The December quarter ACCI–Westpac Business Survey has been released with manufacturers continuing to experience the weakest demand conditions in a decade (outside of the pandemic shock in 2020), along with higher costs.

The mood of manufacturers has also darkened, with a net 41% expecting the general business situation to worsen over the next six months – the weakest reading since the Global Financial Crisis (GFC) in 2008.

Below is the summary of Westpac’s note.

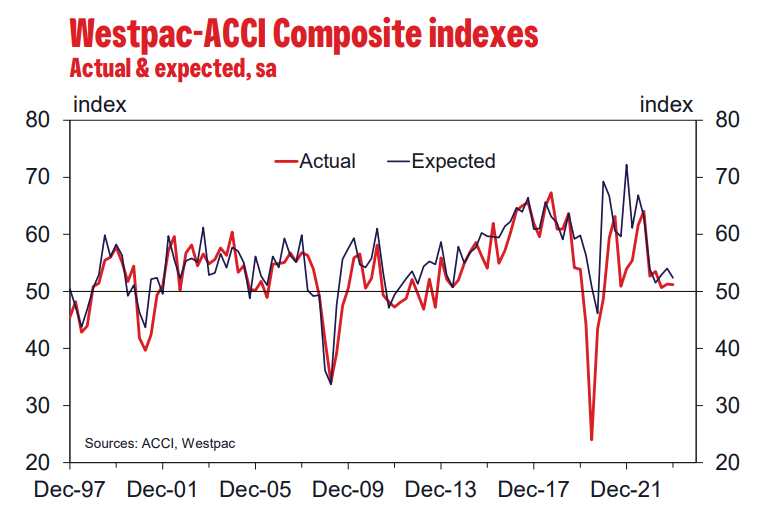

The Westpac-ACCI Actual Composite remains at its lowest level since 2014, excluding the pandemic shock, moving sideways into year-end at 51.2 in December from 51.3 in September.

With a reading around the break-even mark of 50, for a third consecutive quarter, this indicates that conditions are near stalling.

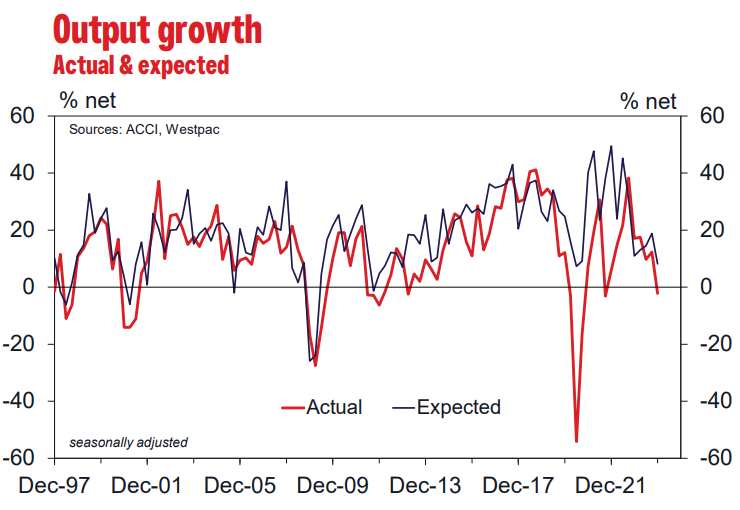

The December quarter survey reported tepid growth in new orders, a decline in output, and broadly flat employment and overtime.

