So says Goldman.

USD: Is adjustment a-justified?

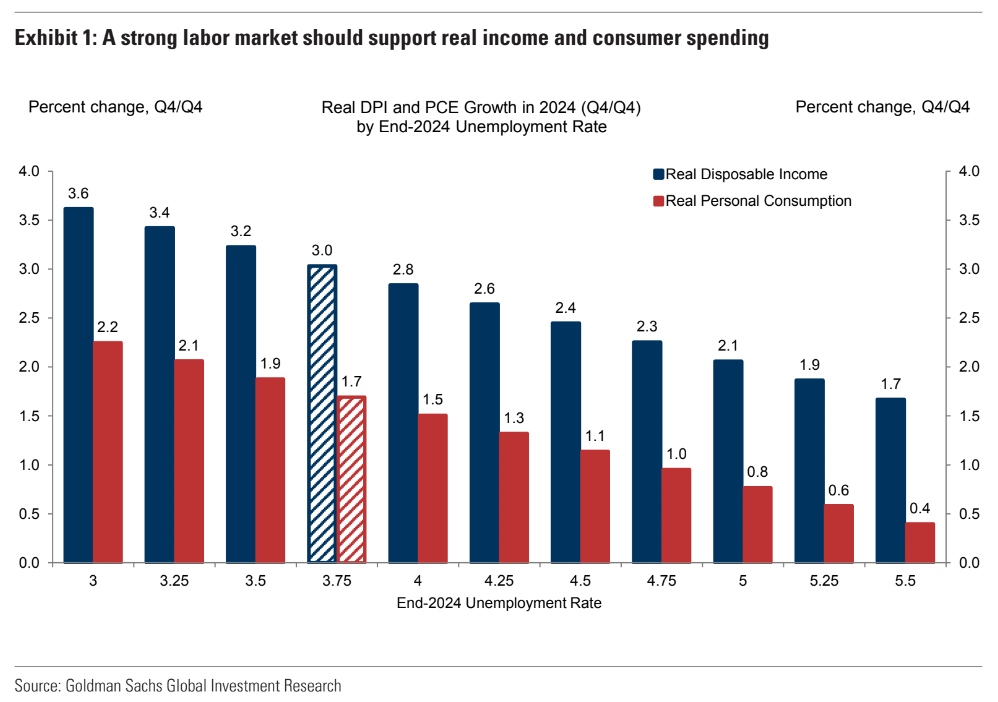

The US unemployment rate fell back to 3.7% in November. That matters for a few reasons.

First, it is in line with the FOMC’s September projections, so there is nothing from the labour market side suggesting a big re-think is needed.

Second, it supports our view of relatively strong real income growth next year, which is a key reason why we expect the US economy to continue to perform well, and much better than consensus (Exhibit 1).

Third, it eliminates perhaps the easiest route to ‘adjustment cuts’ early next year.

While Governor Waller put forth a view that cuts could be considered as long as inflation continues to moderate, he has traditionally placed less emphasis on the Phillips Curve, and we suspect it will at least take longer than current market pricing suggests for the FOMC to come to a consensus on this issue if the labour market stays strong.

At a minimum, recent economic data continue to suggest a more mixed case for rate cuts than elsewhere.

This, combined with our more optimistic view on the US growth outlook leads us to retain our “stronger for longer” Dollar view as we think the market has done “ a bit too much adjustment” and seems to be pricing rate relief as a bigger component to the soft landing than we envision in our baseline.

We would lean against Dollar weakness given the global breadth of the ongoing disinflation and a less resilient activity picture in Europe and China, and the greater plausibility of earlier and faster ECB rate cuts.

AUD won’t rise if DXY doesn’t fall. I still expect a material slowing of the US economy as public and private credit tides go out together. But the basic principles here are right.