BNP isn’t sparing the forex horses.

Fed reaction function shifts: Although a number of Fed speakers this week, including Governor Powell today, have tried to walk back dovish rhetoric from Governor Waller, we think the genie is out of the bottle, meaning:

1. the market is and could remain firmly convinced the next move is more likely to be a cut than a hike, and

2. the market may be more reactive to softer than stronger US activity and price data.

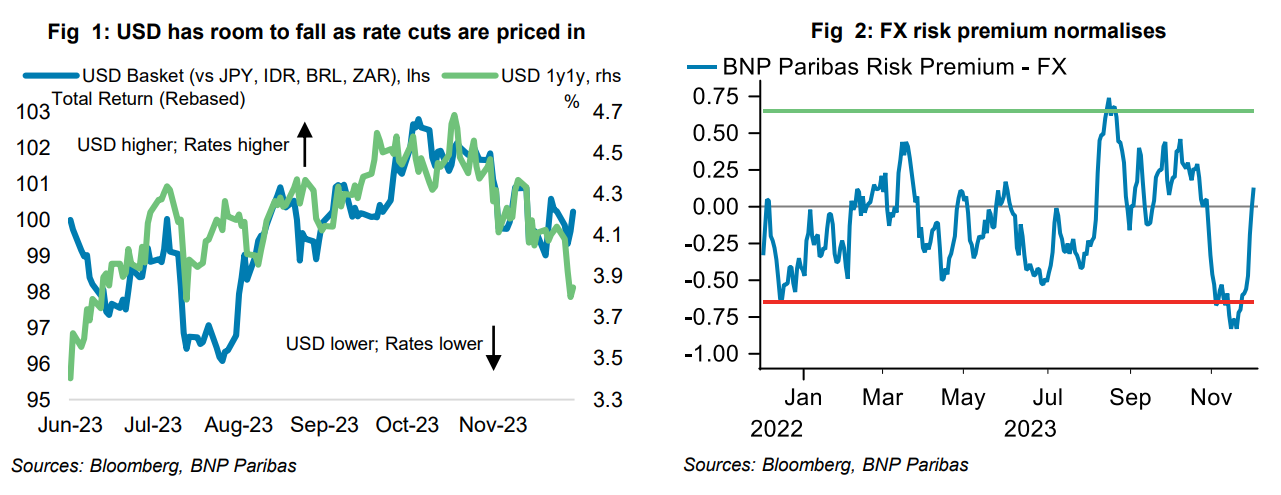

A perceived more proactive Fed, where the central bank is unlikely to wait for a big decline in the data before acting, means the left hand side smile risks have fallen, while the middle of USD smile risks have risen (see here). Combined with a still decent global growth we see the USD transitioning into a structural bear market. A 25bp March cut is currently priced with around a 60% implied probability. We do not think it necessary for US front-end yields to price in a higher Fed rate cut probability for the USD to weaken further, because the USD has weakened less than rates would have implied. Figure 1 shows our USD basket has scope to catch down with the rally in US 1y1y forward swap rates.

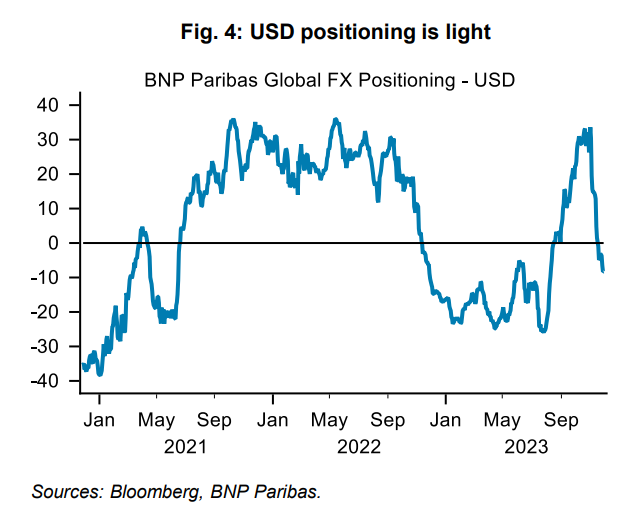

FX models no longer signal caution in selling USD. While our positioning, valuations and risk premium models are not telling us to short the USD, these tend to be less effective at capturing trend moves in markets and importantly, are no longer flagging caution in selling the USD. BNP Paribas FX risk premium has turned positive (Figure 2), having been low previously, which suggests improved risk-reward for USD shorts, and BNP Paribas Global FX Positioning Tracker signals market positioning is neutral on the USD (Figure 4), rather than bearish.

Expressing bearish USD view via a basket: To express our bearish USD view we choose currencies from different regions to more accurately capture a broad USD move and with varying betas to global equities in order to reduce sensitivity to risky assets. The currencies chosen (BRL, JPY, IDR and ZAR) also have among the most bullish year-ahead consensus forecasts and historically it has proven an attractive strategy to trade consensus trades at year-end.

More room for DXY to fall there though it will stabilise somewhere around 100 or just below in a soft landing. It will take a harder landing to drive DXY back to recent cycle lows closer to 90.

Europe and China are just too weak.