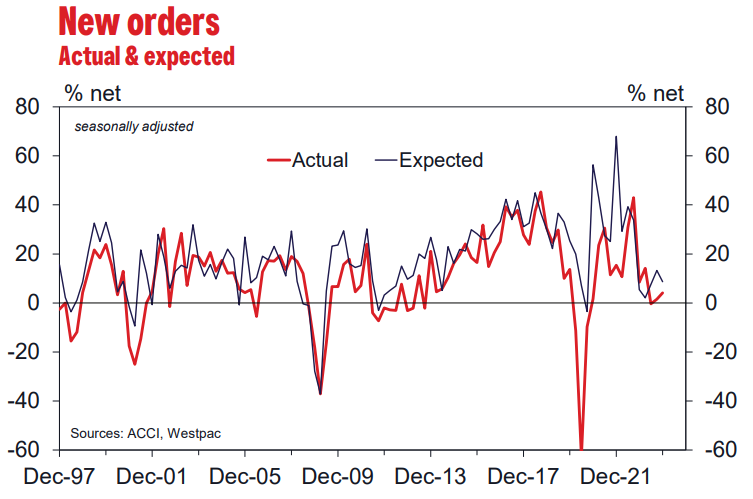

As reported three months ago and confirmed in this update, the key message and the number one concern of manufacturers is weak new orders. New orders have been near flat for three consecutive quarters, at an average net +2%, together the weakest outcomes since 2013, excluding the pandemic slump in 2020.

The stalling of manufacturing new orders mirrors the flat-lining of household demand across the Australian economy which is driving the slowdown. Real household disposable income contracted a sharp 4.3% over the year, squeezed by high inflation, higher interest rates and additional tax obligations.

The outlook heading into 2024 is downbeat. The Expected Composite printed a soft 52.4, in line with the average for 2023, but down from 54.0 in September. With the impact of interest rate rises still materialising, the soft trend is likely to continue.

The mood of manufacturers has darkened. A net 41% expect the general business situation to worsen over the next six months, down from a net 35% last quarter and the weakest reading since the GFC.

Equipment investment intentions have been marked down from those in 2022. A net 10% of respondents intend to increase spending in the next 12 months, down from a net 19% over the second half of 2022, but a little above the long-run average of a net 6%, with capacity utilisation levels still elevated.

Cost pressures re-emerged, after moderating in the September quarter. The combination of falling output in the December quarter and still rising costs triggered a sharp jump in average unit costs. A net 66% of firms reported a rise, in line with the June reading of 67%, after dipping to 37% in September.

Manufacturers are facing cost pressures, both non-labour (a rebound in commodity prices) and labour.

Official data reports that manufacturing annual wages growth is running at a brisk 4.4%, a 15 year high and only a touch below the 2008 peak of 4.6%.

Wage pressures look set to extend into 2024 the survey reports, a net 42% of respondents expect their next enterprise wage agreement to deliver an outcome above their last.

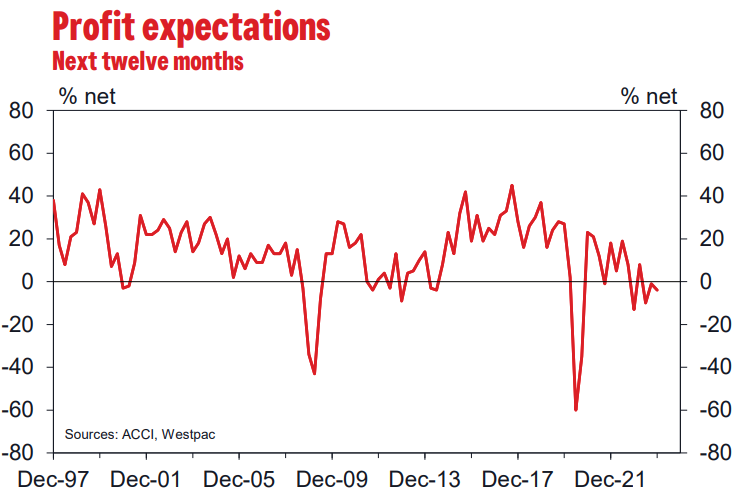

Profit expectations slipped further into negative territory in the December quarter, with a net 4% of manufacturers anticipating profits will decline in the coming year, well below the long-run average for the survey of a net 19% expecting an increase.