By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We retain our call for the RBA to increase the cash rate by 25bp to 4.35% at the November Board meeting.

- Following strong September retail trade data we now ascribe an 80% chance to a 25bp rate increase and a 20% probability to no change (we had previously put the probability of a Cup Day hike at 70%, post the Q3 23 CPI).

- The RBA will publish their full suite of updated economic forecasts in the November 2023 Statement on Monetary Policy (SMP) next Friday.

- We expect the RBA to upwardly revise both their end-23 and end-24 inflation forecasts. But we anticipate they will retain their central scenario that inflation will return to the target band in late 2025.

- The end-23 unemployment rate forecast may be nudged down a touch, but we don’t expect any major changes to the RBA’s forecast profile for the jobless rate.

- The RBA’s forecasts for wages growth are unlikely to be changed.

- GDP forecasts will be upwardly revised for end-23 to reflect upward revisions from the ABS. GDP growth for end-24 may also be nudged higher based on a slower retracement of population growth to its pre-pandemic rate.

Overview:

The coming week is another big one for Australian financial market participants. The RBA November Board meeting on Tuesday comes in the wake of the strong Q3 23 CPI, which contained an upside surprise on the trimmed mean relative to the RBA’s forecast profile.

The November Board meeting also follows the September labour force survey, which indicated the unemployment rate was not far off its cyclical low at 3.6%.

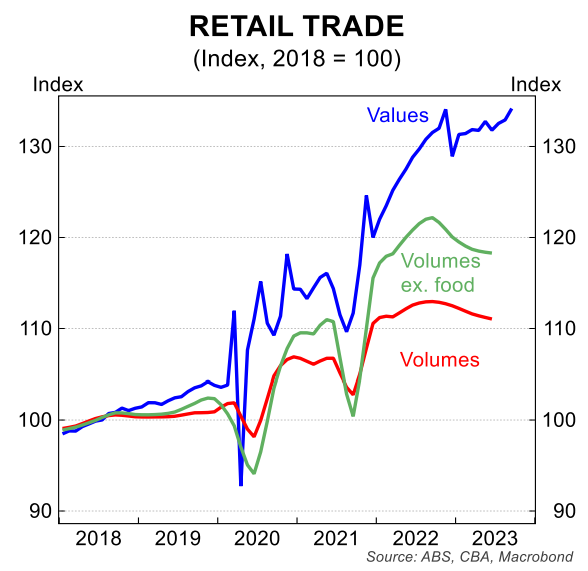

Finally retail trade for September, which printed earlier this week, came in materially hotter than the market median economist anticipated.

The RBA Board will debate the case to extend their four month pause in the tightening cycle or deliver on their tightening bias and raise the cash rate by 25bp to 4.35%. We expect a 25bp rate hike.

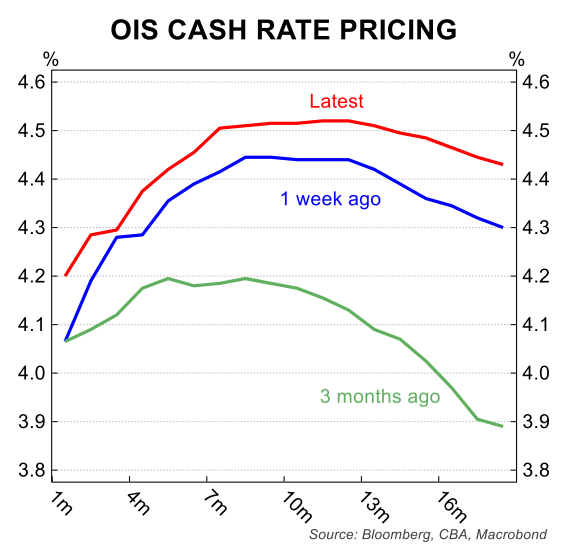

Money markets agree with our view that a rate hike is more likely than not next week. As we go to press a ~70% chance of a 25bp rate increase is priced.

We expect a 25bp Cup Day hike will be the clear consensus call across the forecasting community.

The RBA will also publish an updated set of forecasts in the November SMP on Friday (10/11). The key numbers will be previewed in the Governor’s Statement accompanying the November decision.

Setting the scene – a recap of the RBA in October:

The RBA Board left the cash rate on hold at 4.10% in October, as was widely anticipated. It was the fourth consecutive monthly Board meeting where policy was left unchanged (recall that the last move in the cash rate was a 25bp increase in June, which took the cash rate target to 4.10%).

New Governor Michele Bullock had the opportunity to alter the language and tone in her Statement accompanying the on hold decision in October.

But instead the Governor made minimal changes to the Statement that accompanied the September Board meeting – former Governor Philip Lowe’s last one.

The October Board Minutes, however, struck a more hawkish tone. The RBA’s hiking bias from the September Board Minutes was retained. Namely, that “some further tightening of policy may be required should inflation prove more persistent than expected.”

