Asian share markets are still somewhat mixed but this is mainly due to USD weakness lifting Yen which has dragged Japanese shares down while the rest of the region continues to rebound from Friday night’s US employment print. Tonight’s inflation follow up print could upset the apple cart in both currency and bond markets however.

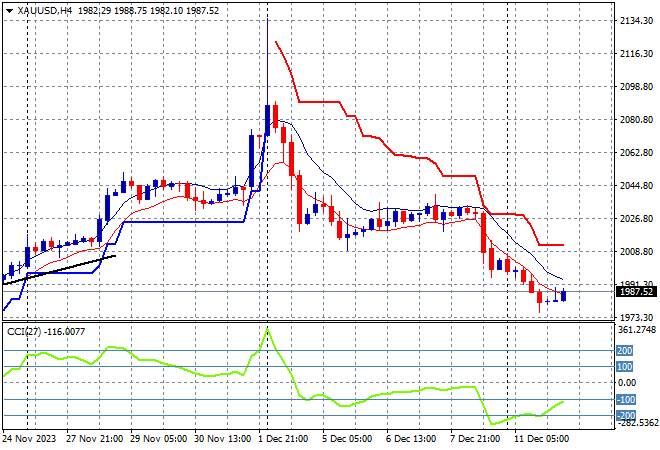

Oil prices are trying to rebound after some steep falls last week with Brent crude staying above the $76USD per barrel level while gold has failed to get back above the $2000USD per ounce level following the subdued recovery last week but without further downside:

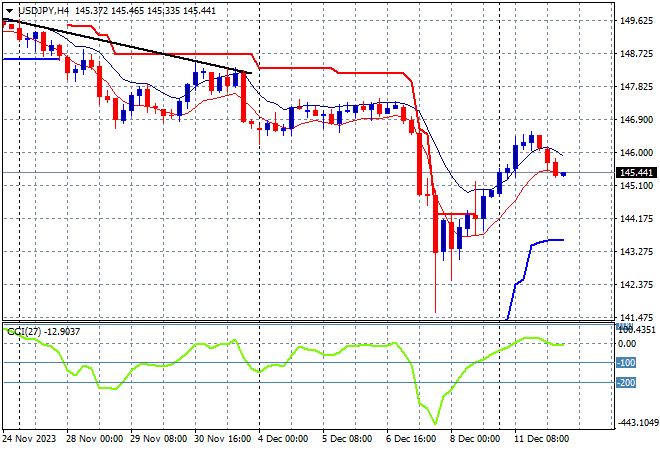

Mainland Chinese share markets started off slow but the Shanghai Composite finally broke the 3000 point barrier to close 0.4% higher while in Hong Kong the Hang Seng Index has gained at least 1% to 16375 points. Japanese stock markets however have not been able to translate the previous gains into anything sustainable with the Nikkei 225 putting in a scratch session at 32843 points while the USDJPY pair has pulled back slightly to the mid 145 level, taking back all of the previous gain:

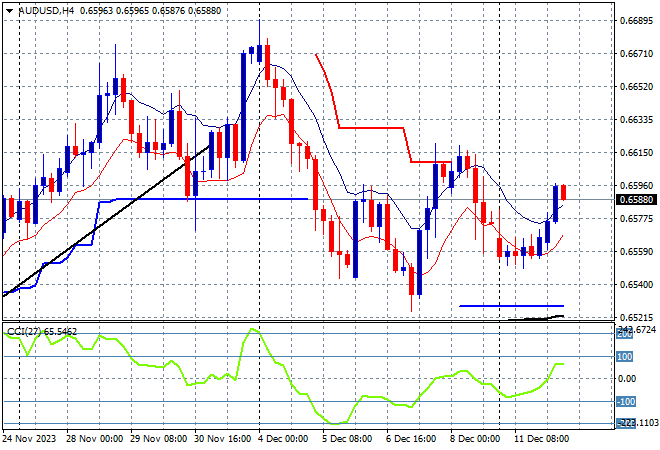

Australian stocks were able to put in a modest session with the ASX200 lifting further above the 7200 point level to close 0.5% higher at 7235 points while the Australian dollar is taking advantage of USD weakness with another attempt at getting back above the 66 cent level:

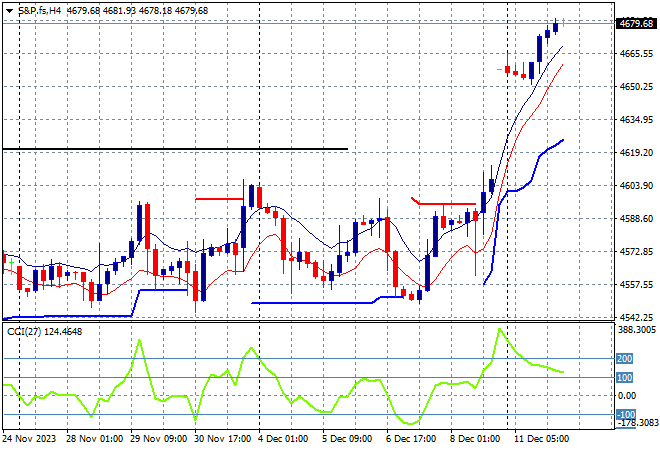

S&P and Eurostoxx futures have lifted higher going into the London open as the S&P500 four hourly chart shows support upgraded since Friday night’s NFP print and subsequent rally. The 4600 point level is likely to become the new support level having played as resistance for so long as part of a horizontal continuation pattern that is now broken:

The economic calendar swings into high gear with UK unemployment, the closely watched German ZEW survey then US core inflation numbers for November.