By Gareth Aird, head of Australian economics at CBA.

Key Points:

- We expect the RBA to leave the cash rate on hold at 4.35% at the December Board meeting.

- We ascribe a 90% chance to no change and a 10% probability to a 25bp increase (we consider the risk of any other move to be immaterial).

- The RBA Board is now data dependent and the economic data released since the November Board meeting does not support another rate increase in December.

- We expect the RBA to retain their tightening bias and expect no changes to current forward guidance.

- A no change decision is anticipated to be accompanied by the line, “whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks.”

- The Q323 national accounts will be published on Wednesday 6 December (the day after the RBA Board meeting).

The December Board meeting should be a low key affair:

The upcoming RBA Board meeting should not be a pivotal one for Australian financial market participants.

We see very little chance of the RBA raising the cash rate or shifting their forward guidance (recall that the RBA raised the cash rate by 25bp to 4.35% at the November Board meeting after four months of policy on hold).

The RBA Board is data dependent. And any further tightening will require the economic data, particularly on the prices side of the economy, to print stronger than the RBA is anticipating.

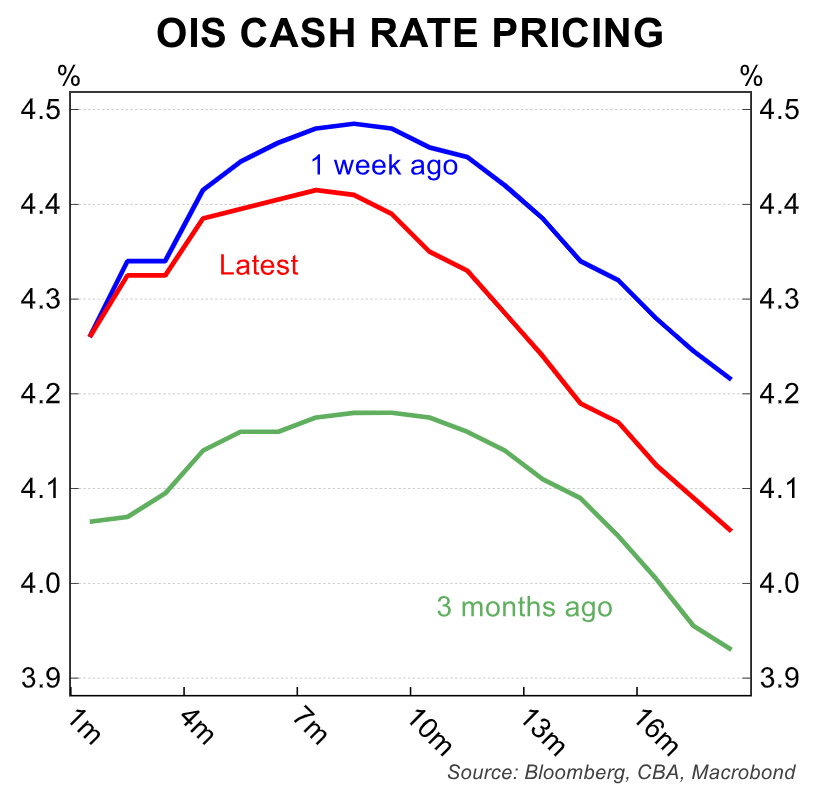

Markets have ascribed a 3% chance that the RBA lifts the cash rate in December. That looks a pretty fair assessment of the balance of probabilities next week.

Key domestic economic data that has printed since the November Board meeting does not support the case for further policy tightening in December.

