Westpac with the note.

- Leading Index growth rate dips to –0.40%.

- Economy set to remain stuck in ‘low growth rut’ well into next year.

- Range of headwinds continues despite improvement since start of the year.

- Components show cooling labour market, unsettled financial markets and shaky confidence are now the main weak spots.

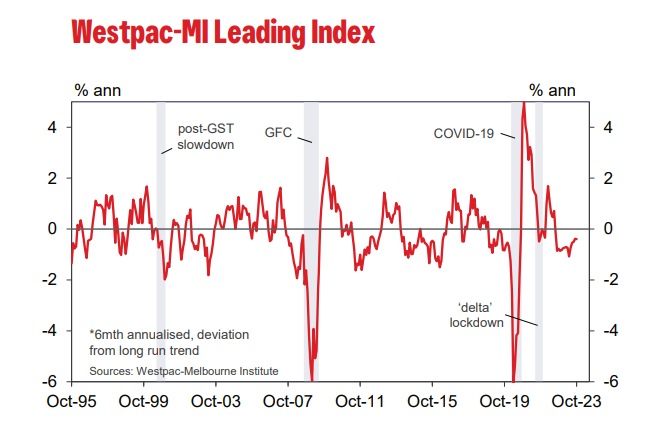

The Leading Index shows little change in the Australian economy’s sub-par performance. October marks the fifteenth successive sub-zero read on the Index growth rate – signalling that the activity is set to remain in the ‘low growth rut’ that has prevailed throughout 2023 well into 2024.

Note that this is still consistent with moderately positive growth in absolute terms. With Australia’s population currently growing at around 2.4%yr, our ‘trend’ GDP growth rate is well above 3%yr even under very conservative productivity assumptions. Both Westpac and the RBA expect actual growth to be in the 1-2% range both this year and next, tracking well behind any reasonable estimates of trend.

While the Leading Index growth rate remains negative, it has improved marginally over the last six months, lifting from –0.7% in March to –0.4% in October. The main components driving the shift have been a widening yield spread (adding +0.67ppts to the headline growth rate) – led by surging long term interest rates – and a stabilisation in dwelling approvals (+0.27ppts). Recent gains in commodity prices, measured in AUD terms, have also provided some support, albeit with prices still coming off a significant correction since late last year.

These positives have been partially offset by slower growth in aggregate monthly hours worked (taking –0.41ppts off the Index growth rate); and a correction in the S&P/ASX 200 (–0.34ppts).

Note that developments in November may see some of these shifts reverse partially. In particular: the yield spread has narrowed significantly following the RBA’s November rate rise and a rally in global bond markets; and both the AUD and equity markets have risen materially.

The Reserve Bank Board next meets on December 5. Today’s release again highlights the sluggish growth environment that looks set to carry well into the new year. Whether its sluggish enough to bring inflation back to the RBA’s 2-3% target range over an acceptable timeframe remains the RBA Board’s central concern.

As reiterated in the recently-released minutes from its November meeting, the Board continues to have a low tolerance for any further upside surprises or delays in the return of inflation to the target range. As such, policy meetings next year will be very much ‘live’.