But importantly, the Minutes contained a new line, which was hawkish. Specifically that, “the Board has a low tolerance for a slower return of inflation to target than currently expected.”

Last week Governor Bullock upped the inflation fighting rhetoric in her maiden speech as Governor at the CBA Global Markets Conference. The Governor stated that, “the Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation”.

We do not know what constitutes a ‘material upward revision to the inflation outlook’. But stating that the Board ‘will not hesitate’ to raise the cash rate further implies the Board has no appetite for a slower return of inflation to target than they previously expected.

Indeed, the Governor made these remarks on the eve of the Q3 23 CPI. The timing suggests it was a reminder to market participants that the November Board meeting is ‘live’. And that the September quarter inflation report will be a critical input into RBA’s assessment of the outlook for inflation.

The case to keep the cash rate on hold in November:

The arguments the Board will debate in favour of leaving the policy rate on hold next week will largely be the ones that were put forward in October.

Monetary policy works with the well documented ‘long and variable lags’. And inflation itself is a lagging indicator.

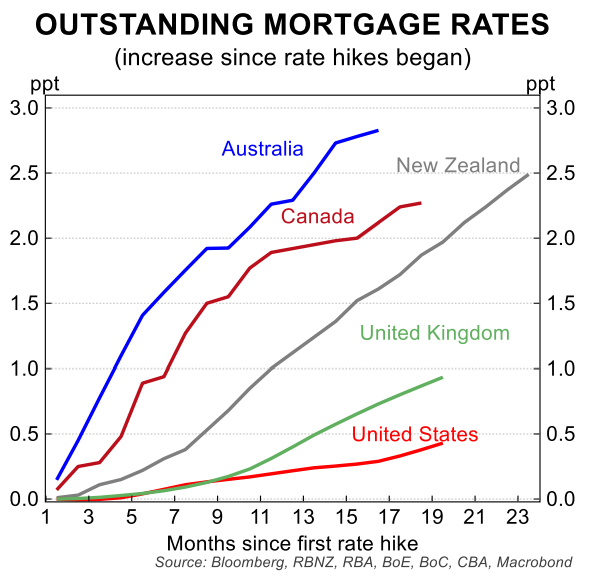

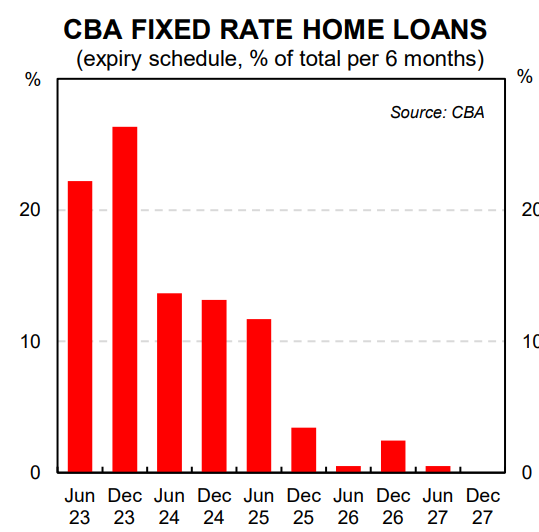

The cash rate has been increased significantly in a short period. And the fixed rate rollover is still continuing, which means policy is still organically tightening.

In short, the effects of tighter policy are still to fully play out in the activity and inflation data.

The Board can also make the case again that the labour market has reached a turning point. The unemployment rate dipped by 0.1ppt to 3.6% in September.

But hours worked fell over the September quarter and job vacancies continue to trend down. Indeed the Governor reiterated her view that the labour market has turned in her appearance before the Senate Economics Legislation Committee on 26 October (i.e. after the September labour force survey was published).

Finally, the Board could judge that the outlook for inflation has not changed ‘materially’ despite the stronger-than-expected Q3 23 CPI. That is the view of the Federal Treasurer.

At his press conference following the publication of the Q3 23 CPI the Treasurer stated, “the Reserve Bank looks for material changes in the inflation outlook …. but what we’ve seen today [i.e. the inflation data] is consistent with our expectations, it doesn’t materially change the inflation outlook going forward.”

It is unclear if the RBA Governor shares the same view on the inflation outlook as the Treasurer. But it is important to note that the Treasury Secretary, Steven Kennedy, is a member of the RBA Board.

The RBA’s sway on the Board is slightly lessened at the moment given the Treasurer has not yet appointed a new RBA Deputy Governor.

The RBA Deputy Governor sits on the Board. But there is no acting Deputy Governor, which means the RBA Board currently has only one representative from the RBA – the Governor.

It is unusual to see the Deputy Governor’s position still vacant given the Treasurer appointed Michele Bullock to the Governor’s position on 14 July (her appointment meant the Deputy Governor position was vacated).

