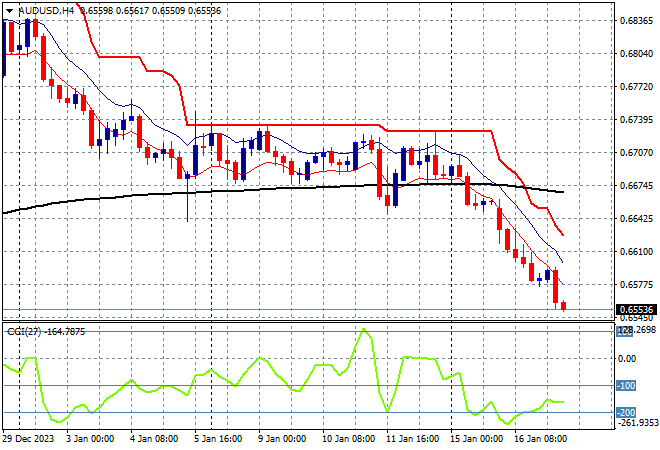

The latest Chinese GDP growth figures came in softer than expected and sent mainland and offshore markets a lot lower in response, coupled with a higher USD that isn’t helping other risk markets. The Australian dollar is maintaining a straight pulldown throughout today’s session, now extending into the mid 65 cent level as we head into the London sessions.

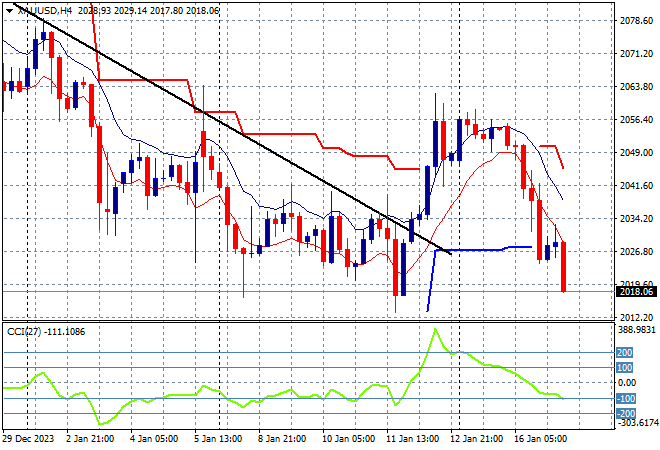

Oil prices have stalled again with Brent crude still slightly above the $77USD per barrel level but going nowhere while gold has returned to its previously weekly low as it now dices with the $2000USD per ounce level:

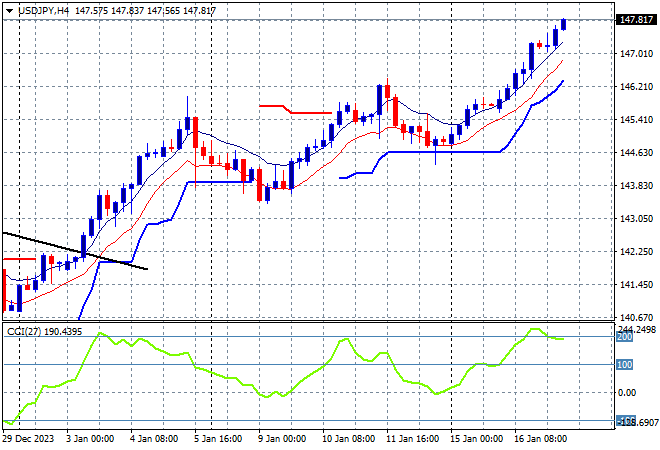

Mainland Chinese share markets are pulling back again as the Shanghai Composite again rejects the 2900 point barrier, falling more than 1% to 2859 points while in Hong Kong the Hang Seng Index has collapsed again, down more than 3.5% to 15311 points. Japanese stock markets are now in a two day retreat with the Nikkei 225 down nearly 0.4% to 35447 points while the USDJPY pair has another attempt at breaking out above the 146 level:

Australian stocks are still failing to gain any positive momentum, with the ASX200 losing more than 0.3% to now push below the 7400 point level, closing at 7393 points. Meanwhile the Australian dollar also brokedown further after slipping through the 67 handle on the weekend gap and is now threatening the 66 cent level:

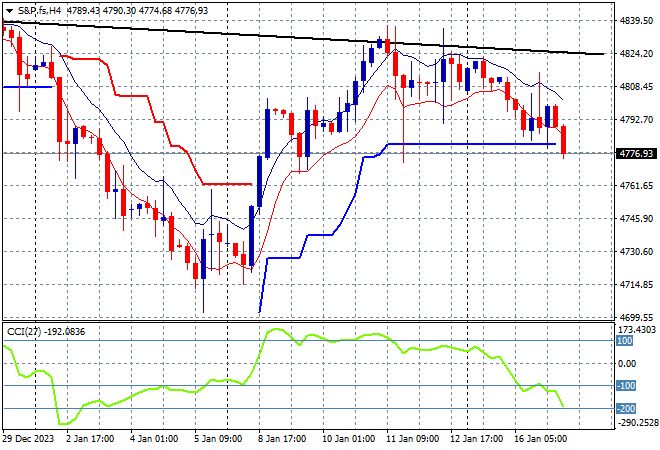

S&P and Eurostoxx futures are pulling sharply in unison with Asian shares the S&P500 four hourly chart showing a retracement well below the 4800 point level which is no longer acting as support going into tonight’s session:

The economic calendar will focus on the latest UK and Euro inflation prints, then US retail sales.