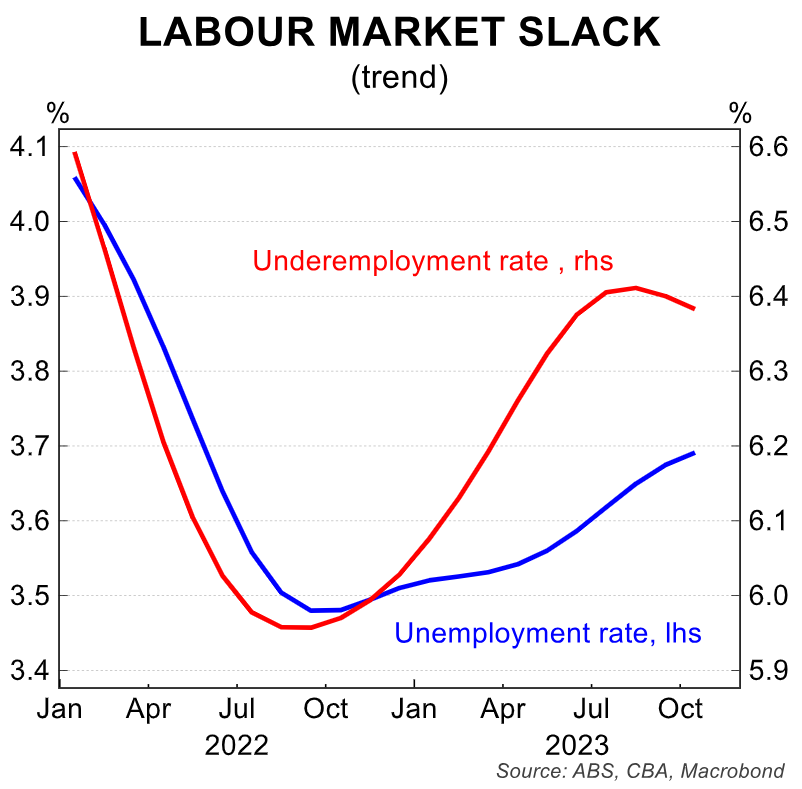

The October labour force survey reported a small uptick in the unemployment rate from 3.6% to 3.7%.

The 1.3%/qtr increase in the Q3 23 WPI was broadly in line with the RBA’s forecast from the November Statement on Monetary Policy (SMP).

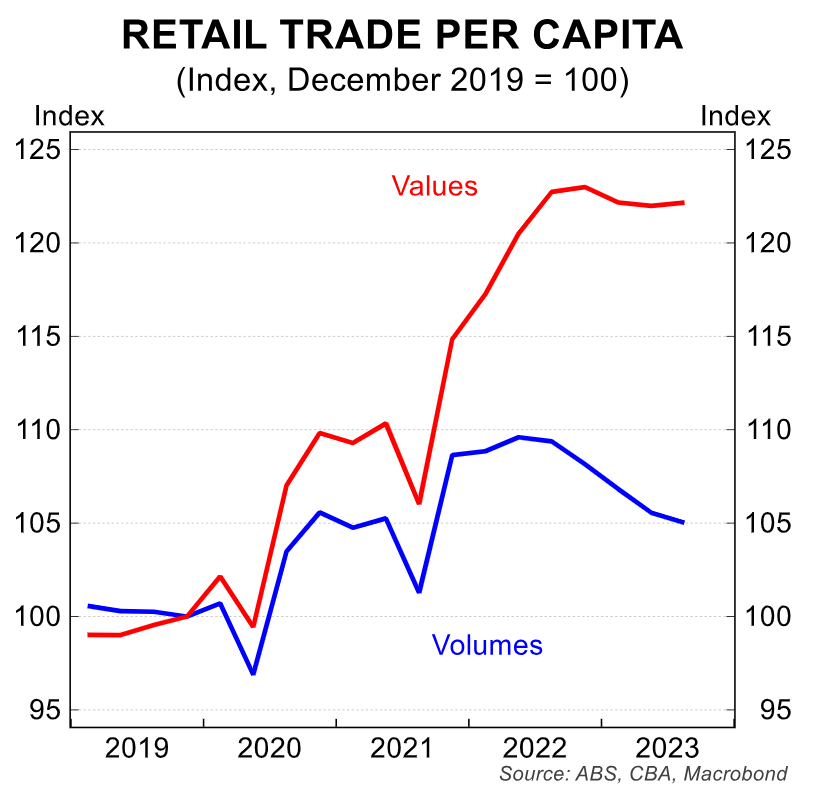

October retail trade was down by 0.2%/mth.