The Board may reach the conclusion that there is merit in extending the pause in the tightening cycle to further assess trends in spending and the outlook for inflation and the labour market.

This is a valid consideration. But the Board will weigh up these factors against the case to tighten policy.

The case to raise the cash rate in November:

The case to increase the cash rate by 25bp in November hinges on the Board’s assessment of the outlook for inflation.

Indeed, the RBA’s updated economic forecasts will be a critical input to the Board’s decision, so we start with our expectations for the RBA’s new inflation forecasts.

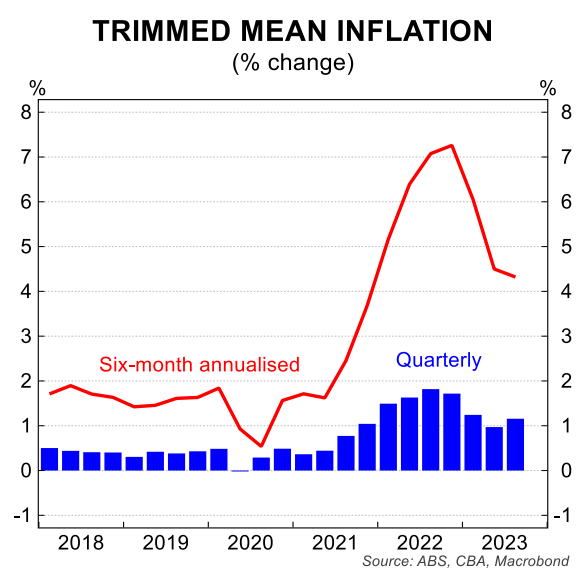

The RBA’s implied profile from the August SMP put Q3 23 trimmed mean, the Bank’s preferred measure of core inflation, at ~4.8%/yr.

The Q3 23 trimmed mean printed at 5.2%/yr. As such, the annual rate of core inflation in Q1 23 was 0.4ppts higher than the RBA’s forecast (note the 0.4ppt differential comprised a 0.3ppt miss on Q3 23 and a 0.1ppt upward revision to the Q2 23 trimmed mean CPI).

This stronger-than-anticipated core inflation outcome will mechanically result in the RBA upwardly revising their near term inflation forecasts. But we think the RBA will also upwardly revise their end-2024 annual core inflation forecast (currently 3.1%).

The inflation profile for 2025 is unlikely to be changed. More specifically, we expect the RBA will retain its central scenario that inflation will return to the target band in late 2025.

The RBA can simply state that a rate increase in November will contribute to greater certainty that inflation returning to the target band by late 2025 (here we note that the RBA’s updated forecasts will be conditional on at least one further 25bp rate increase).

Other data that will feed into the case to increase the cash rate in November relates to the activity side of the economy.

The unemployment rate has been slower to rise than the RBA expected (the RBA is likely to nudge down their near term unemployment rate forecasts). And retail trade was particularly strong in September, rising by 0.9%/mth.

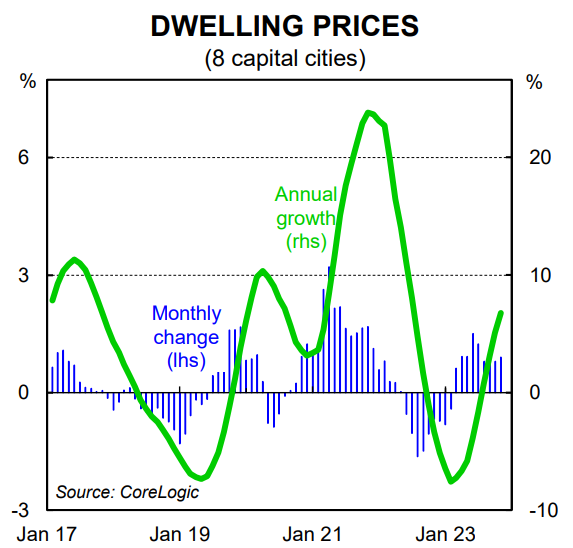

The RBA have spoken more recently about the risk that rising home prices will see stronger than otherwise household consumption. And the September retail figures may cause them some discomfort.

Our expectation is that the September spike in retail trade was a one-off. And we expect more modest monthly prints from here, notwithstanding volatility around Black Friday and Cyber Monday.

But the RBA may feel a sense of urgency to tighten policy further given inflation has surprised to the upside, home prices continue to rise and the retail trade figures showed a solid lift in spending over September.

The RBA Board may also judge that an increase in the cash rate in November could elicit a greater behavioural response from the household sector than any previous individual 25bp rate increase.

For households on a floating rate mortgage, another rate rise just before Christmas would further tighten budgets. And it would also send a clear signal that the tightening cycle is not necessarily over.

A November rate hike would marry up with the RBA’s rhetoric that it will do what is necessary to return inflation to target within a reasonable time frame.