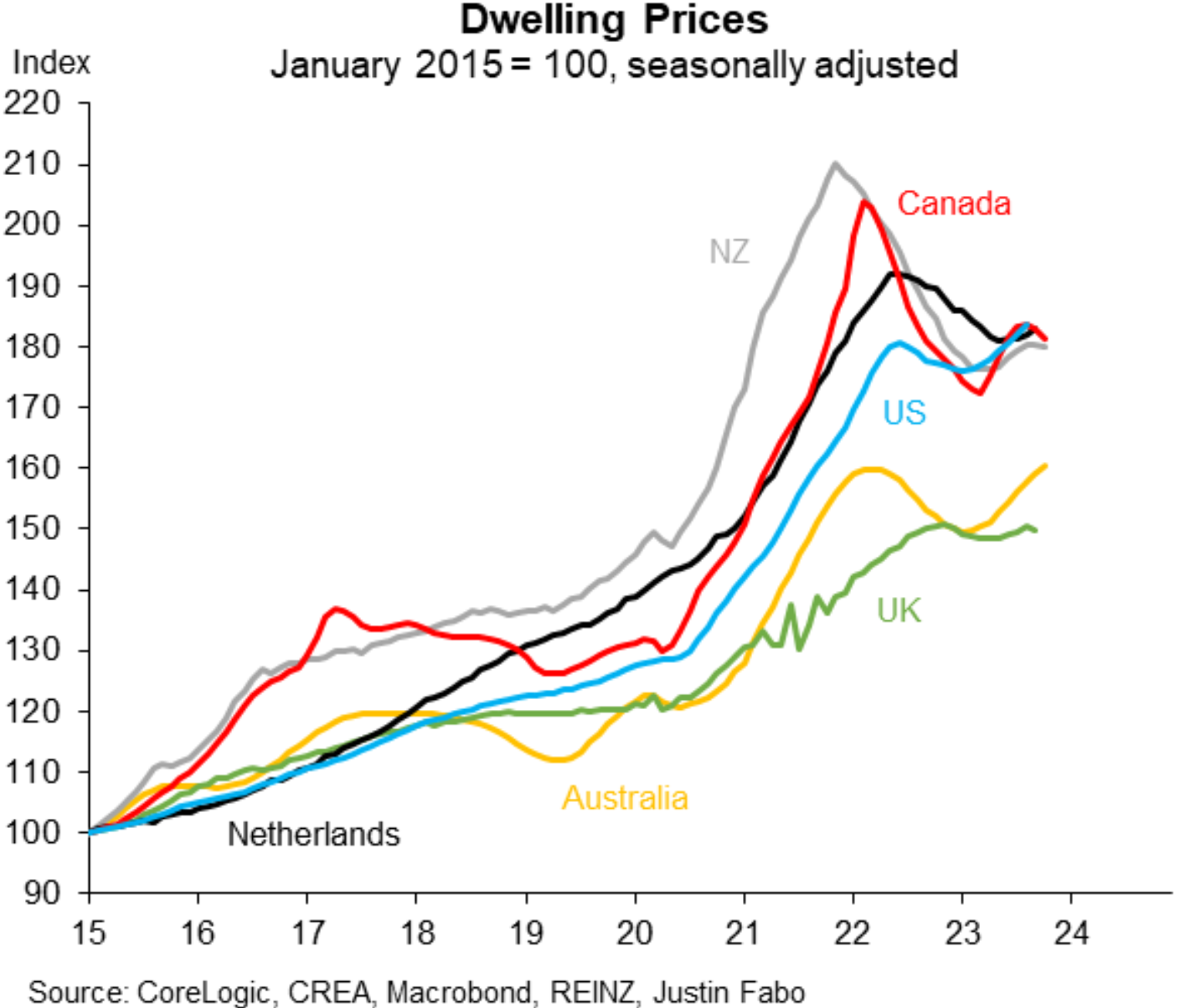

Justin Fabo from Macquarie Group published the below chart last week on Twitter (X) showing that “housing prices appear to be rolling over in Canada and NZ (and possibly the UK)” But “growth in Australia is slowing but still solid”:

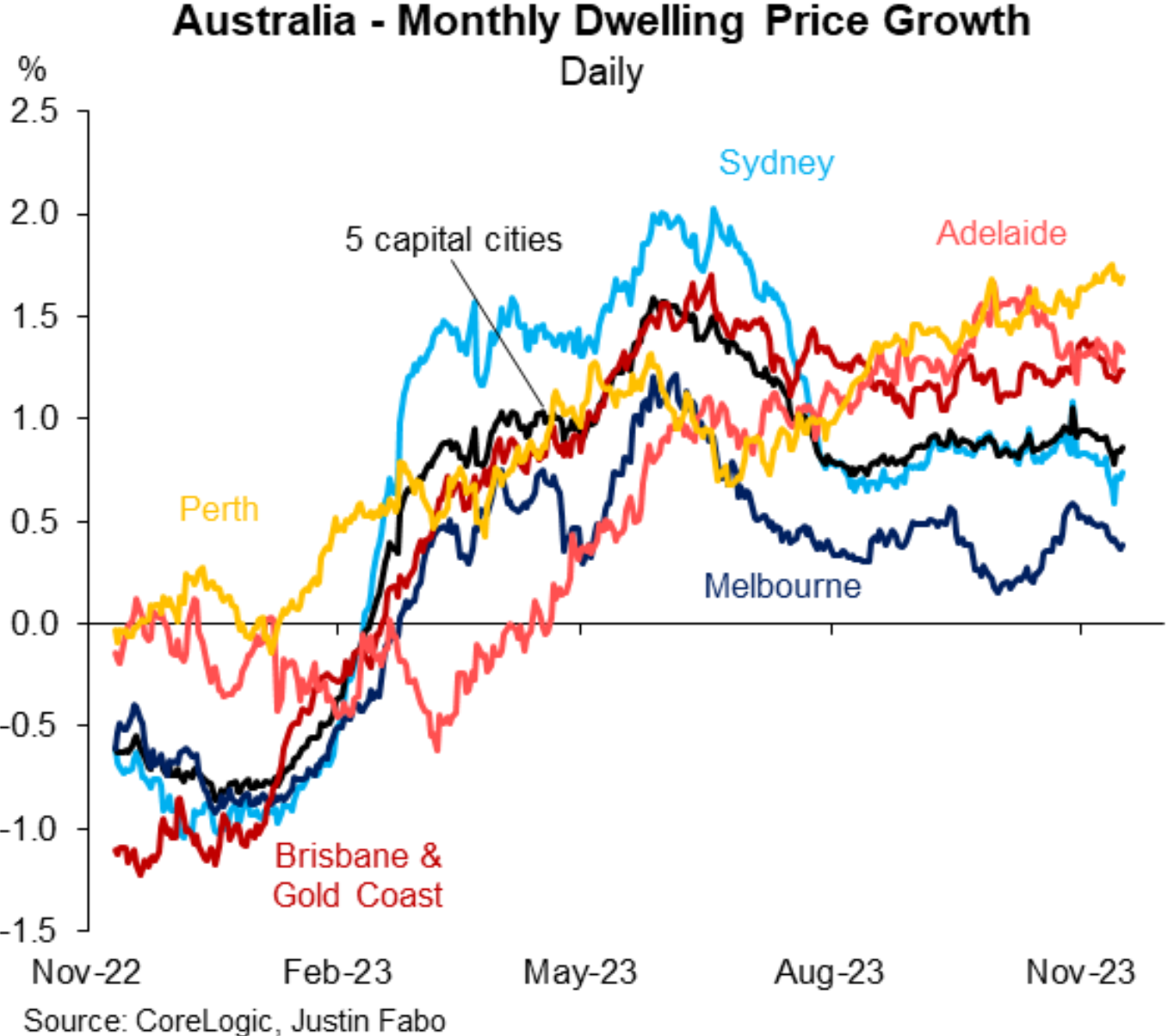

CoreLogic’s daily dwelling values index continues to record around 0.8% monthly growth at the 5-city aggregate level, with minimal movement over recent months:

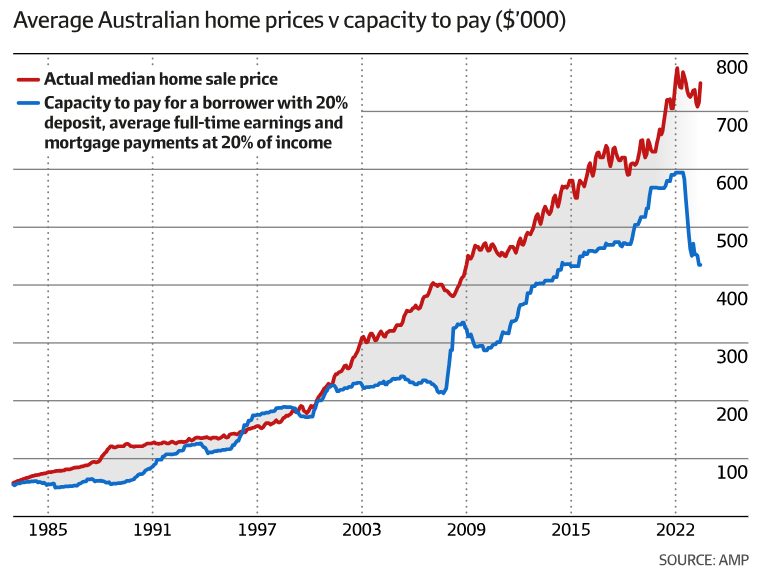

Australia’s house price rebound has defied gravity, given it coincided with a circa 30% decline in borrowing capacity before this month’s rate hike by the RBA:

The big question looking ahead is: Can Australian home values continue to defy gravity? Or will they follow the path of the other markets and roll over?

