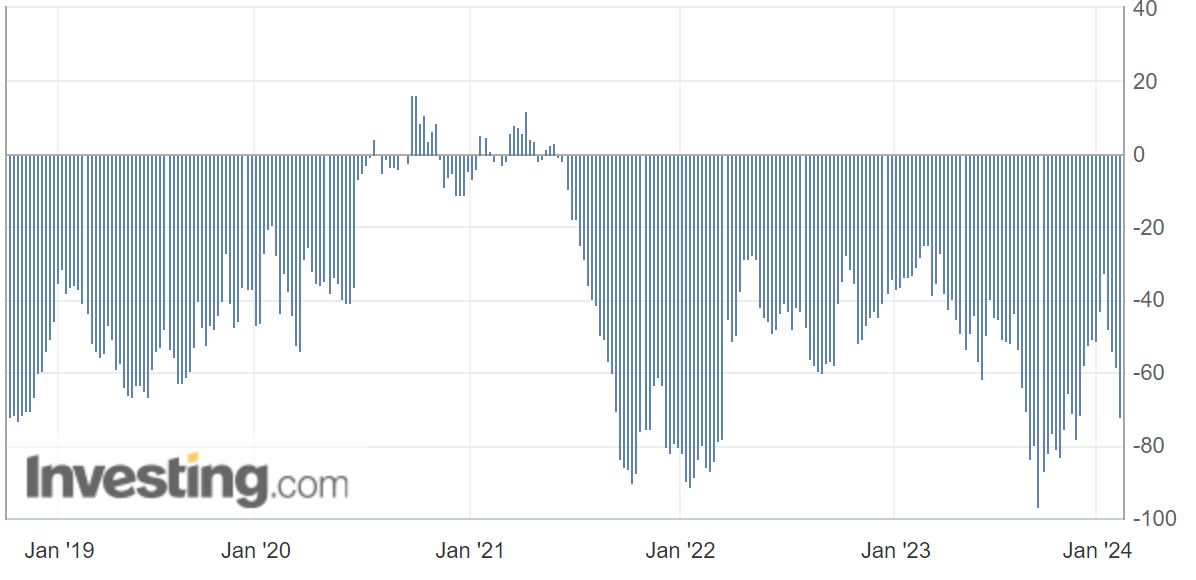

AUD bears have surged on CFTC. Hard for the currency to fall much now:

Oil is trending higher. Big trouble here if it rolls on:

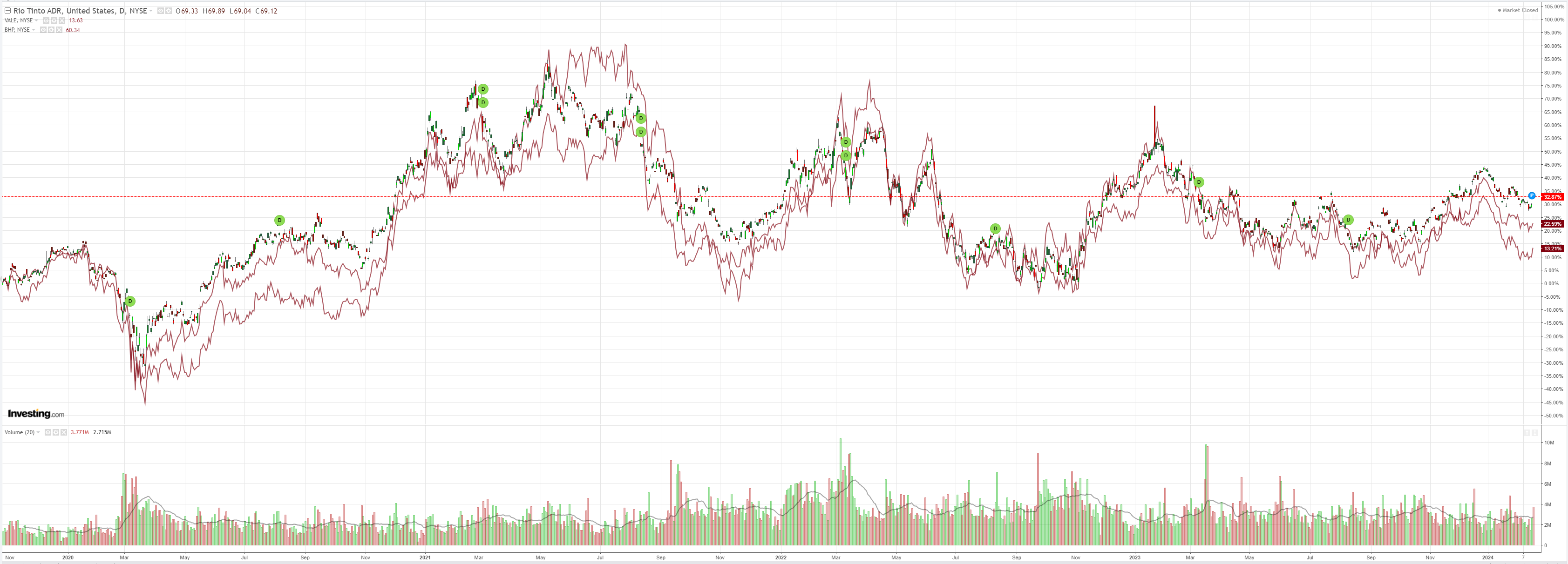

Dirt popped:

Miners too:

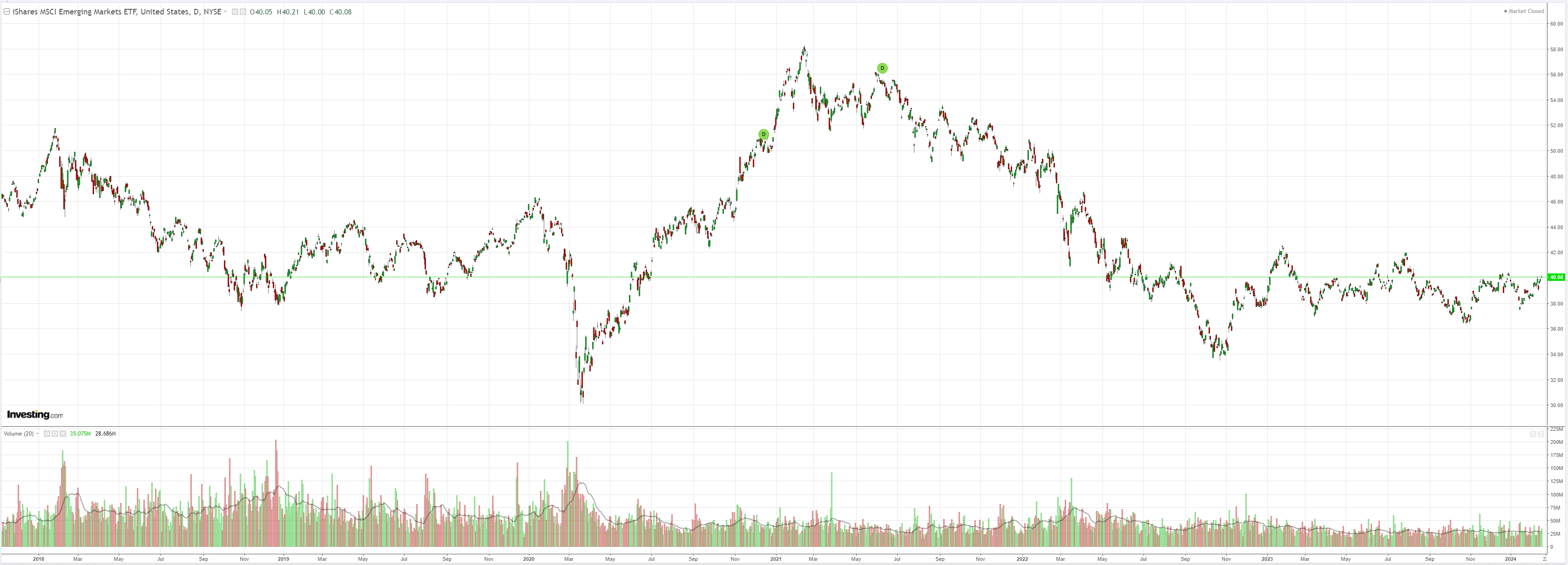

EM up:

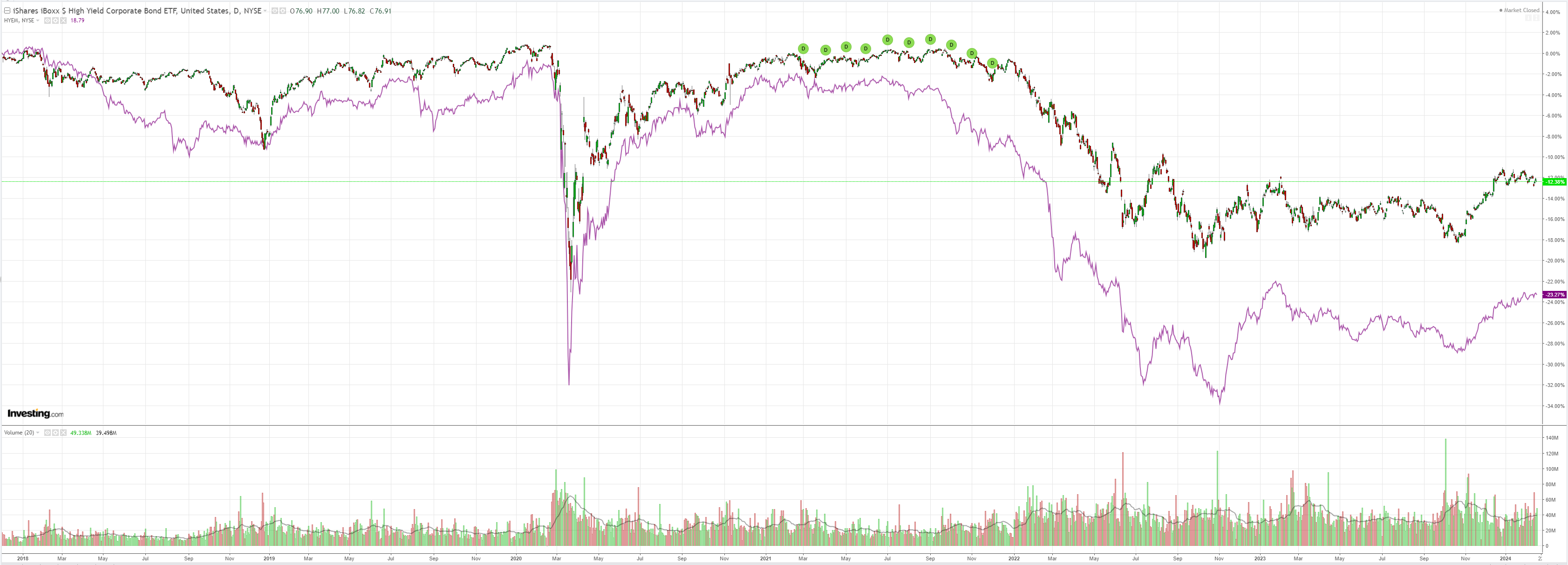

EM junk slowly closing the jaws with DM:

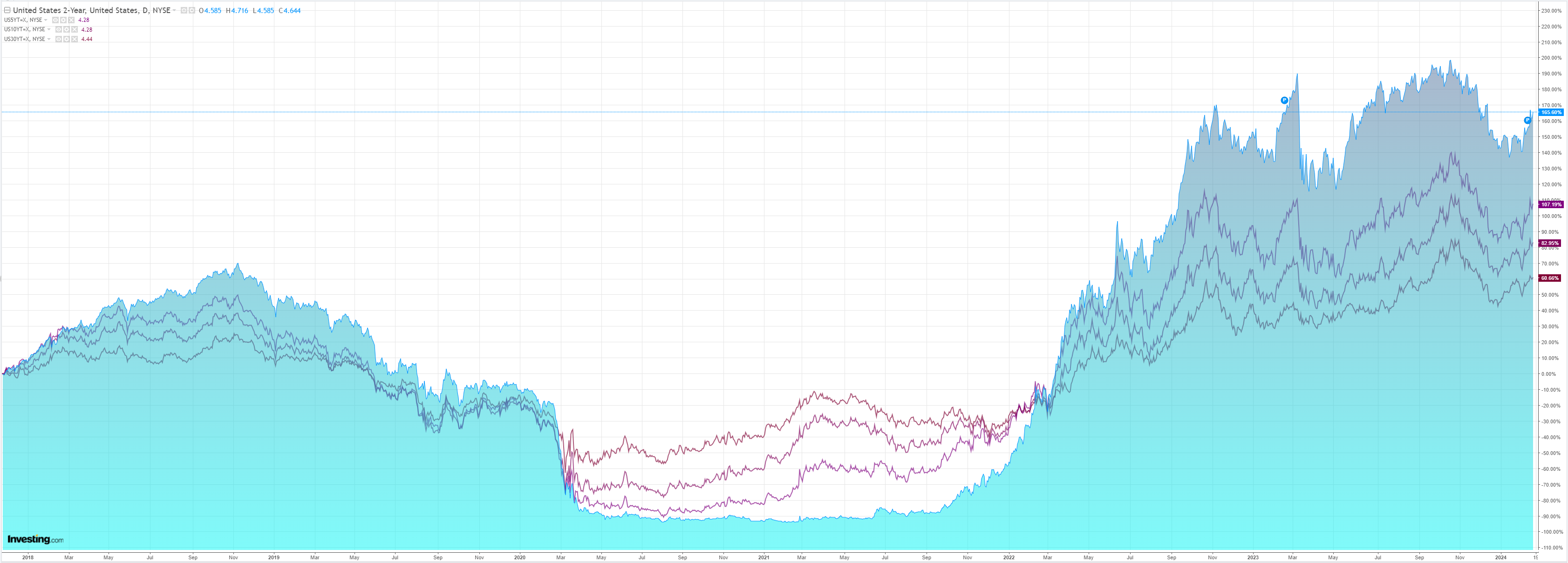

As yields rise:

And Mag7 falls:

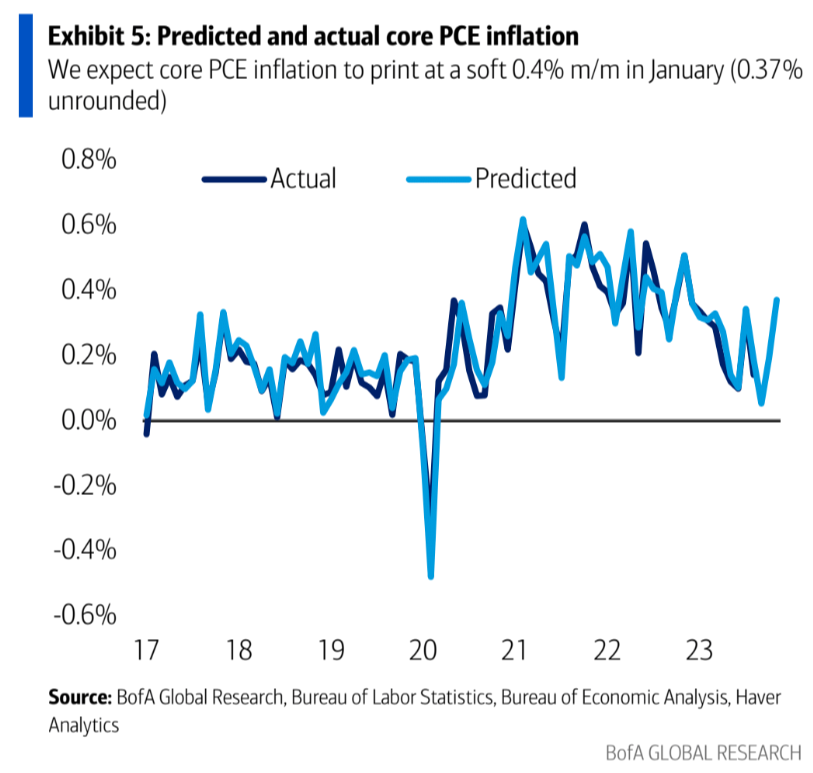

The US PPI was a shocker. BofA:

PPI tops expectations in January

Continuing the string on strong January inflation data, the Producer Price Index (PPI) topped expectations across the board.

Headline rose by 0.3%m/m(consensus: 0.1%), core increased by 0.5% (consensus: 0.1%) and core-core rose by 0.6% (consensus: 0.1%).

Core PCE likely to print at 0.4% m/m in January

Based on the January PPI and CPI (Consumer Price Index) data, we expect core PCE inflation to print at a soft 0.4% m/m in January (0.37% unrounded).

Given our forecast, we see risk that core PCE could round down to 0.3% m/m.

If our forecast proves correct, then the six-month annualized rate of core PCE would likely accelerate from 1.9% to 2.4% and the 3-month annualized rate would pick up from 1.5% to 2.5%.

Vindicated

The January inflation data vindicates the Fed’s wait-and-see approach.

Services inflation remains sticky, and the Fed would like to see more progress there to have confidence that inflation is returning to its 2% target on a persistent basis.

We still expect the Fed to start its cutting cycle in June when it will have four more CPI and employment reports.

January is usually a hot month for new year price rises. And, there were ironic price rises in finance derived from the bubble.

Even so, this is a bad print and gives the unlikely “no landing” scenario some legs.

While the market mulls this outcome, I can’t see how DXY falls. The overnight AUD bounce is idiosyncratic.

That said, so many bears on CFTC mean it is unlikely to fall much, either.