DXY is marking time:

AUD flopping around 0.65 cents:

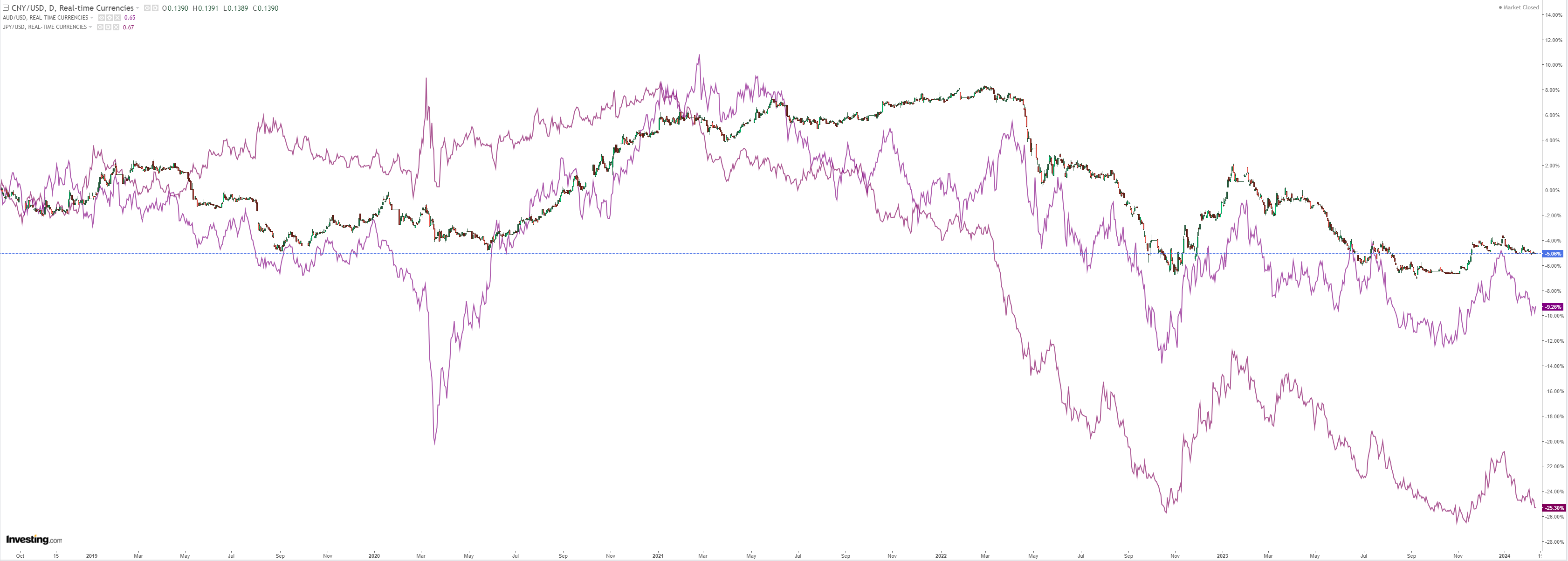

No support from North Asia:

Oil is still trying to warm up:

Dirt is being washed into the sea:

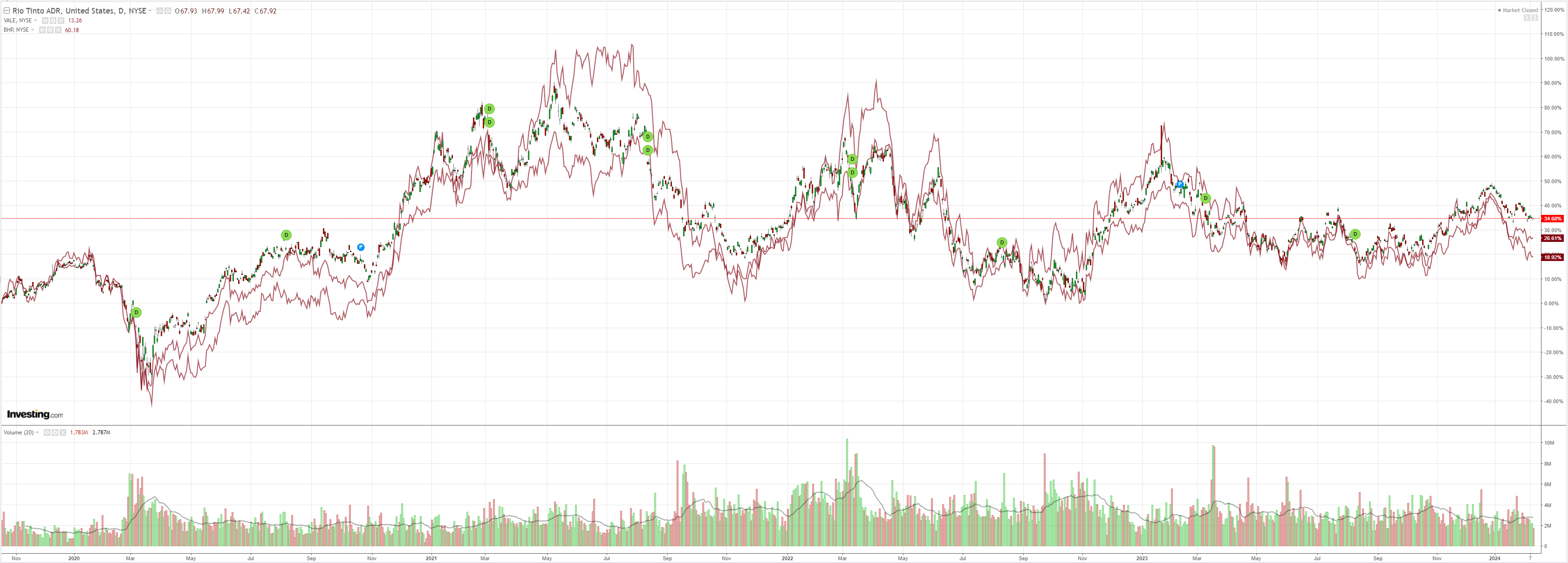

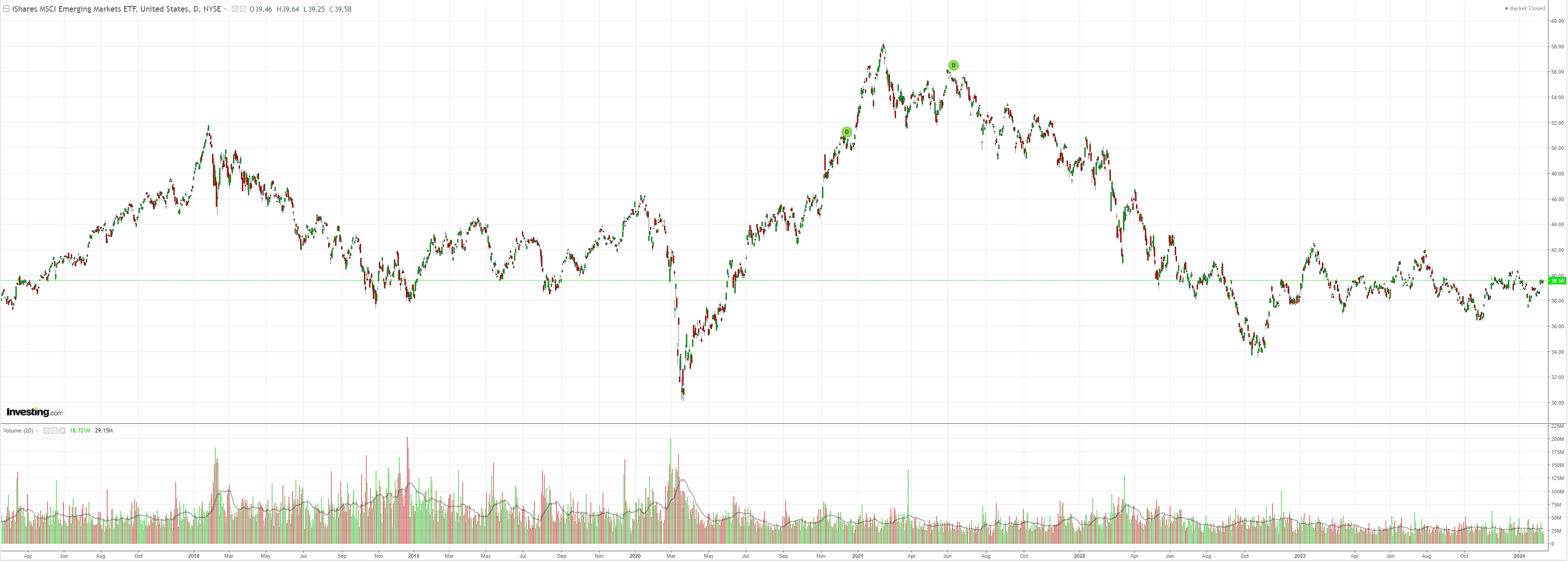

Big miners and EM yawn:

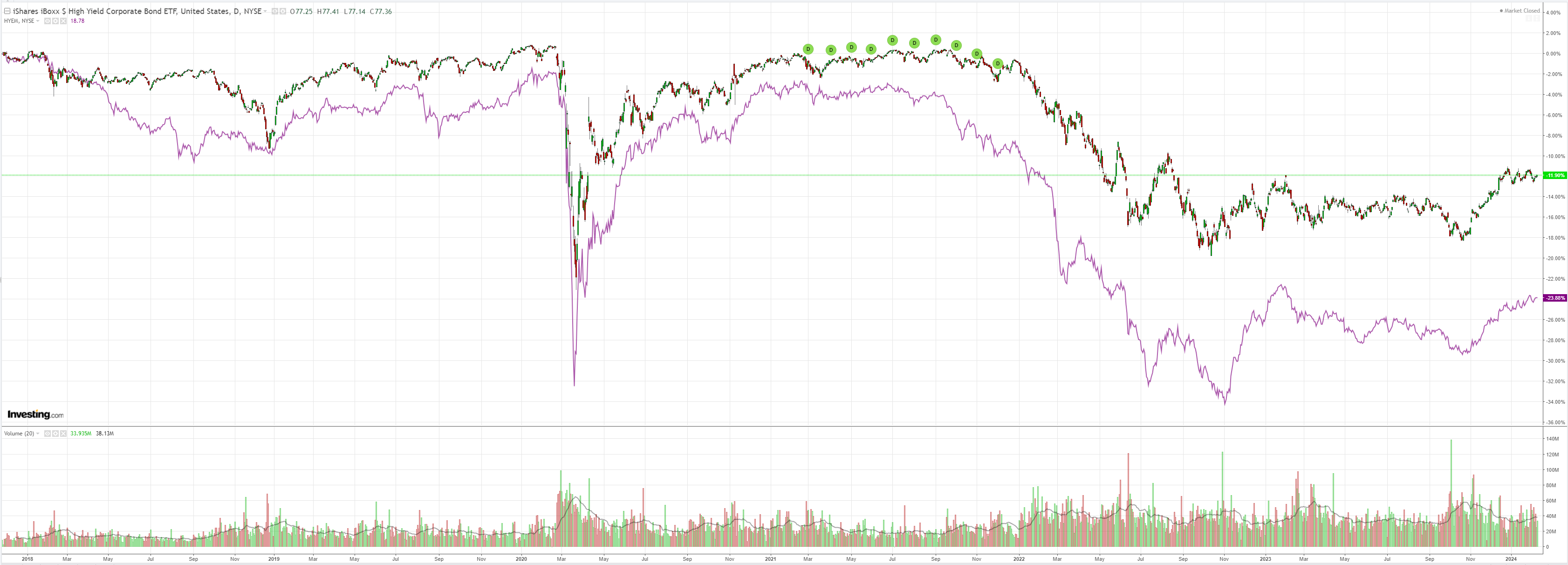

Junk needs to rev up for the rally. Nope:

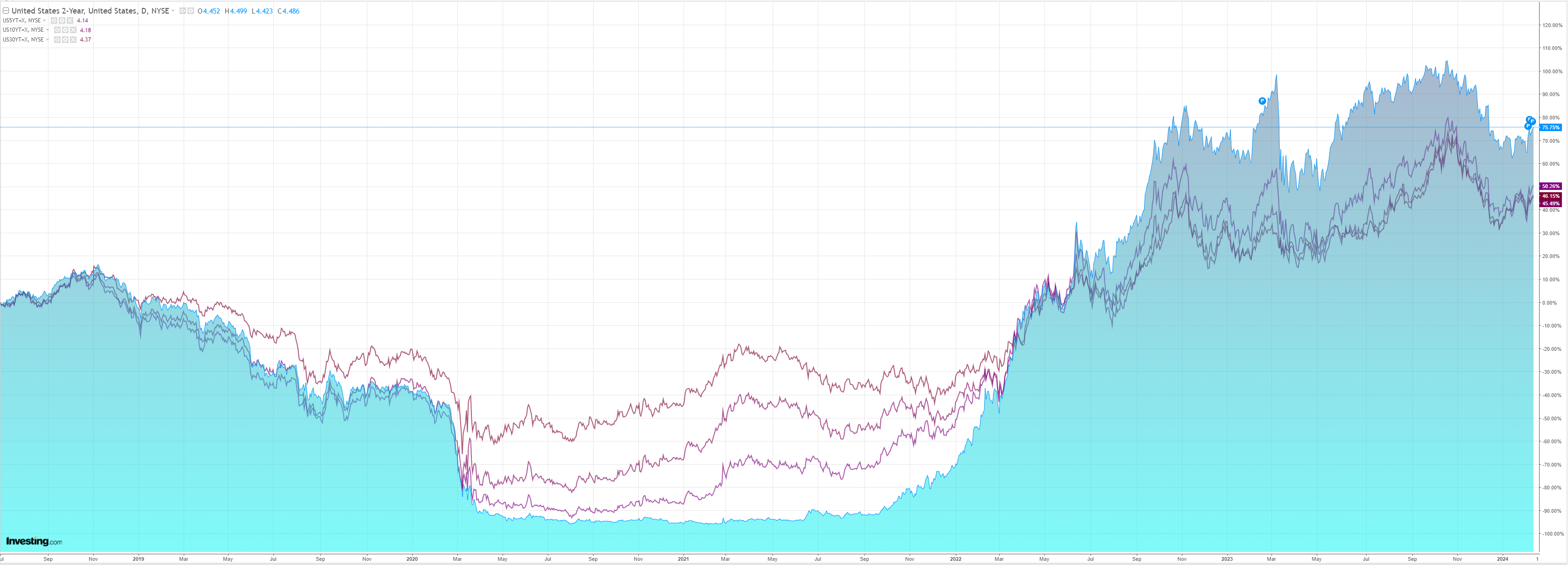

Treasury yields are instead:

As stock only straight up:

Goldman mulls the DXY:

USD: Divergent cycles, convergent cuts: Need a plan to get us out of here.

The DXY has gained a little ground since last week’s strong US payrolls report but has failed to build on momentum since earlier in the week.

There are two main issues holding the Dollar back.

First, the positive growth news has helped more cyclical currencies as recession risks relax further.

This is a key feature of our 2024 FX forecasts: Based on our robust growth expectations, the cyclical “flanks” of the FX market should perform relatively well.

Second, while Fed pricing has reset a bit, other markets have followed suit, with ECB pricing (for example) also moving almost in lockstep, despite further data disappointments.

As a simple summary measure, since we published our 2024 Outlooks 3 months ago, our economists have revised their US GDP forecast up by a full percentage point, while our Euro area tracking has fallen 2 tenths, but this has not translated into any meaningful divergence in the rate differential (Exhibit 1).

Until the cyclical divergence translates into policy divergence, FX will likely struggle to break out, with JPY a notable exception given its sensitivity to duration, and it is therefore no surprise to see the market focus on RV trade expressions in the meantime.

