Everybody with a brain is shifting away from China:

Years of harrowing losses have left Chinese stocks with a diminished standing in global portfolios, a trend that’s likely to accelerate as some of the world’s biggest funds distance themselves from the risk-ridden market.

An analysis of filings by 14 US pension funds with investments in Chinese stocks show most of them have reduced their holdings since 2020. The California Public Employees’ Retirement System and New York State Common Retirement Fund, among the nation’s biggest pension investors, cut their exposure for a third straight year.

What started out as a performance-driven exodus now risks becoming a structural shift due to a toxic combination of doubts over Beijing’s long-term economic agenda, a prolonged property crisis and strategic competition with the US.

Add the tyranny and support for Russia, plus invasion into core European export markets, plus Taiwan tensions, and you have the deglobalisation perfect storm.

We have the mighty Xi Jinping to thank for it. And Aussies, in particular, should be grateful that he is prepared to do what Canberra is not.

The unstoppable Chinese economic winddown has stalled Aussie export growth even as Albo prostrates himself to restore it.

Even better, the structural slowdown will shift the export share away from China much further yet as bulk commodities deflate and shift to Africa for the next decade:

I have often noted the bizarre habit of Beijing acting inadvertently in the Australian national interest while all Canberra wants to do is sell itself to the same.

Canberra is like a whore compulsively forcing ourselves upon a pimp who recoils in disgust

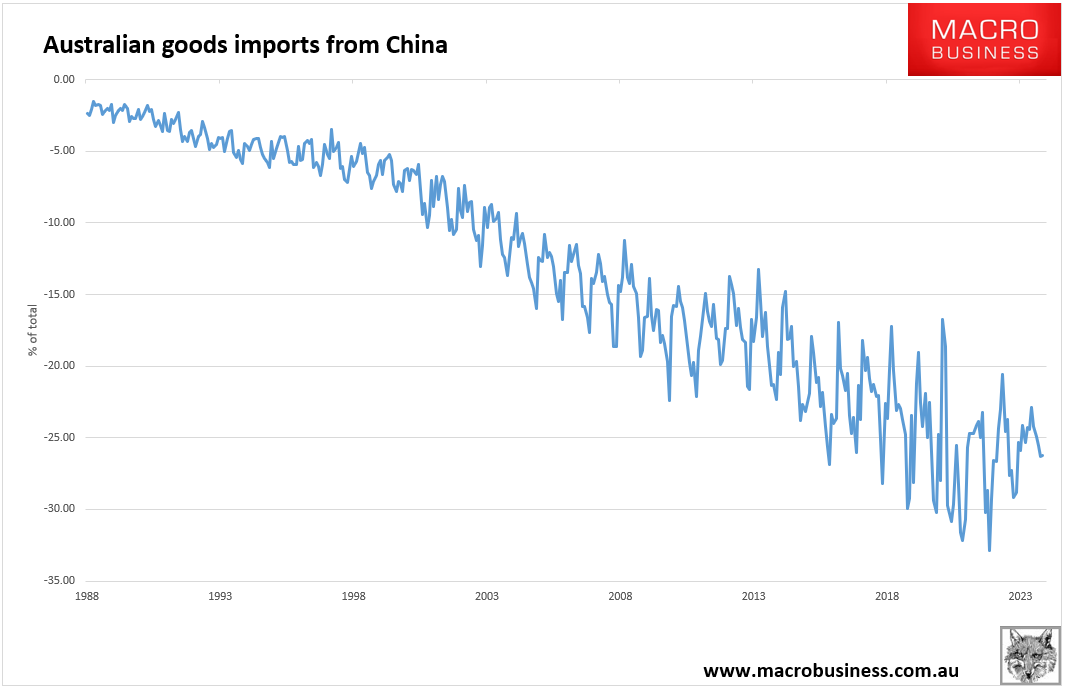

Sadly, the story on imports is less sanguine. They have likewise stalled, but this is a demand story, and the trend to greater dependence is not yet decisively broken:

If Australian domestic demand recovers, the Chinese import share will grow because Albo has no re-industrialisation policies to stop it.

This is another Albanese Government policymaking shocker.

China is derisking its critical supply chains with Australia. Meanwhile, our dependence upon Chinese supply chains deepens, maximising our economic and political vulnerability.

In the event of this:

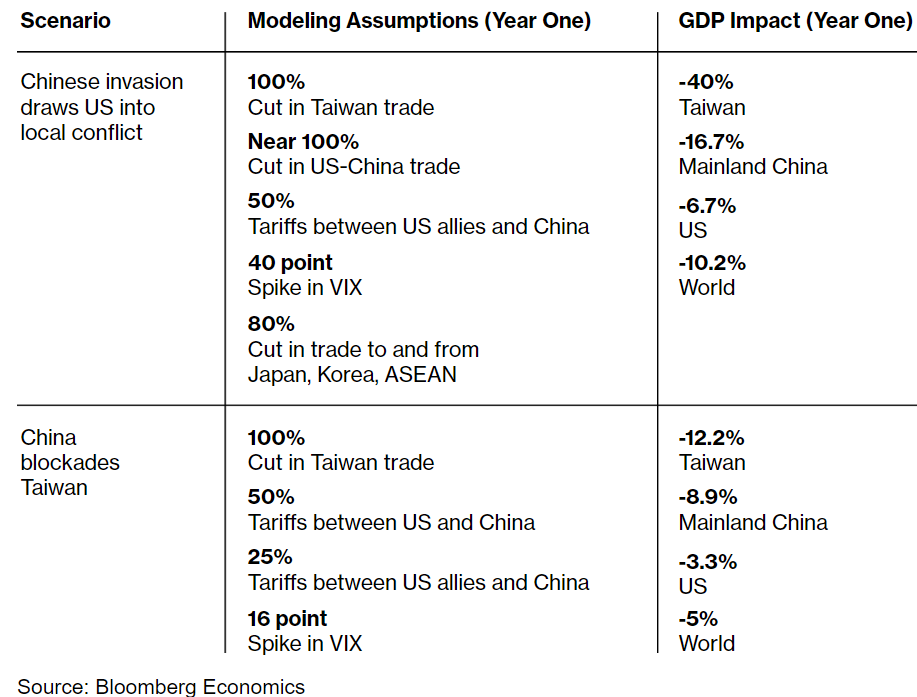

War over Taiwan would have a cost in blood and treasure so vast that even those unhappiest with the status quo have reason not to risk it. Bloomberg Economics estimate the price tag at around $10 trillion, equal to about 10% of global GDP — dwarfing the blow from the war in Ukraine, Covid pandemic and Global Financial Crisis.

Taiwan makes most of the world’s advanced logic semiconductors, and a lot of lagging edge chips as well. Globally, 5.6% of total value added comes from sectors using chips as direct inputs — nearly $6 trillion. Total market cap for the top 20 customers of chip giant Taiwan Semiconductor Manufacturing Co. is around $7.4 trillion. The Taiwan Strait is one of the world’s busiest shipping lanes.

Bloomberg Economics has modeled two scenarios: a Chinese invasion drawing the US into a local conflict, and a blockade cutting Taiwan off from trade with the rest of the world. A suite of models is used to estimate the impact on GDP, taking account of the blow to semiconductor supply, disruption to shipping in the region, trade sanctions and tariffs, and the impact on financial markets.

For the main protagonists, other major economies, and the world as a whole, the biggest hit comes from the missing semiconductors. Factory lines producing laptops, tablets and smartphones — where Taiwan’s high-end chips are the irreplaceable “golden screw” — would stall. Autos and other sectors that use lower-end chips would also take a significant hit.

Barriers to trade and a significant risk-off shock in financial markets add to the costs.

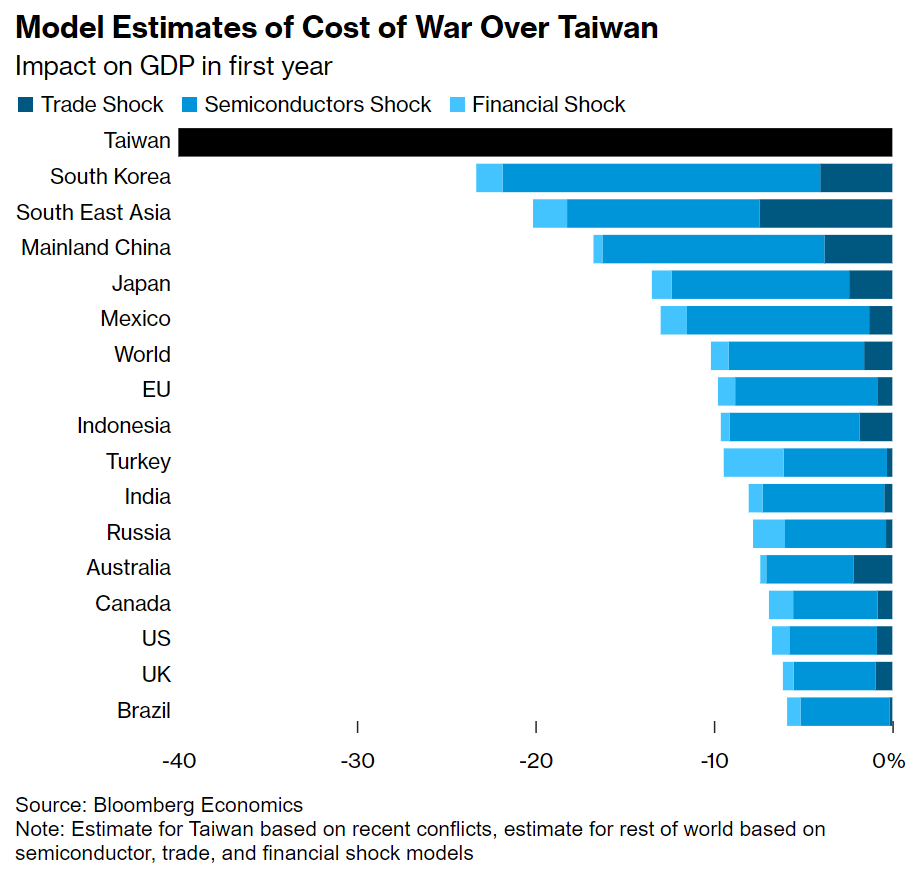

There is no way on this earth that EU and Mexico would do worse than Australia in a Taiwan war.

I’m guessing the Bloomberg model does not model a halving of Australian house prices as trade blockades destroy national income and consumption.

Failing to hedge this risk at all is another Mad Albo special.