DXY is still consolidating:

AUD likewise:

The North Asian dogs are a big headwind for AUD:

AUD positioning is killing off the bears quick smart:

Oil rose but not much, given the flying missiles:

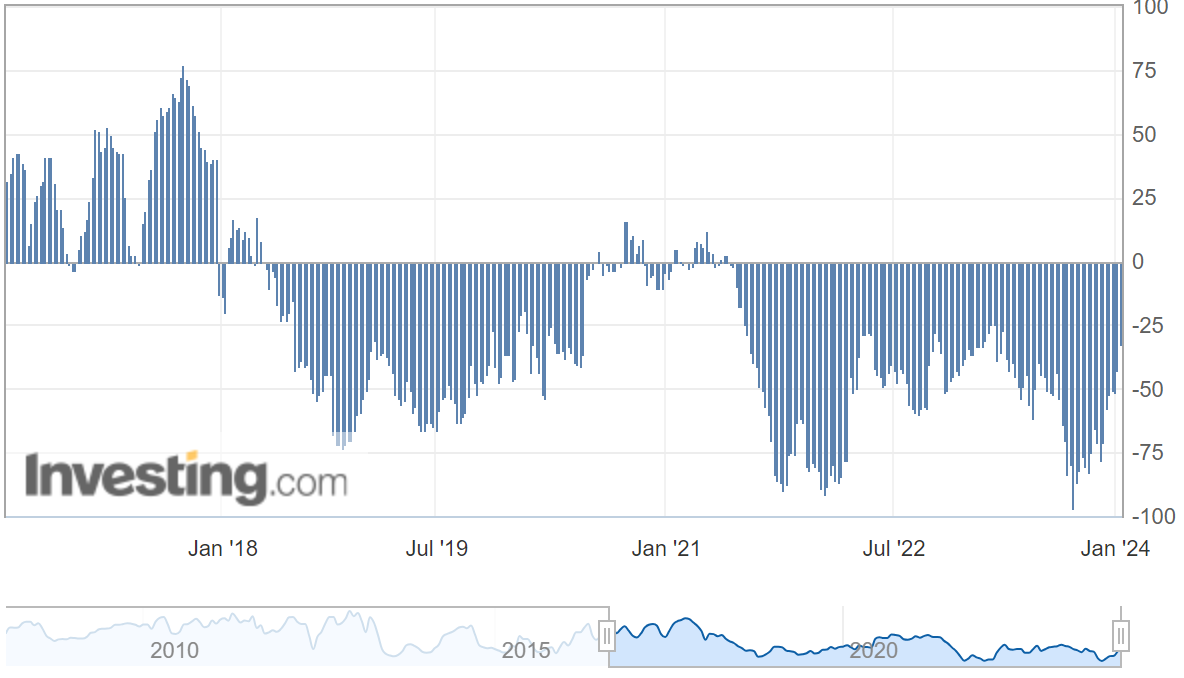

Dirt is hosing the reflation as Chinese data dumps:

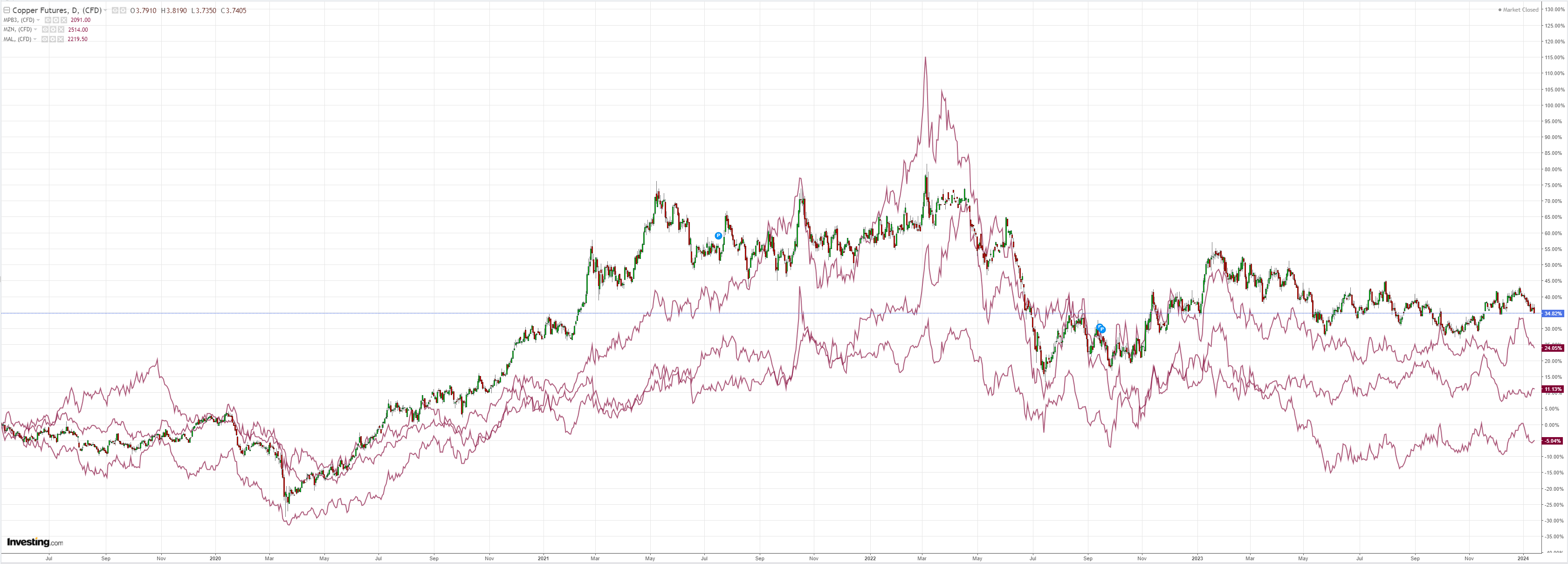

Big miners too:

EM yawn:

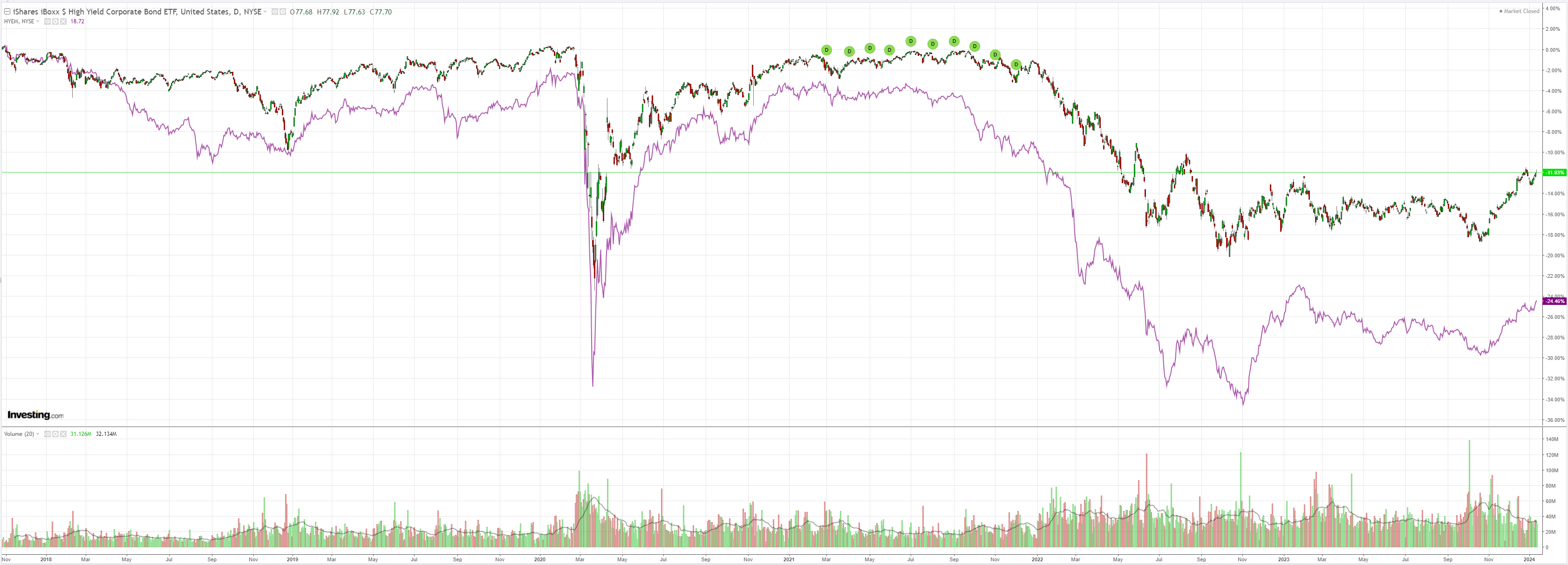

Junk hope:

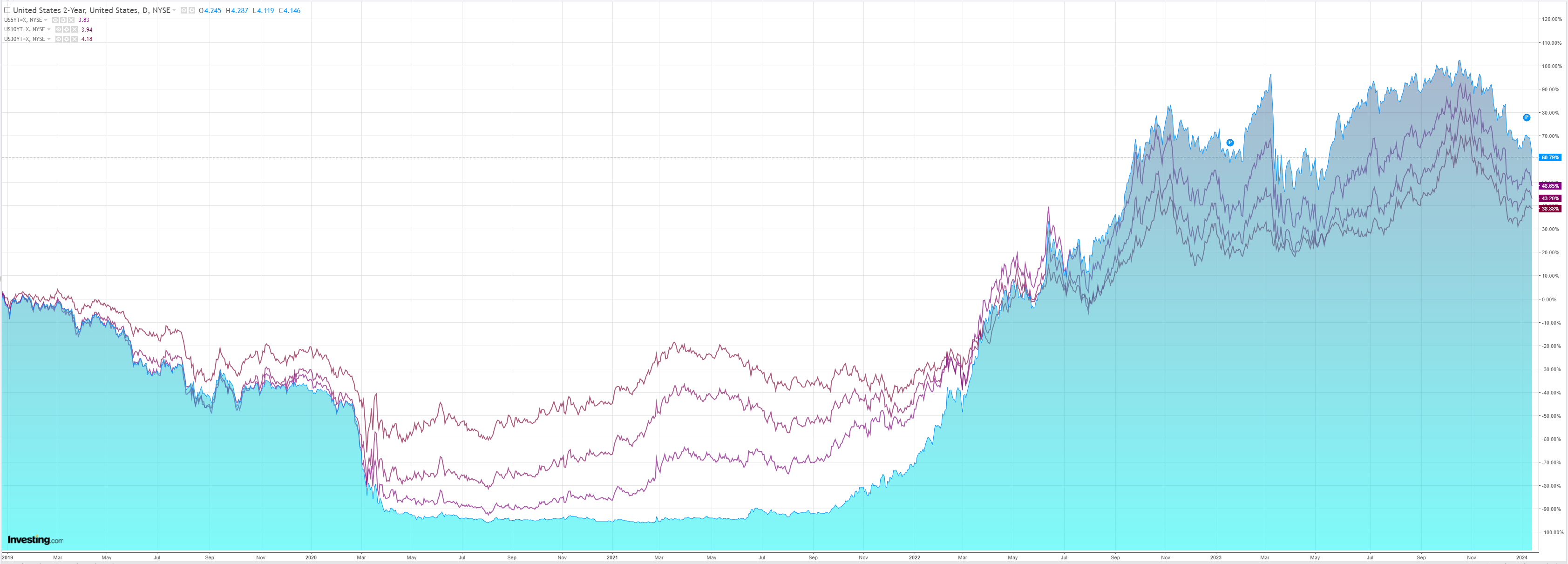

Yields down on the US PPI:

Stocks look exhausted:

BofA reckons AUD will keep going up:

We recently closed our long AUD (vs. GBP) recommendation on tactical considerations but remain constructive over 2024.

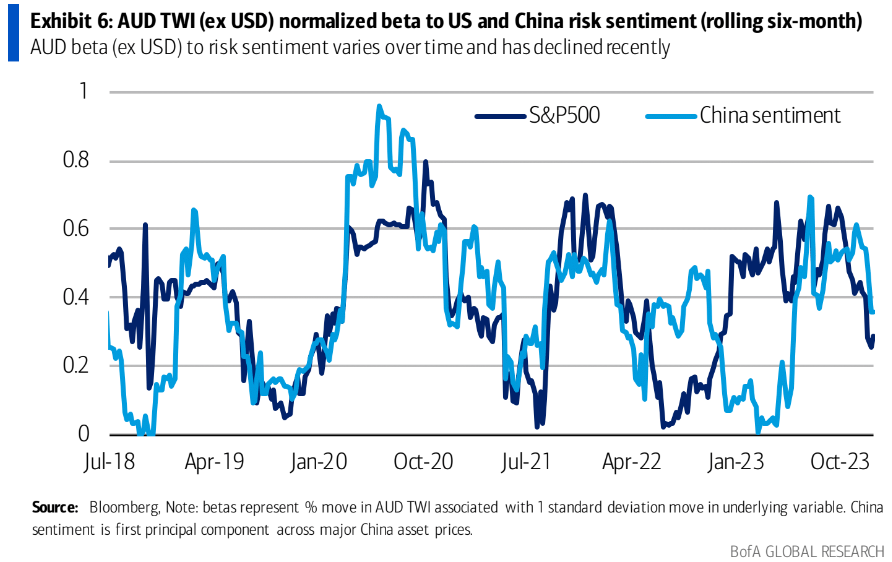

Our medium-term view partly rests on lower sensitivity to global risk sentiment over time.

This is already evident in the resilience of AUD TWI (ex USD) to the multi-year China slowdown, as well as the sharp compression of implied skew.

We argue these are durable trends related to export diversification and improvement in net foreign liabilities.

We are constructive AUD over 2024:

1.Domestic economic headwinds mean the RBA is likely done hiking. But we expect the RBA to be among the few central banks that do not cut in 2024, partly because the policy rate is less restrictive than elsewhere.

2.China sentiment remains at bearish extremes. China’s import impulse for Australia lags its policy stimulus by three quarters but several high frequency indicators can help track spill overs to AUD (new home sales, steel production, port shipments).

3.Service sector exports have recovered sharply but not yet back to trend levels nor share of exports observed pre-pandemic–the recovery could further support AUD.

4.Australia remains in a strong fiscal position relative to its G10 peers, both in terms of deficit and debt levels. This allows some room for fiscal support in the event of a growth downturn, reducing the burden on monetary easing.

5.While AUD is perceived as a “high beta” currency, an improving NIIP should reduce its sensitivity to risk over time.

My thoughts:

- RBA will be cutting this year. Conditions for households are tighter than elsewhere which is why sentiment is so bad.

- China sentiment might be bearish, but it is not extreme; it is the new normal post-property bust. Australian trade with China has not adjusted down to this reality.

- Yeh, more migrants.

- Any downturn is much more likely to result in rate cuts than fiscal.

- AUD is still high beta.

I agree that AUD will probably rise over the year with a global softish landing, but my enthusiasm for it is waning as the Japan/China deflation monster growls ever louder and the bears are chased out of the currency.