Consistent with the risks we flagged in our Outlook, we still think risks are tilted in the direction of a more resilient Dollar.

But, for FX to get a “fast car and a ticket to anywhere,” it will probably require the divergent cycle to translate into more divergent policy pricing.

As long as inflation keeps cooperating, and other policymakers seem more reluctant to drive ahead of the FOMC, then the broad Dollar “ain’t goin’ nowhere,” fast.

I disagree. In the current circumstances of imminent US cuts and reflation, DXY would typically be very weak. Instead, it is strong. Cyclically adjusted, DXY not going down is very impressive strength.

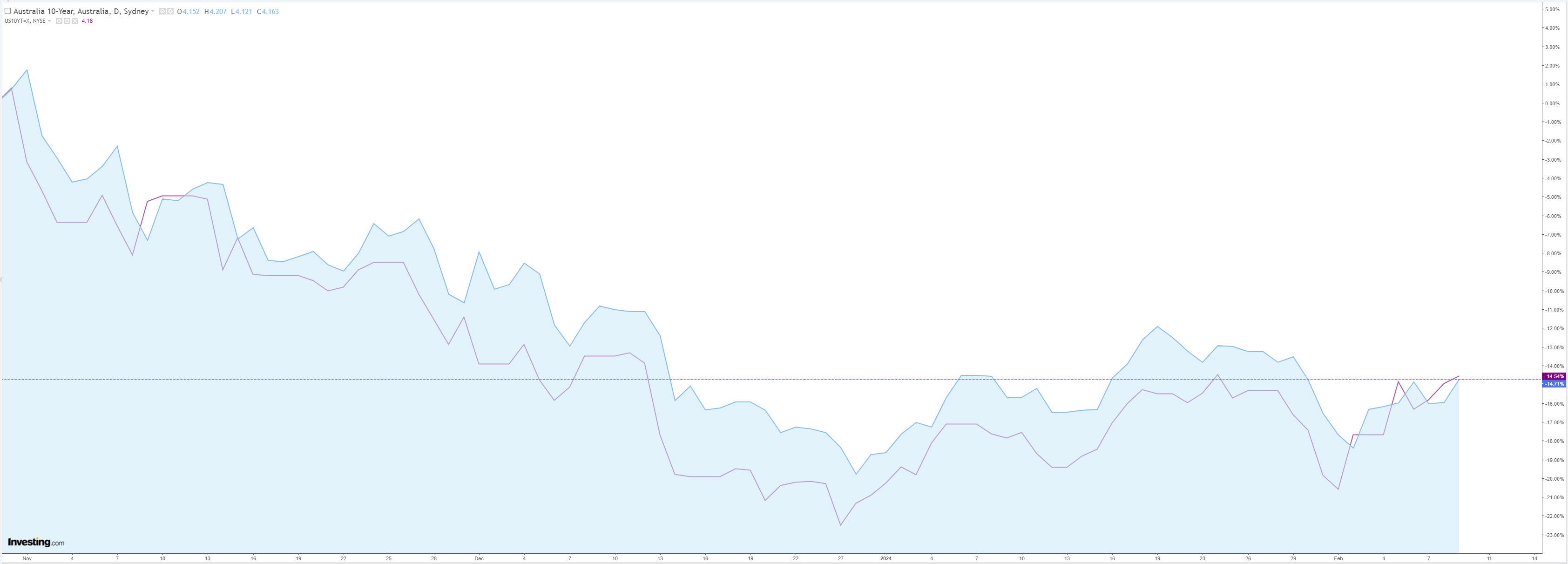

For Australia, Goldman’s policy divergence is a process that is well underway.

As Fed cuts have eased, RBA cuts have advanced. The move has so far been at the margin but there is more ahead.

The 10 year bond spread has shifted roughly 25bps in Australia’s favour since the rally started and is now inverted for the AUD:

As markets grasp that the Australian outlook is materially worse than that of the US, the downside risks remain on the front burner for AUD.