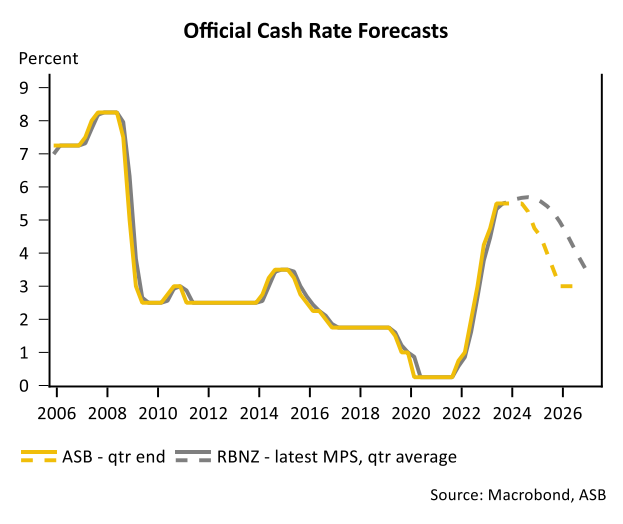

Reserve Bank to bring forward rate cuts

Big Four bank, ASB, says the New Zealand economy has lost momentum much faster than envisaged.

It believes that inflation will soon follow suit, which will prompt the Reserve Bank to cut the official cash rate in August 2024, six months earlier than its previous forecast:

“The weaker than expected GDP, historical revisions, and the new suite of monthly pricing data Statistics NZ is now publishing all point to inflation pressures easing quicker than we had been expecting”.

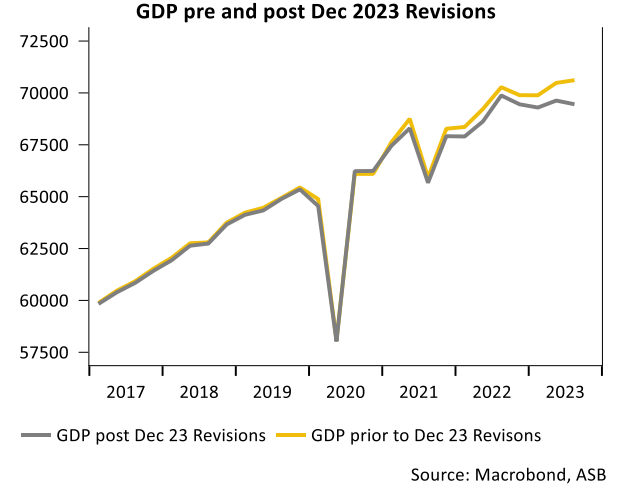

“Economic momentum has been a lot slower than previously thought, particularly for 2023. Q3 GDP fell 0.3%, against the +0.2% we expected (RBNZ +0.3%). The initially-published 0.9% growth for Q2 GDP got revised down to 0.5%, and there were further more minor downward revisions going back to 2021”.

“We have revised down our GDP outlook, on the basis that momentum will remain weaker than previously thought”.

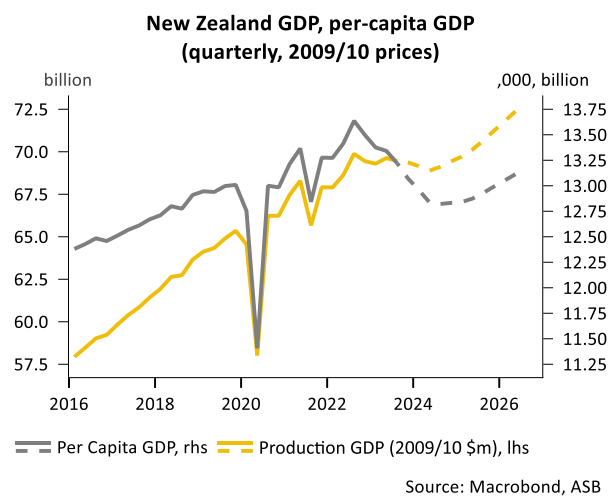

“Even with record net inbound migration, GDP has still fallen over the last year. Looking at per-capita GDP, the pressure of tight monetary conditions is evident, with per-capita GDP already down 3% over the past year and likely to eventually exceed the 4% decline NZ experienced during the Global Financial Crisis”.

“There is still a further lagged impact from debt servicing costs to still come through”.

“The labour market will soften at a faster pace, slowing wage growth more quickly and reducing cost pressures”.

“The general message from monthly pricing indicators suggests that inflation is undershooting the RBNZ’s expectations in the short term”.

“In short, we think the RBNZ is already putting enough squeeze on that it a) won’t need to lift the OCR further, and b) will find itself cutting the OCR much sooner than it has been expecting”.

I has a similar view on the Australian economy and believe our Reserve Bank will commence an easing cycle in the second half of 2024.

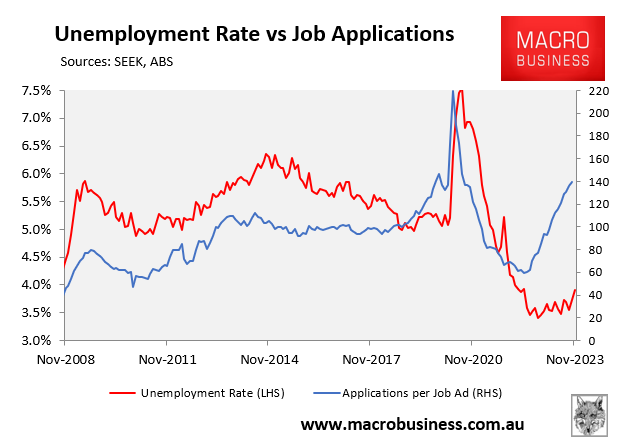

First, Australian unemployment will rise significantly next year and will likely approach 5% by year’s end.

Second, real per capita household disposable income has fallen sharply and is currently tracking around 2010 levels:

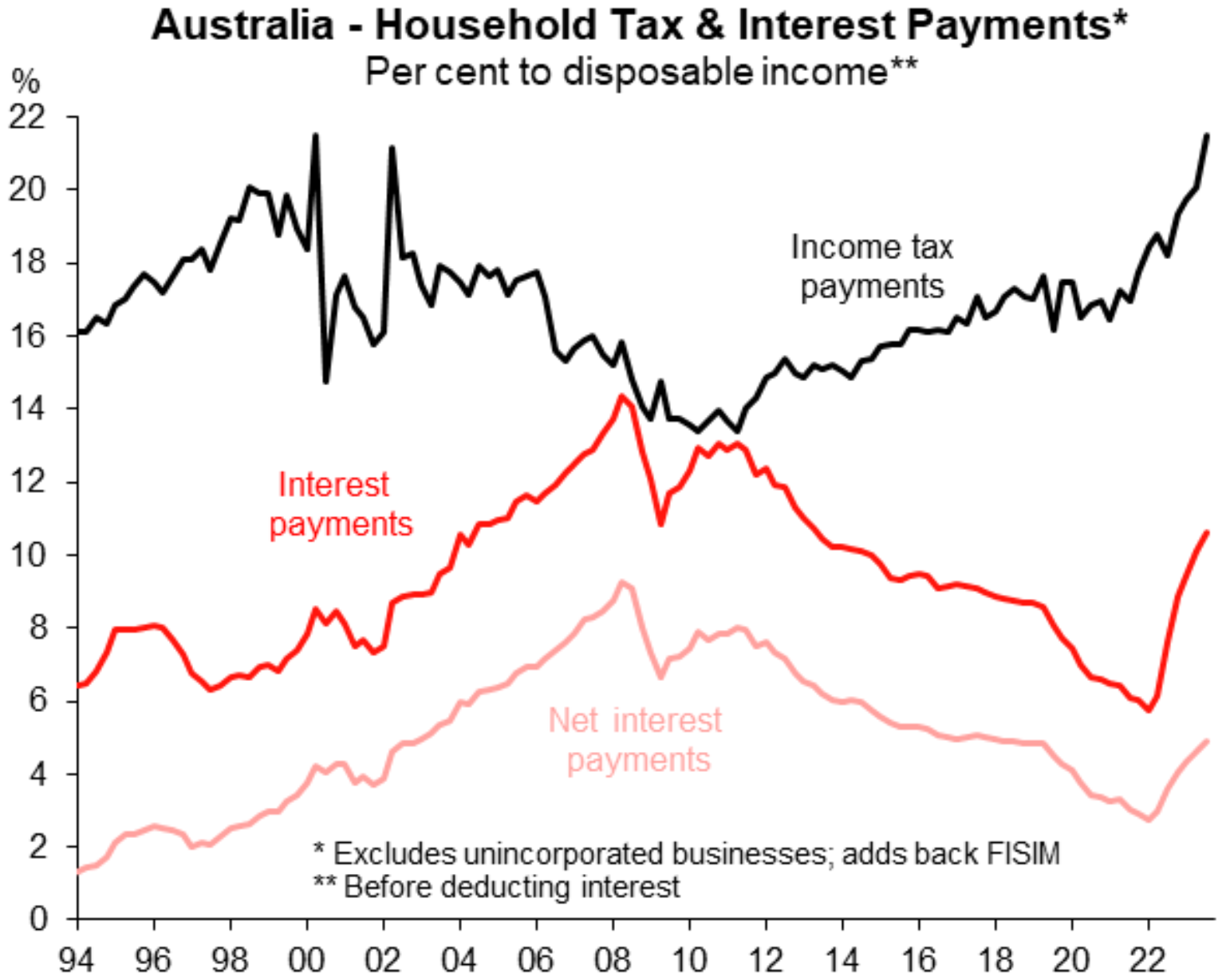

This partly reflects soaring mortgage and tax burdens:

Source: Justin Fabo

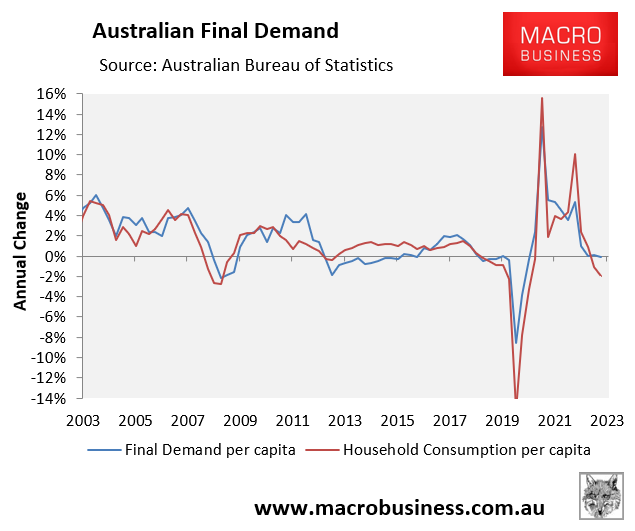

Real per capita household consumption fell by 1.9% over the year to September, but has obviously held up much better than incomes:

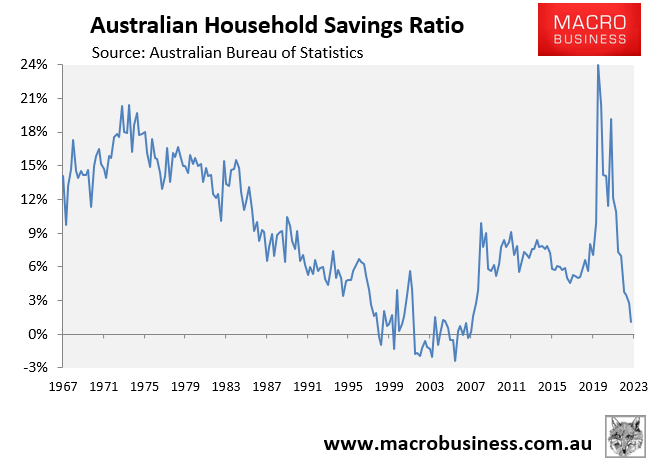

The reason why household spending has held up is because Australia’s household savings rate collapsed to only 1.1%, which was the lowest level since December 2007, before the Global Financial Crisis:

With the savings rate close to zero, this suggests that household consumption could fall in the period ahead unless incomes unexpectedly rebound.

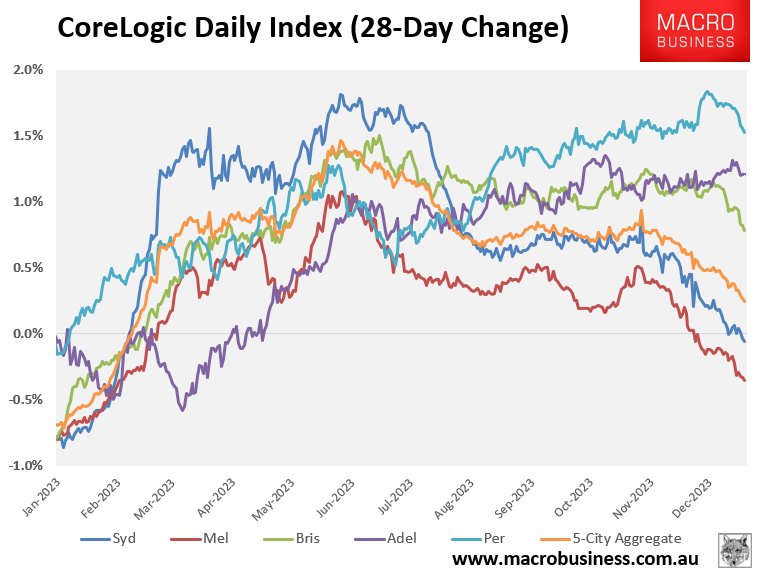

Third, the heat has well and truly come out of Australia’s housing market, with Sydney and Melbourne reporting outright falls and price growth more broadly softening:

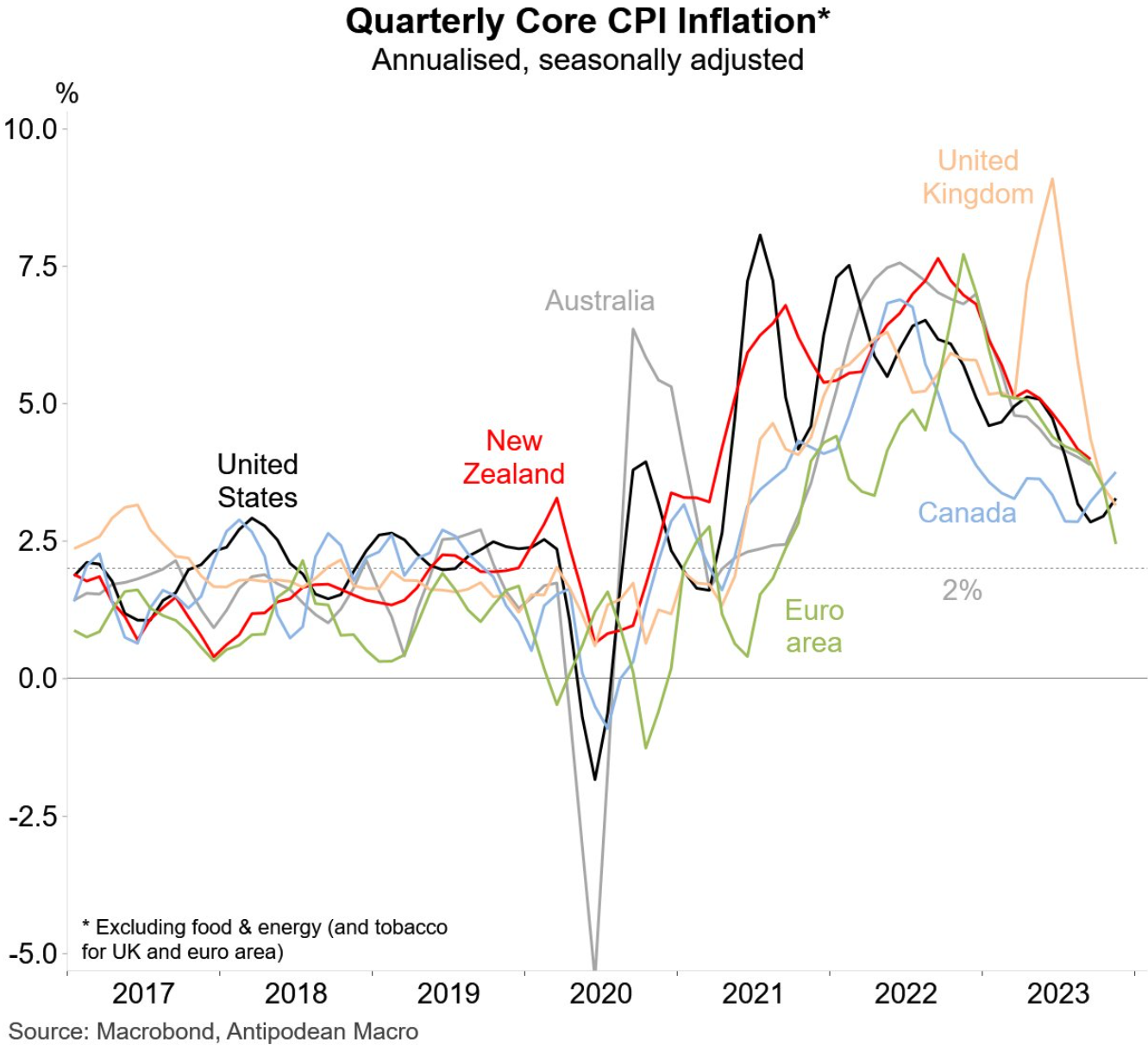

Finally, goods deflation is happening globally, helping to drag down core inflation (including in Australia):

Given these conditions it will be a high hurdle for the Reserve Bank of Australia to hike again.

Instead, they are more likely to cut as inflationary pressures ease, the economy weakens, and unemployment rises.