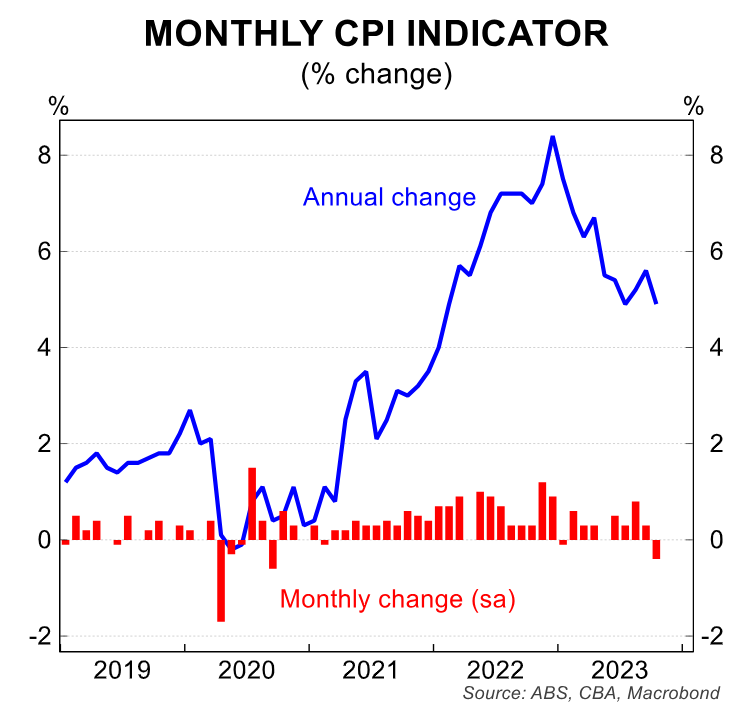

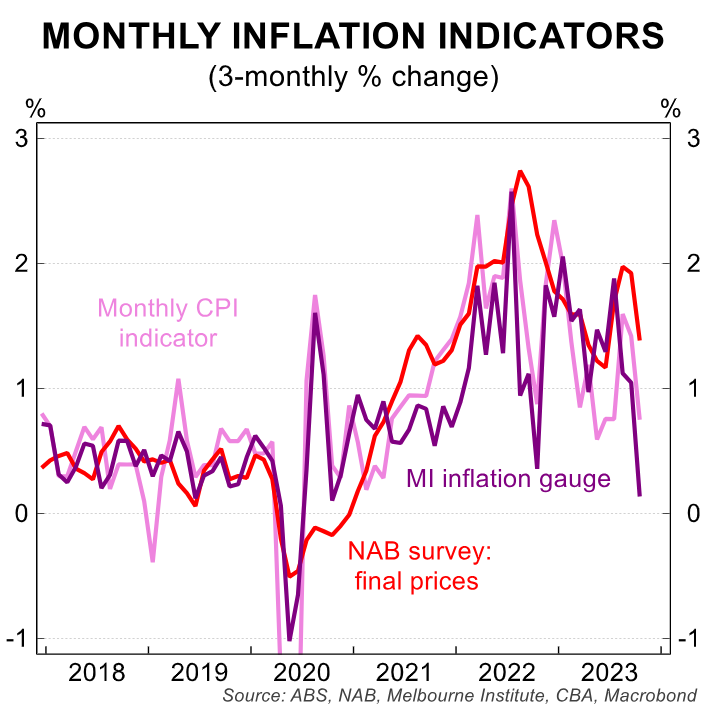

The October monthly CPI indicator came in below market expectations at 4.9%/yr (versus the consensus of 5.2%/yr).

More importantly the data suggests that trimmed mean CPI in Q4 23 is unlikely to be stronger than the RBA’s ~1.0%/qtr forecast.

To be fair, the October monthly CPI does not capture a lot of services prices movements in the economy. That information will be apparent in the November monthly CPI.

That said, the changes in the basket of prices surveyed over October is encouraging. A ‘nowcast’ of the December quarter CPI based on the already released prices data for Q4 23 suggests we are on track to see a trimmed mean outcome in line with the RBA’s forecasts or below –so far so good.

Prior to the October monthly CPI we wrote that the already released private survey prices gauges for October implied inflation pressures had eased compared to Q3 23. The official data released this week is consistent with these private surveys.

In that context, the expected decision to leave the cash rate on hold in December should be straight forward.

An ‘on hold’ decision will mean that the focus for market participants is on the Governor’s Statement accompanying the decision rather than the decision itself.

The Governor has arguably upped the ‘hawkish’ rhetoric since the November rate increase. But we believe much of the Governor’s communication post the November rate hike has simply justified the increase in the cash rate rather than any shift in the RBA’s reaction function.

We also think that the Governor is trying to ‘jawbone’ to the household sector to elicit a greater behavioural response to the November rate increase.

The RBA Board does not want to tighten policy further. But they will do so if the data makes that case that another rate increase is the right policy option.

For that to happen, there must be a clear signal in the domestic economic data that the policy rate is not sufficiently restrictive to bring inflation back to target over the period of time that the RBA Board deems acceptable.

The data that has printed since the November rate hike does not support another rate increase in December. As such, we expect a decision to leave the cash rate unchanged next week to be straight forward.

The RBA will retain a tightening bias, however. And it would be odd if the Governor shifted the key paragraph pertaining to forward guidance.

In conclusion, we expect a no change decision in December to also accompanied by no change to the Board’s forward guidance.

Namely we expect the line to be repeated that, “whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks.”

If our expectations for the RBA next week are correct then the more interesting event should be on Wednesday when the ABS will publish the Q3 23 national accounts.

The national accounts will give us an update on production, income, savings, unit labour costs and productivity in the September quarter.

At this stage we forecast an increase in real GDP of 0.4%/qtr. But a host of partial data is due to print early next week and we will finalise our point estimate for Q3 23 GDP on Tuesday.