DXY was down Friday night:

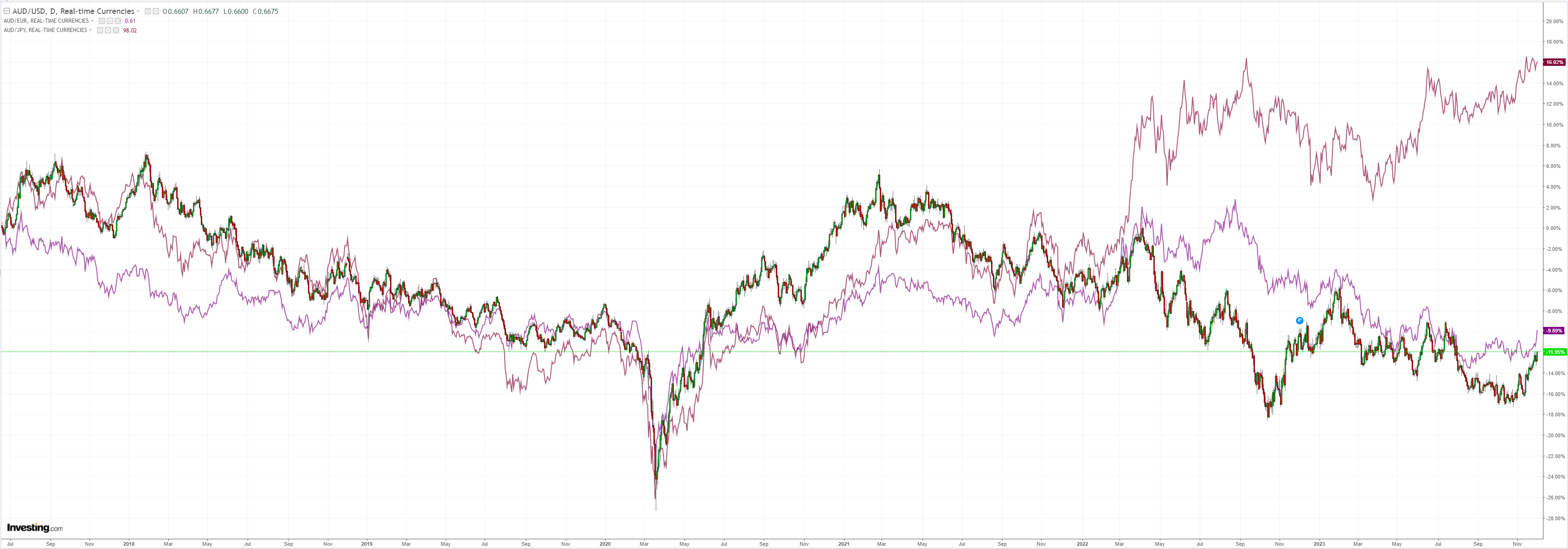

AUS is arcing towards 70 cents:

Gold is at an all-time high:

Copper is bid:

