DXY is breaking higher:

AUD is still weak:

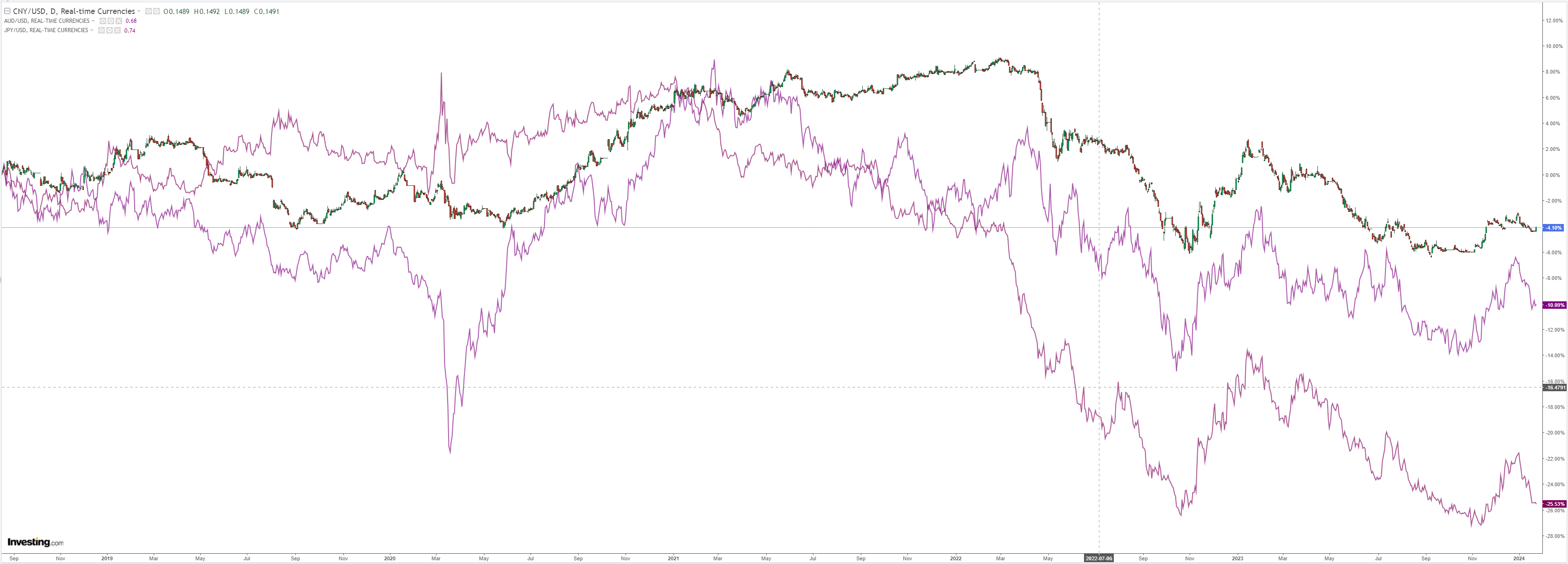

CNY popped for a day on the stock rescue. JPY didn’t:

Oil is grinding higher:

Was it a Chinese stock or dirt rescue?

EM yawn:

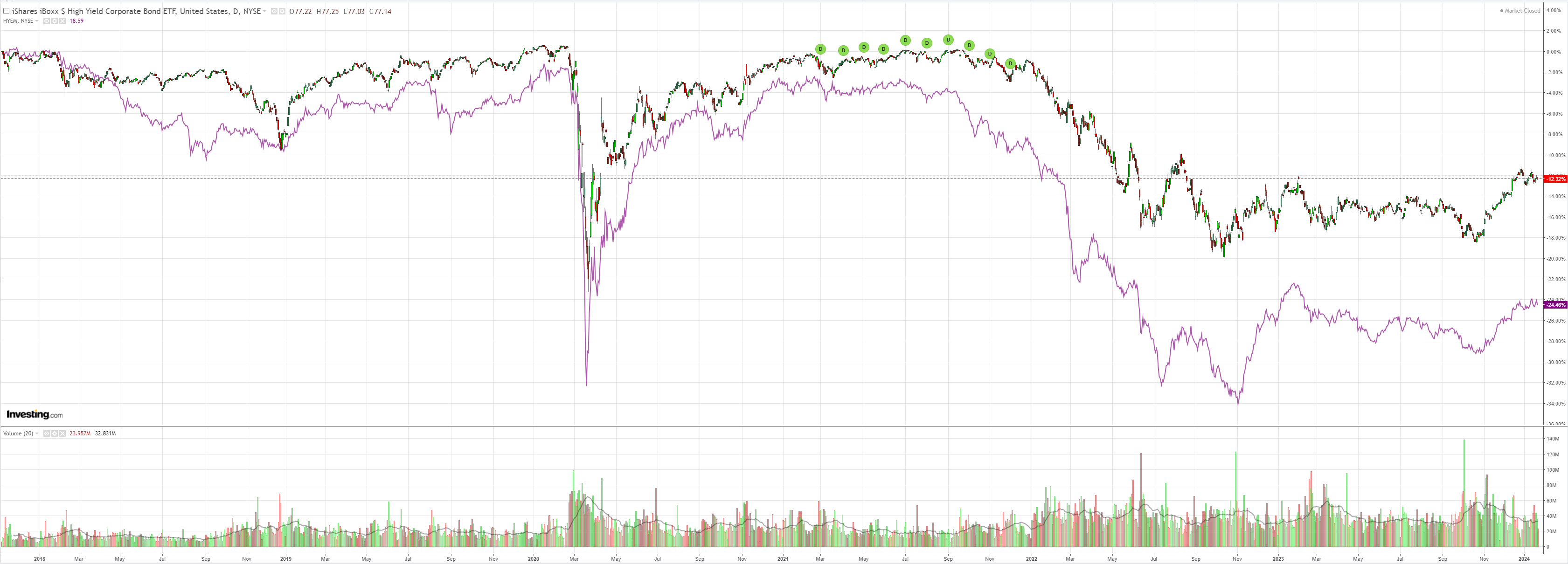

Junk spreads are deteriorating:

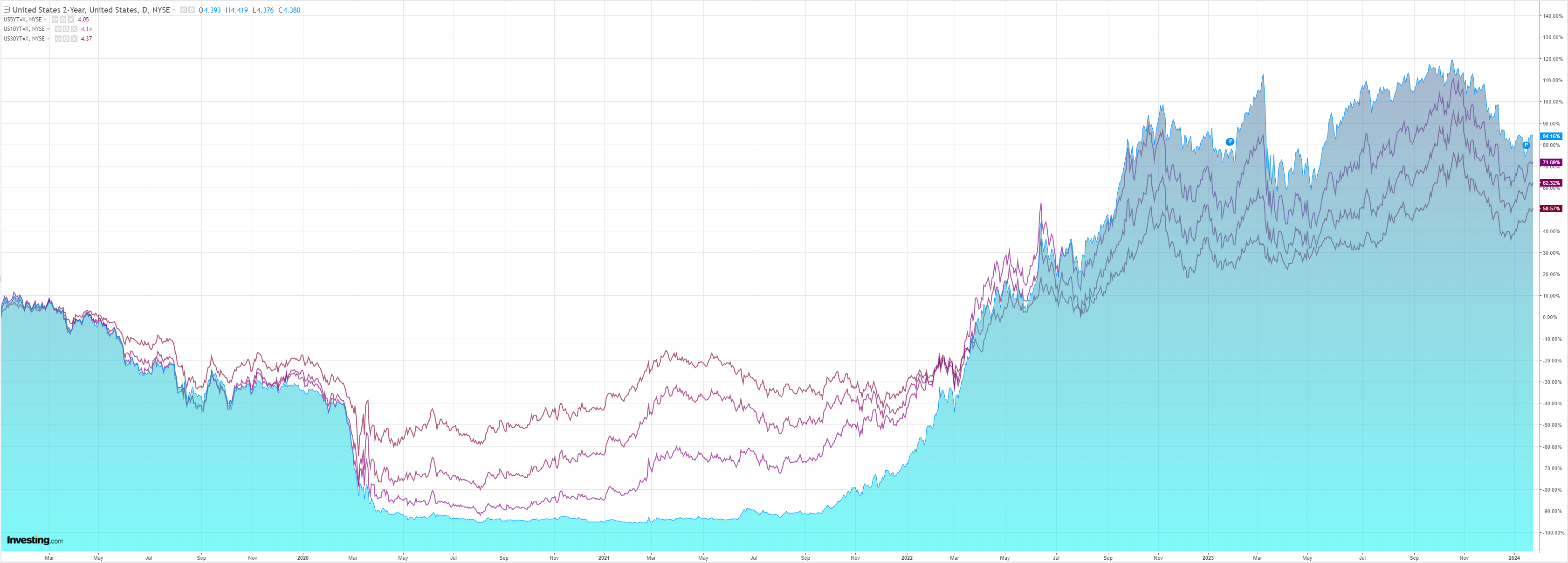

As yields rise:

This will eventually stop stocks from going up:

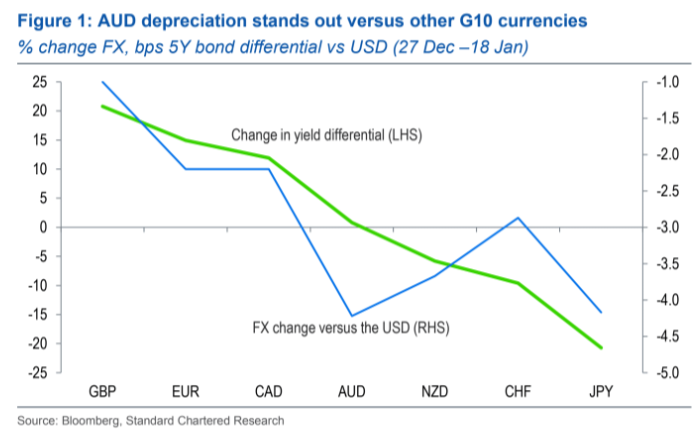

Standard Chartered says AUD is oversold:

All G10 currencies have dropped versus the USD since 27 December, which was the recent low for both the USD and US 5Y UST yields.

Investors have largely focused on US yields and FOMC cutting probabilities.

We find a regular relationship between changes in yield differentials versus 5Y UST yields and currency moves with a couple of exceptions.

First, the AUD has been much weaker relative to its yield differential move than the other G10 currencies that we cover (Figure 1).

We like long AUD-NZD given the NZD outperformance relative to its yield move, and fewer confounding factors to throw off the yield/FX relationship.

There is also a case for outright AUD versus USD given the 4.2% depreciation while yield differentials were holding steady.

That is more risky as it would require US economic data to cooperate and trigger broad USD weakness.

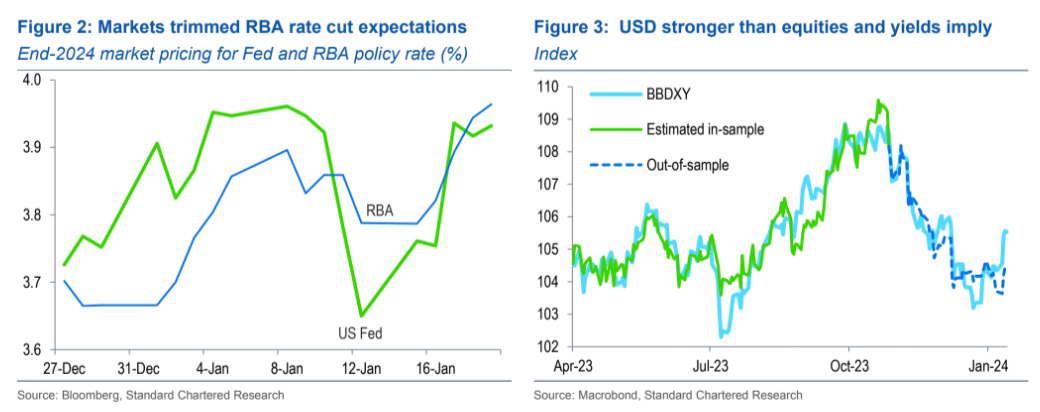

While Australia’s economic data have surprised to the downside in recent weeks, we doubt they offer significant explanatory power for the AUD’s underperformance.

For one, the AUD has been an underperformer in the G10 complex prior to the release of November CPI (10 January) and December labour market report (18 January).

If anything, markets have almost halved RBA rate cut expectations in 2024 to 38bps from 68bps compared to the Fed (160bps to 140bps), which should be supportive for outright AUD against USD.

Said differently, markets expect end-2024 RBA cash rate to exceed that of the Fed (Figure 2)

It is obvious that the bearish sentiment pouring out of China is holding back AUD versus yield spreads.

I think rate cuts are coming sooner and deeper to Australia as well.

The base case for AUD remains a grind higher as the FEd begins to cut, but it’s going to be a hard slog, and it may already be largely over.