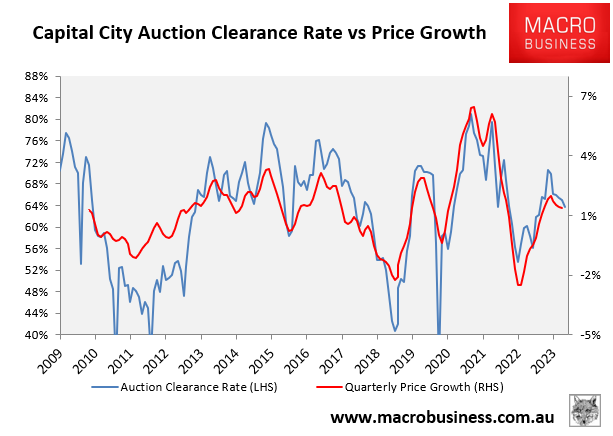

Over recent months, we have seen the nation’s auction clearance rate trend lower, which has historically been a strong leading indicator for price growth:

The latest interest rate hike from the RBA appears to have taken some steam out of the market. And if the RBA follows-up with another rate hike in December or February, then it risks being the straw that broke buyers’ backs.

On the other hand, Australia’s population growth continues to go from strength to strength.

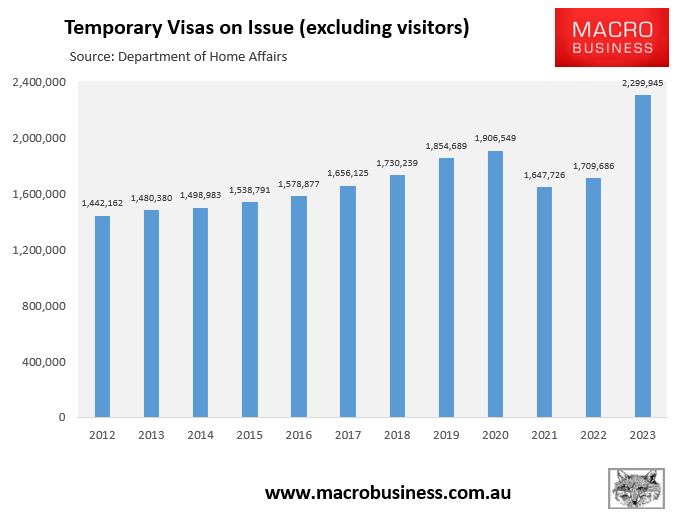

The latest data from the Department of Home Affairs showed that the number of temporary visa holders (excluding visitors) hit a record high 2.3 million people in September, which was an increase of nearly 600,000 people year-on-year:

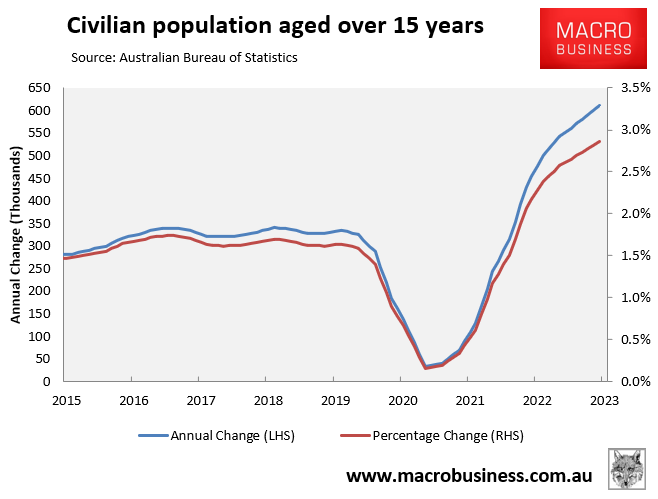

In a similar vein, the latest labour force data from the ABS showed that the civilian population aged 15 years and over grew by a record 612,000 (2.9%) in the year to October:

This record population growth is the primary reason why both house prices and rents have risen so strongly.

Therefore, my guess is that Australian home value growth will merely slow rather than outright decline heading into 2024.

It is difficult to see how a “buyers’ market” will develop when the sheer number of buyers is growing so strongly.