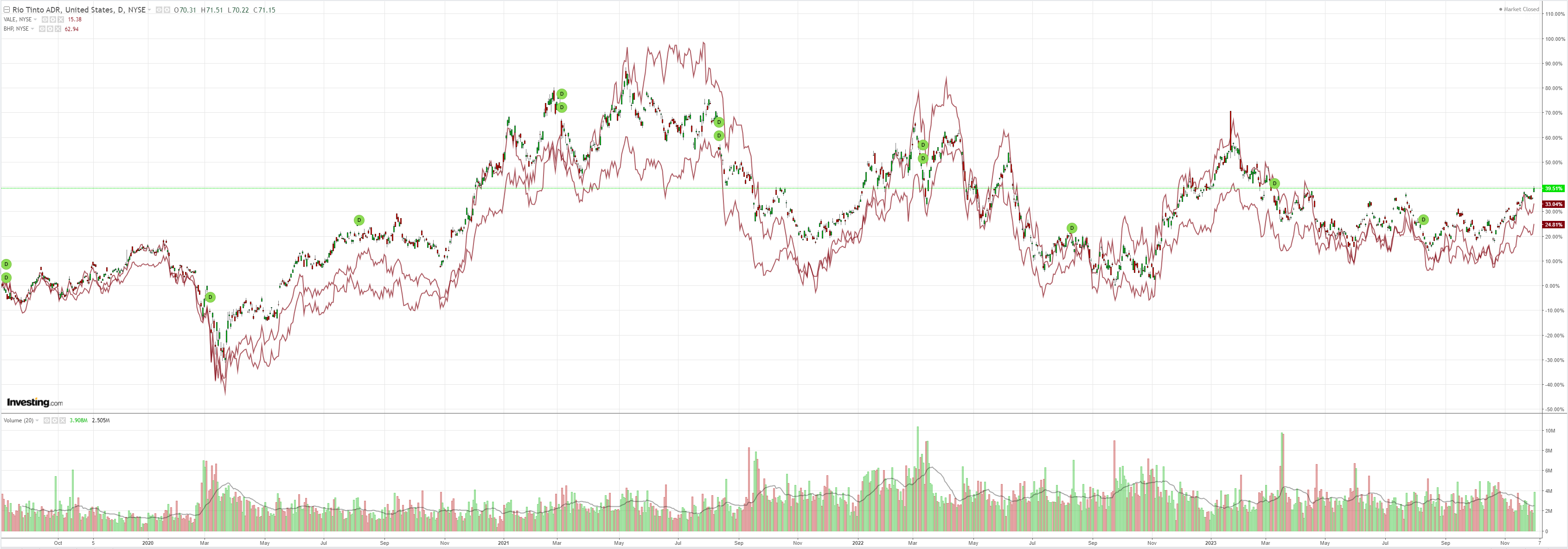

Miners gapped:

Very atypically, EM sat it out:

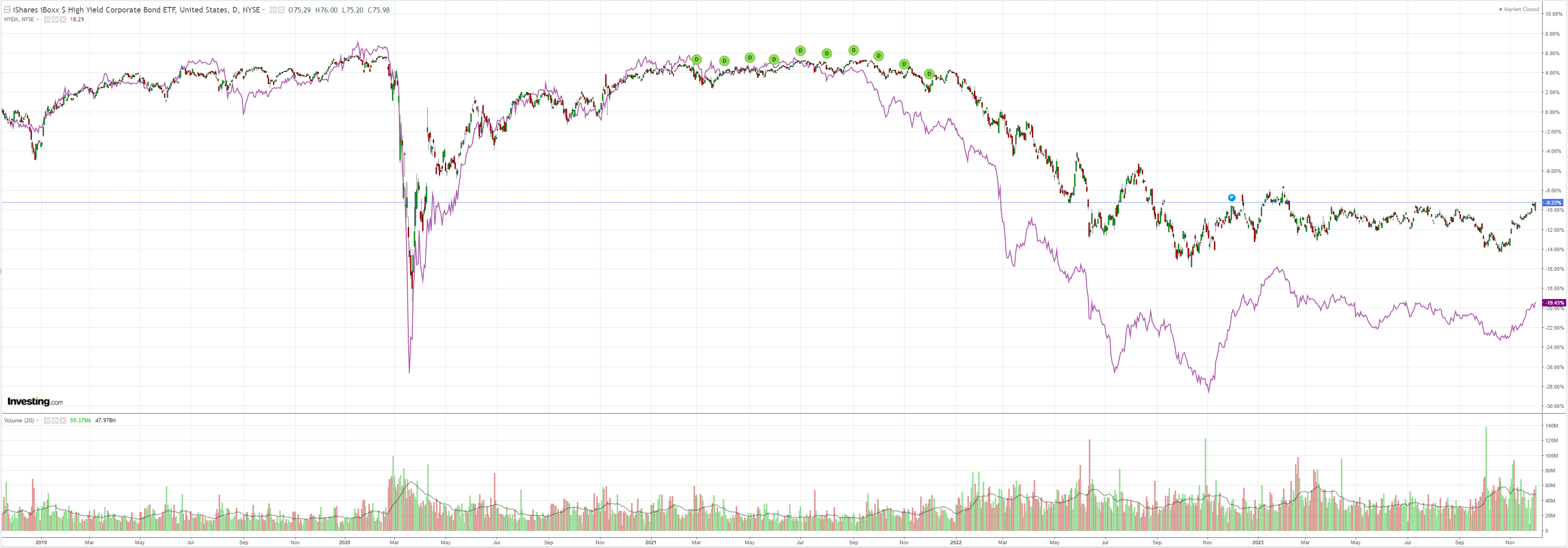

Though junk is pointing it all up:

