Advertisement

Westpac with the note.

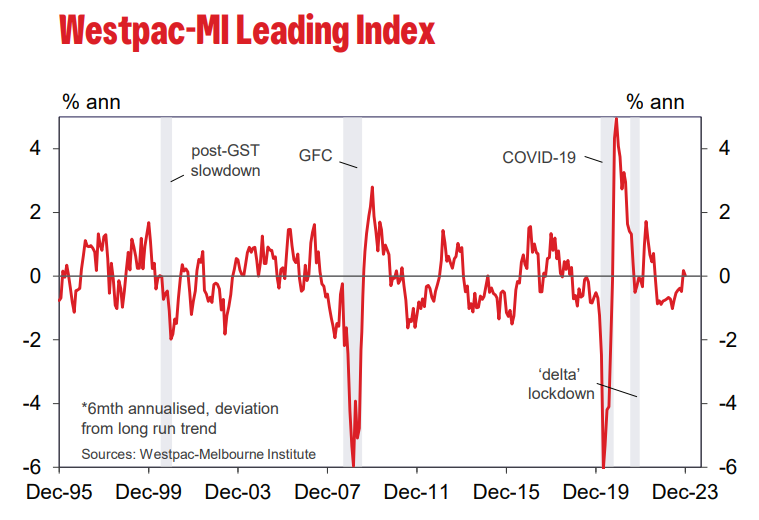

Despite the dip back into year-end, the Leading Index growth continues to show a clear improvement. December is the second consecutive month that the Index growth rate has been around or slightly above the zero ‘gain line’. That follows fifteen consecutive months of negative, below trend reads, mostly in the –0.5–1% range.

Advertisement

However, the broad picture still looks to be of, at best, a stabilisation rather than the beginning of a cyclical upturn. Much of the lift is coming from a recovery in commodity prices since mid-2023, a rally that may not last. Meanwhile momentum excluding this component still looks to be weak.

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.