Reserve Bank relief as inflation falls faster than expected

Statistics New Zealand on Wednesday released its new monthly inflation gauge, which captures around 45% of the CPI basket.

The gauge includes a number of volatile items that can cause sharp quarter-to-quarter swings in the CPI.

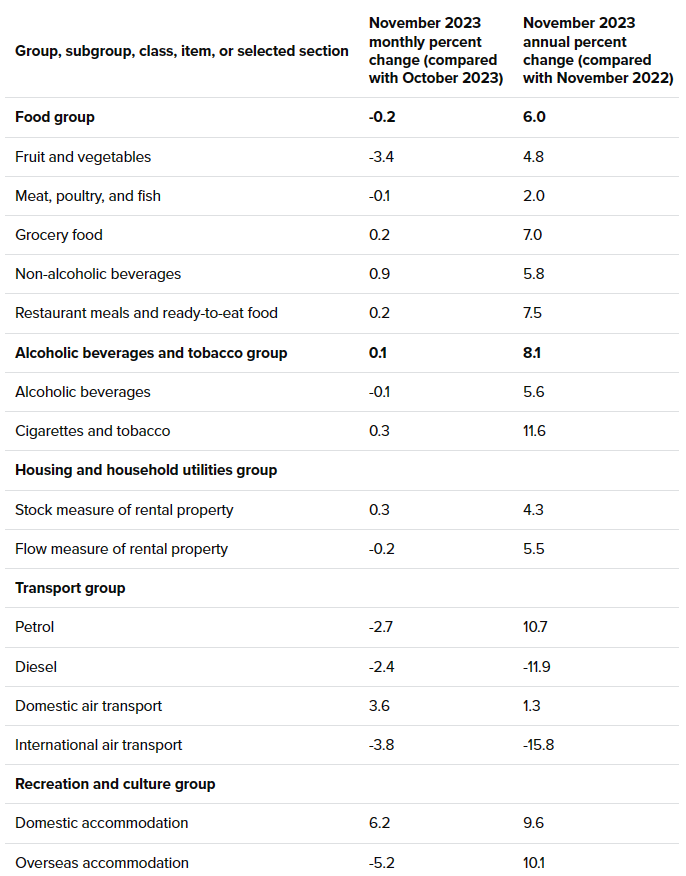

The November update highlighted softness in the prices for air travel, which offset a smaller-than-expected decline in food prices:

Source: Statistics New Zealand

Westpac believes “today’s data reinforces the downside risks to the RBNZ’s forecast for a 0.8% rise in consumer prices in the December quarter”.

Accordingly, Westpac has “revised our forecast for December quarter inflation to 0.3% (down from 0.6% previously). That would leave prices up 4.5% for the year”.

“The RBNZ will take some comfort from the easing in headline inflation”, Westpac says.

“However, while we’ve seen volatility in some specific prices, some of this is just reversing the large price rises that we saw during the pandemic as a result of supply chain disruptions”.

“That won’t be an enduring source of deflationary pressures for the RBNZ”, Westpac warns.

“Core inflation – especially for domestic prices – remains elevated. That means inflation is still set to remain far above the RBNZ’s target well into the new year”.

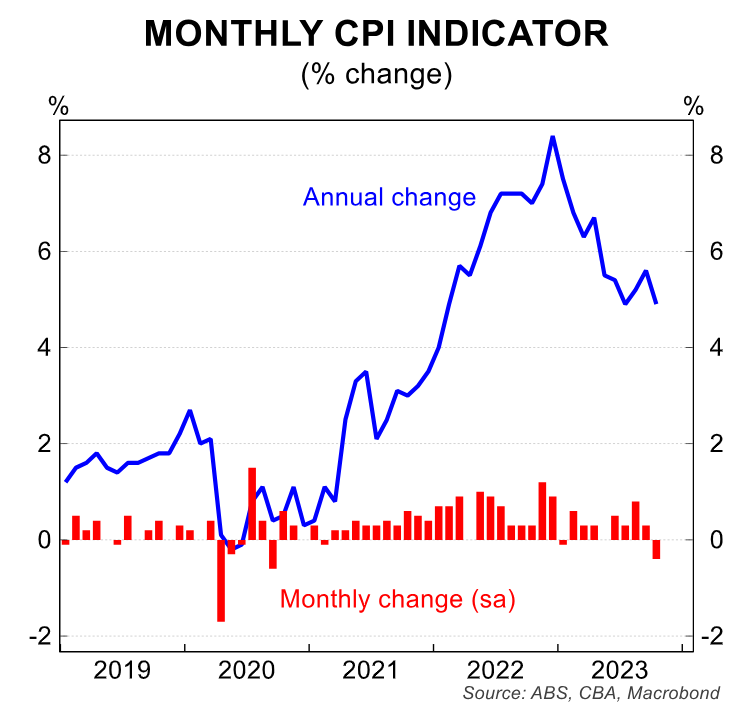

Similar conditions were in play with Australia’s October monthly CPI indicator from the Australian Bureau of Statistics (ABS), which came in below market expectations at 4.9%/yr (versus the consensus of 5.2%/yr):

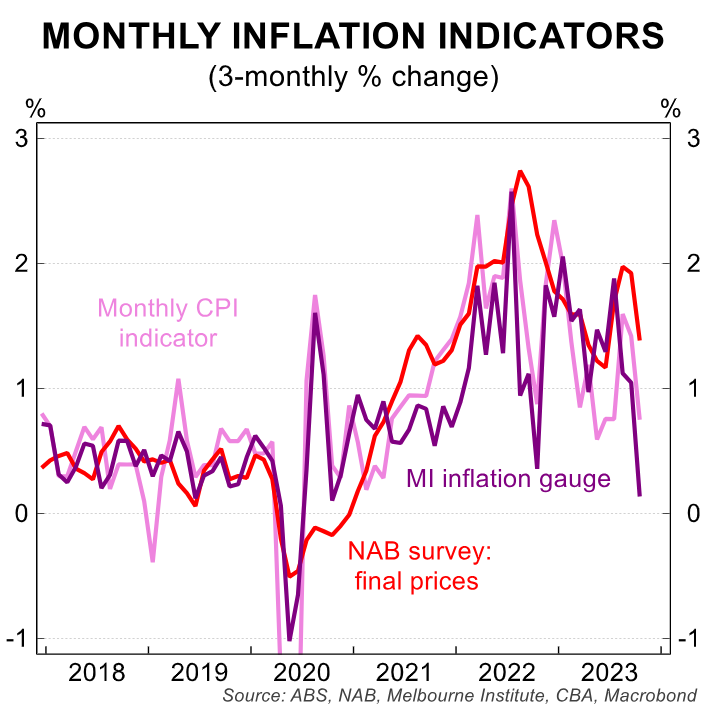

Other surveys also suggest that trimmed mean CPI in Q4 23 is unlikely to be stronger than the RBA’s ~1.0%/qtr forecast, according to CBA:

But like New Zealand, the October monthly CPI indicator from the ABS did not capture a lot of services price movements in the economy.

For those movements, we will have to wait for the release of the Q4 quarterly inflation prints in January.

Nevertheless, the changes in the basket of prices surveyed by both Statistics New Zealand and the ABS are encouraging and point to receding inflationary pressures in both countries.