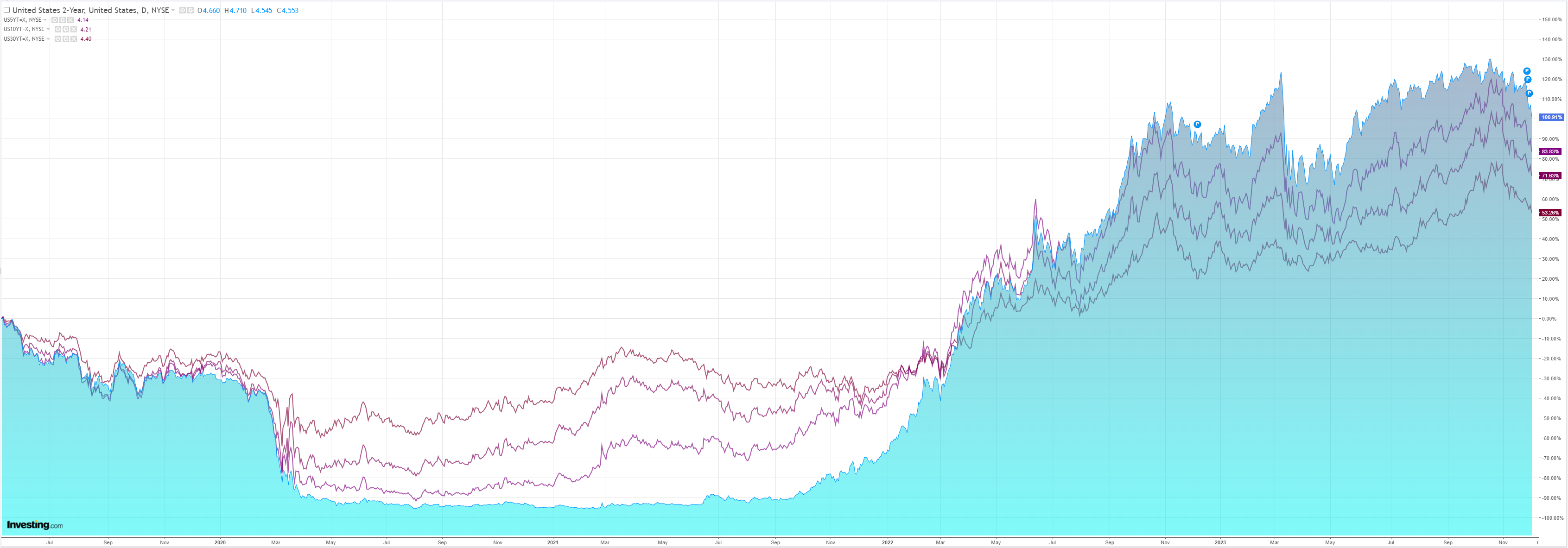

As the end of cycle bear steepening is here:

Even stocks managed a half-bid:

Classic reflation dynamics as the US ISM came in weak:

The Manufacturing PMI® registered 46.7 percent in November, unchanged from the 46.7 percent recorded in October. The overall economy continued in contraction for a second month after one month of weak expansion preceded by nine months of contraction and a 30-month period of expansion before that. (A Manufacturing PMI® above 48.7 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index remained in contraction territory at 48.3 percent, 2.8 percentage points higher than the figure of 45.5 percent recorded in October. The Production Index reading of 48.5 percent is a 1.9-percentage point decrease compared to October’s figure of 50.4 percent. The Prices Index registered 49.9 percent, up 4.8 percentage points compared to the reading of 45.1 percent in October. The Backlog of Orders Index registered 39.3 percent, 2.9 percentage points lower than the October reading of 42.2 percent. The Employment Index registered 45.8 percent, down 1 percentage point from the 46.8 percent reported in October.

And the market overran Fed Chairsatan Powell:

Jay Powell has sought to push back on speculation that the Federal Reserve had won its fight against inflation, even as traders boosted bets that the US central bank could start cutting interest rates as early as next March.

In a speech on Friday, the Fed chair indicated that it was too soon to rule out further rate rises or to start discussing cuts.

“It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease,” he said, just before the start of a quiet period preceding its final monetary policy meeting of the year.

The bear steepener is turning violent, driven by systematics that are too short bonds. That said, gold is corroborating a sudden pivot by the Fed in the near future.

That stocks can’t get bid is a measure of how little conviction the market has in its own priced soft landing.

