The local gas spot price is still hovering around a preposterous $12Gj:

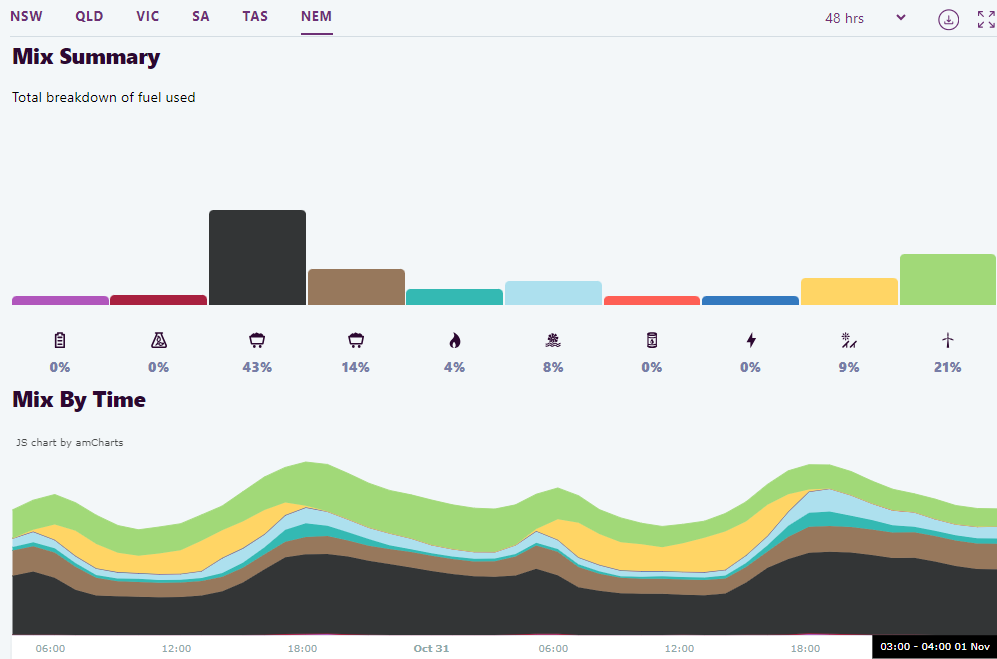

Alas, wind and hydro have dropped, so gas-fired power rose closer to its 5% average:

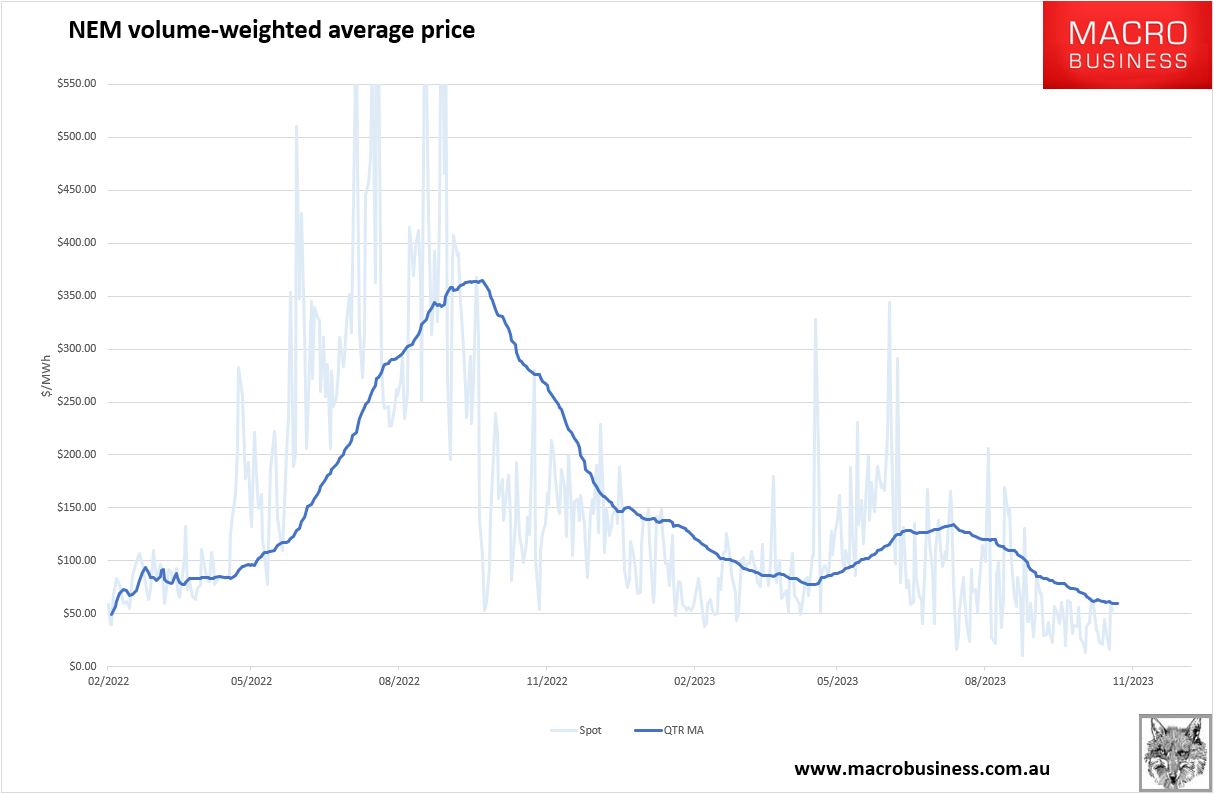

Lifting power costs, though the quarterly average is still around $59MW/h, embedding big bill relief next year if it holds:

Futures prices for power have also improved, but note that the further out we go, the less coal we have and more gas we’ll need, raising prices again:

There is no more news on the Origin deal to monopolise LNG imports via Venic Energy. But there is this:

Brookfield and EIG Partners have hit back in the takeover battle for Australia’s biggest utility Origin Energy, increasing their offer to $9.53 a share and declaring it their best and final bid.

The ACCC should have demanded the divestiture of the Eraring coal-fired power station for this dal to go ahead, which is about to gouge NSW punters via subsidies to stay open. Then, no raised bid would be necessary.

As well, it makes no sense to give any member of the gas export cartel – ORG, WDS, STO, EXXON or Shell – control of gas import volumes.

It is begging to be pillaged.