A great note from TS Lombard that gets it.

Time will tell if last week marked a local bottom in Chinese stocks, but the great unwind in China’s FDI and portfolio flows is just starting. The raft of measures put in place by Beijing to stem the market rout, including reports that Xi Jinping has been briefed on the markets and that the head of China’s markets watchdog has been fired, surely help. But structural drivers will continue to dominate the broad financial cycle. Here is a handy chart summary of our latest Global Financial Trends.

The “National Team” might get some traction now. But capital is structurally flowing out of China, chasing superior risk-adjusted returns, and to finance new “de-risking” agendas of the West and China’s own ambitions abroad (FDI). A Trump re-election can only intensify US-China de-coupling efforts; security concerns add to existing needs to re-shape supply chains; and Beijing’s aversion to a bailout of property/banking sector amid no progress on Common Prosperity reforms implies lower growth.

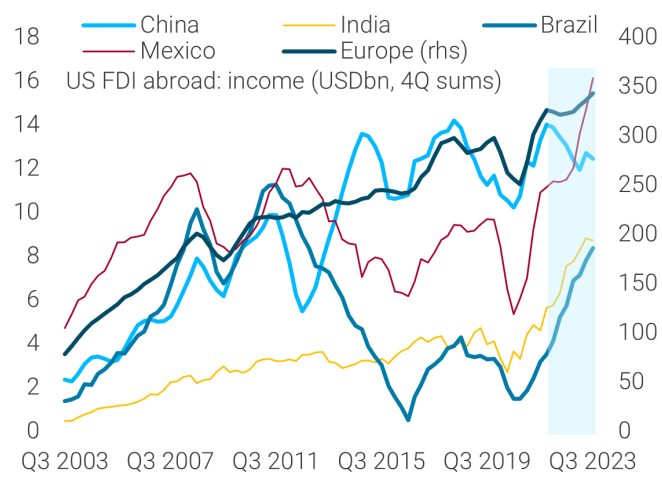

The map of global FDI flows has changed. Geopolitical and regulatory incentives coupled with the yawning gap in relative labour cost vis-à-vis China suggest that the allocation of new FDI has shifted away from China to DMs and other EMs. In EMs, South-East Asia, Mexico, India and commodity-rich LatAm are FDI winners.

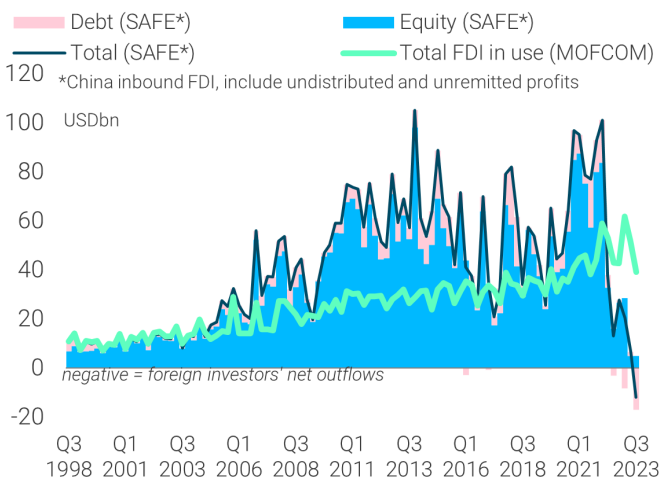

SAFE net FDI flows (of which firms’ reinvested profit is a large part) are well correlated with the spread between 10y CGB and UST yields. More stable MOFCOM figures could suggest FDI outflows are temporary, as large profit repatriation is just a reflection of foreign firms optimizing liquidity management. But rate differentials are working as an accelerator for the above underlying drivers, which started to operate at the same time and will continue in the medium run.

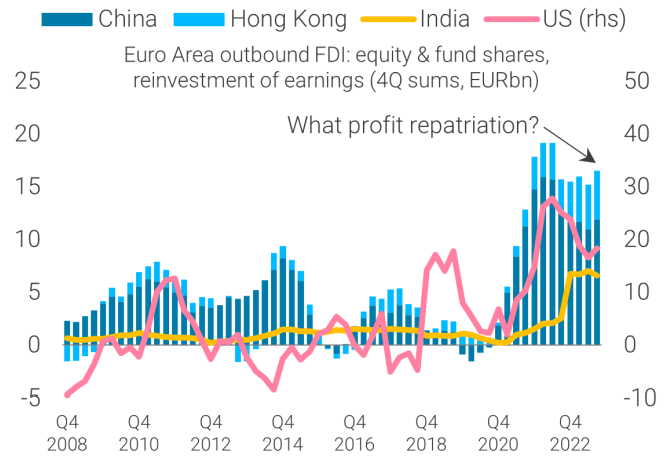

US and EA BoP data provide still limited evidence of profit repatriation from China to DMs, outside US firms. Despite talk about “de-risking” and some encouraging diversification into India, EA firms remain reluctant to reduce China exposure. Unsurprisingly, German firms account for the bulk of EA reinvestments, in line with their aversion to leaving their largest market. To us this means that the financial restoring process is still in its infancy and has significant room to intensify.

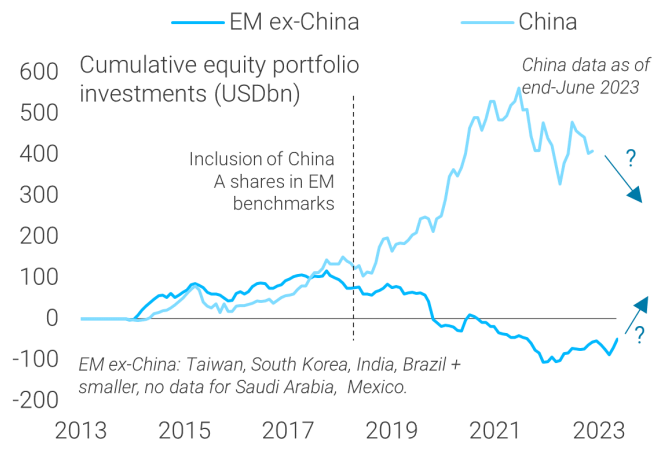

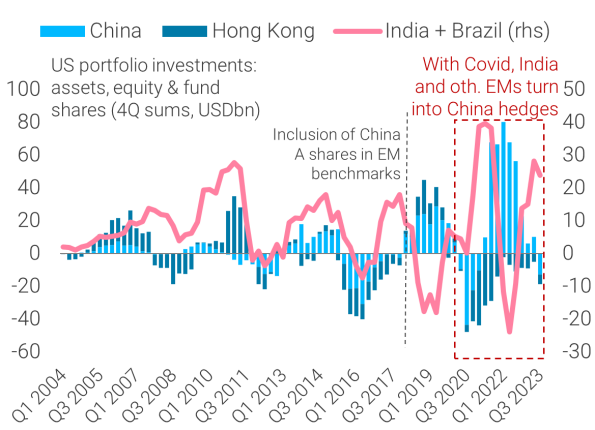

Portfolio flows are more volatile and subject to price action and momentum. So, recent intervention by authorities could spark a rally in the short term. But Beijing’s refusal to deploy structural stimulus – the “bazooka” markets have been waiting for – implies that the reversal of the huge China equity inflows started in 2018-19 with the inclusion of “A shares” into EM benchmarks has likely further to run. Investors without strict mandates are trimming their China exposure.

US and EA financial account data provide early evidence of these dynamics. For example, prior to 2018-19, US residents’ equity portfolio flows into China and other major EMs like India and Brazil were positively correlated, but since then the correlation has flipped. Moreover, since Covid, EM ex-China, and especially India, have effectively worked as a China hedge.

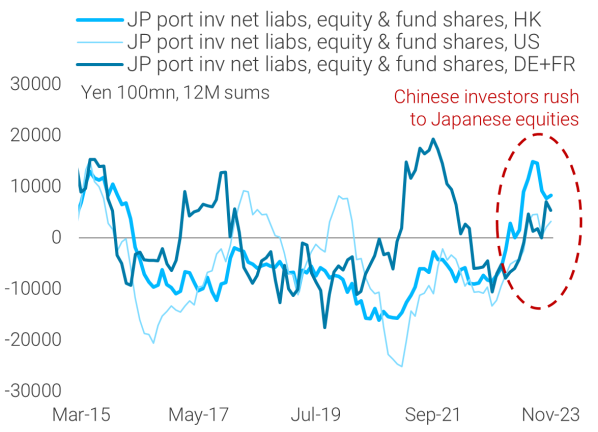

Meanwhile, Chinese investors have not been sitting on their hands with losses piling up. In fact, since early 2023 inflows from Hong Kong into Japanese equities have been larger than those from the US and EA. US tech has been another top pick for Chinese investors. Real-time data from the largest ETFs available to onshore China investors show a massive increase in assets for Nasdaq index trackers.

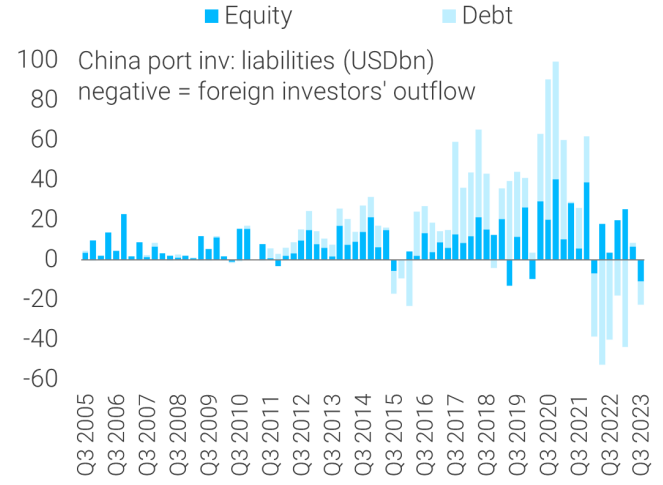

Meanwhile, the widening rate differentials between China and the rest of the world except Japan implied that debt portfolio outflows ballooned too. To be sure, global central banks will cut rates in the next year or two, but global rates will remain high, the differential with China big, and a significant reversal of such debt outflows unlikely.

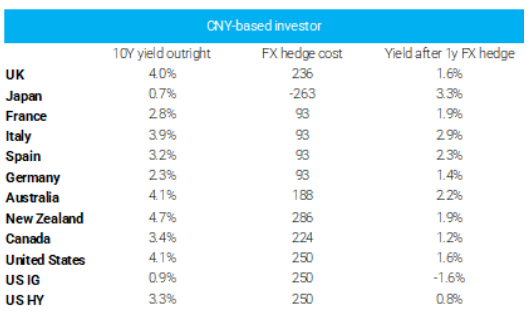

Finally, capital flows will have an impact on the RMB. In the short run, this depends on how much of Chinese domestic unhedged outflows is likely to return home (foreign investors have been paid to hedge CNY). But rising odds of a Trump victory and fears of renewed US-China tensions will weigh on the yuan, China growth and portfolio flows – hedged or unhedged. In the longer run, sustained capital outflows from China will contribute to further downward pressure on the RMB.

Albo the Idiot has yoked Australia to the world’s fastest and largest sinking ship.