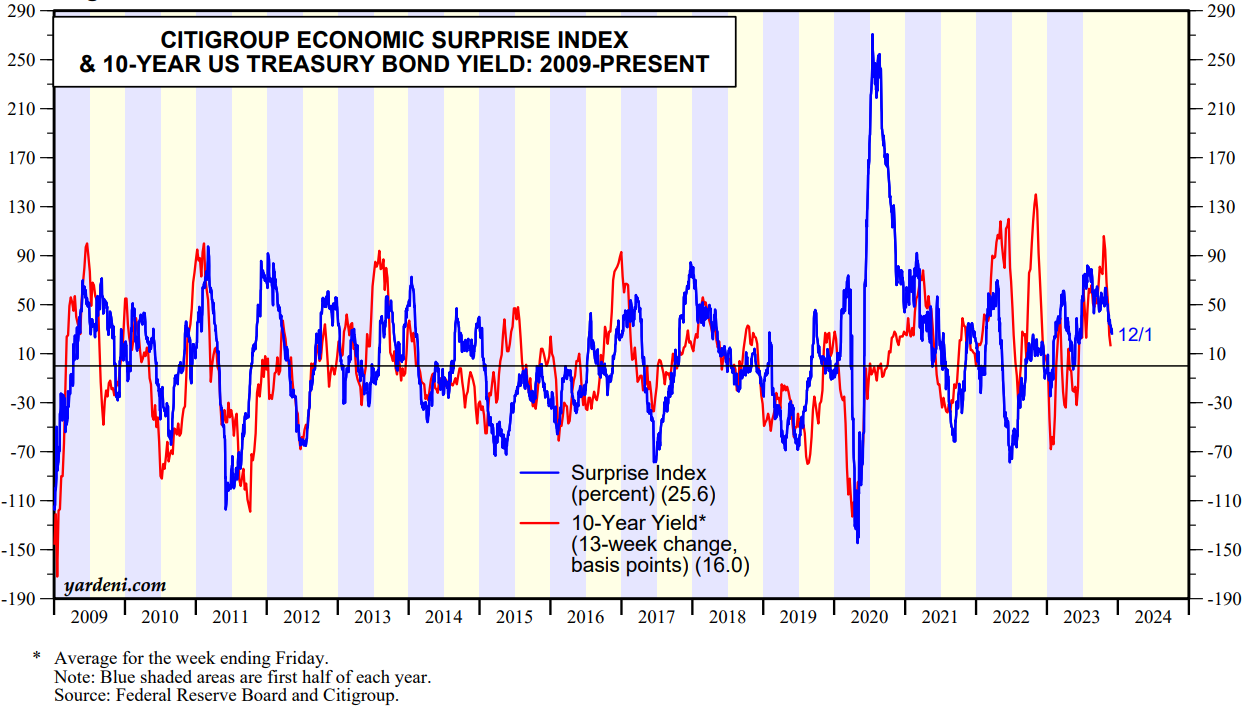

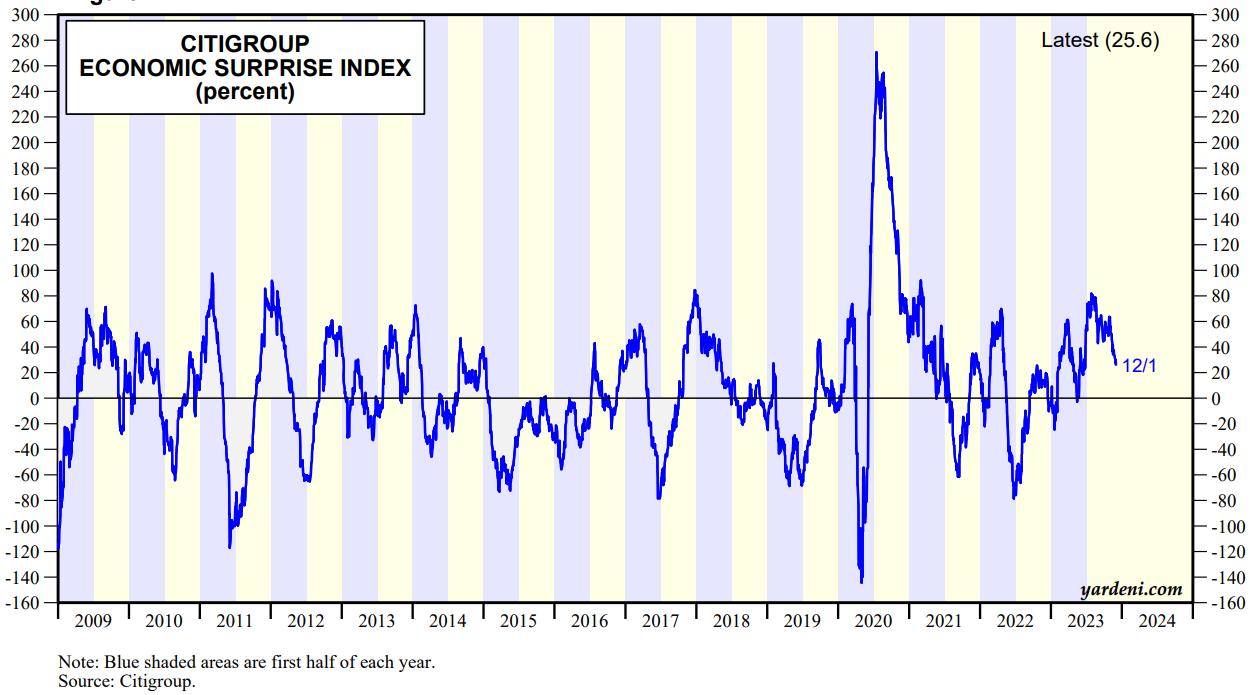

US data is surprising to the downside now:

It will take a fall into the negative to bring back a hard landing scare. That would put a rocket under the steepener, gold and the AUD: