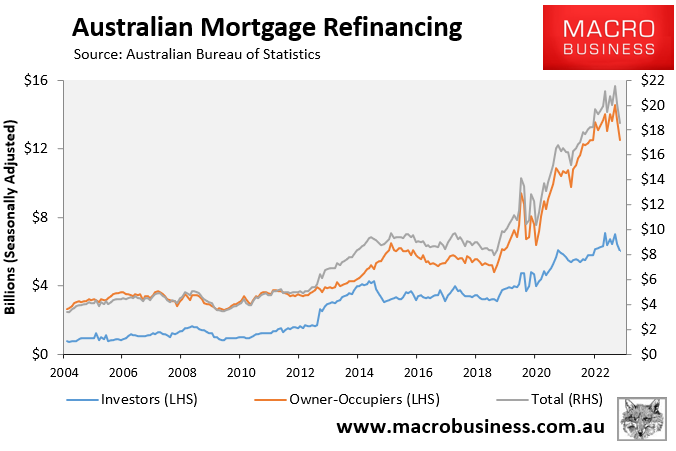

Over the past three years, Australia saw the greatest recorded increase in mortgage refinances on record.

Monthly mortgage refinances increased from around $10 billion in mid-2020 to a peak of $21 billion in mid-2023, according to the Australian Bureau of Statistics (ABS).

However, the mortgage refinancing boom looks to have finally run out of puff, with the total number of refinances falling heavily to $18.5 billion in September:

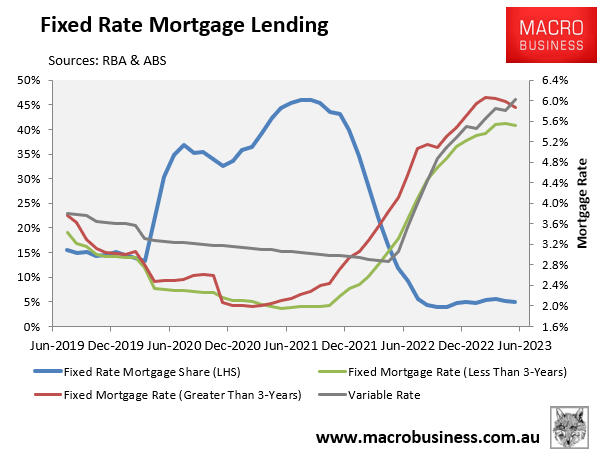

The boom in mortgage refinancings was driven by the large numbers of borrowers that were forced to renegotiate fixed-rate mortgages taken out when interest rates were at historical lows during the pandemic:

These borrowers have moved from ultra-low fixed-rate loans of around 2% to variable rates of between 6% and 7%, forcing many to seek a better deal with a different lender.

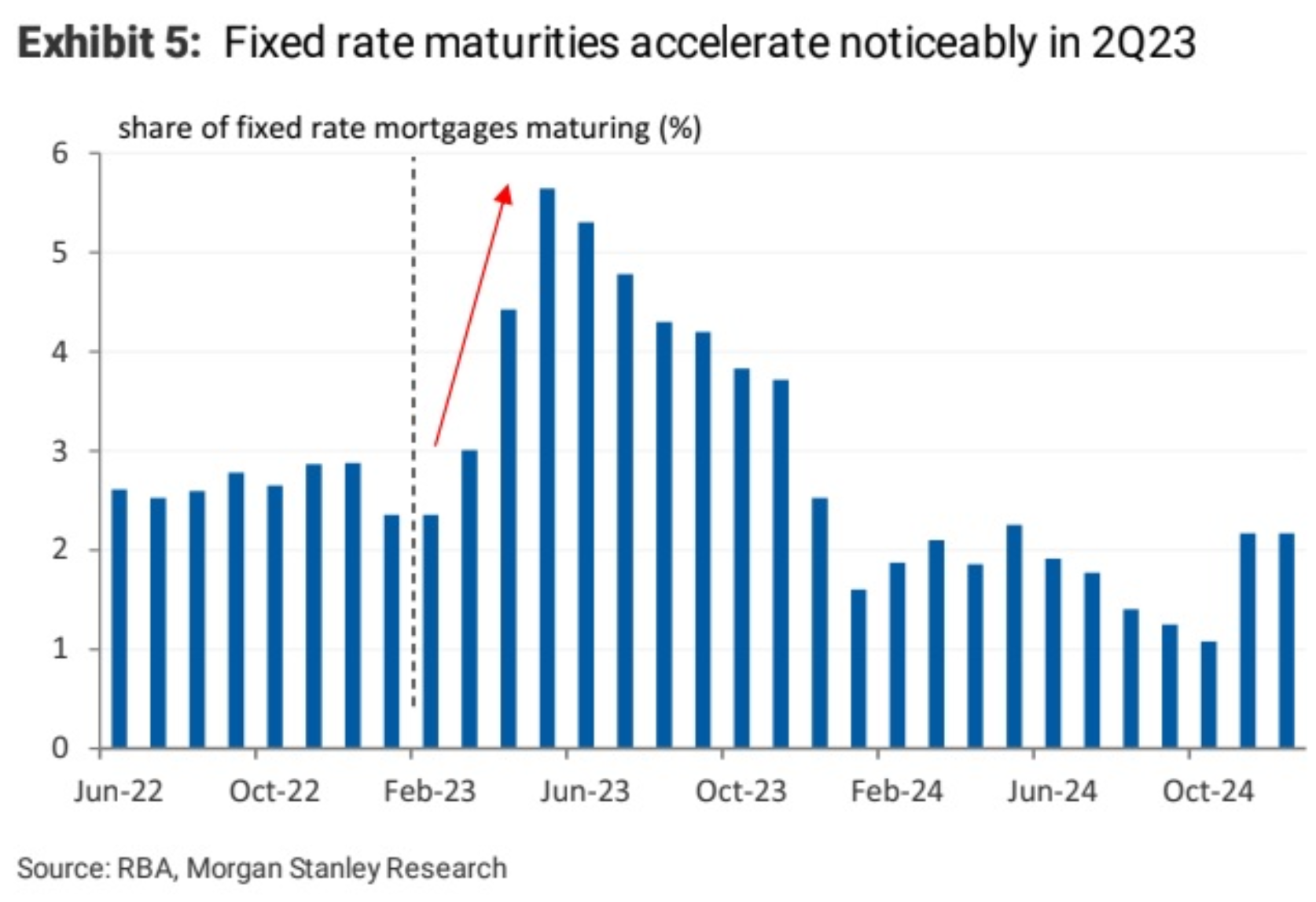

The fixed-rate mortgage ‘cliff’ has largely run its course, given most of the cheap pandemic fixed rates have expired:

This suggests that the volume of mortgage refinancing should continue to fall going forward.

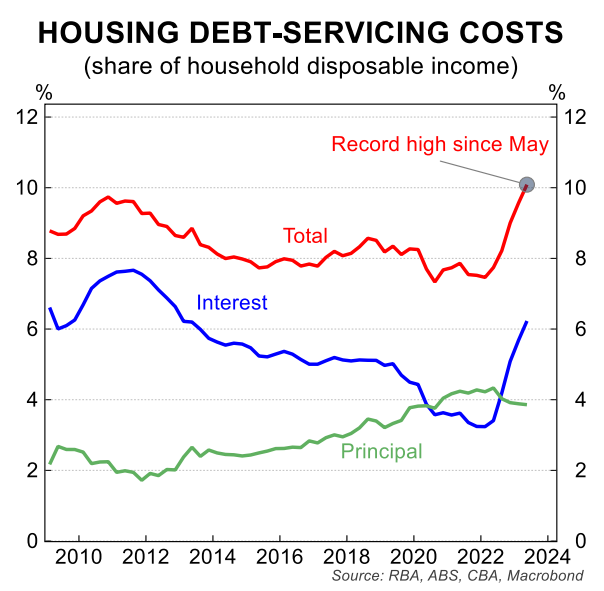

That said, Australian households are now paying a record share of their incomes on debt repayments:

And this will only rise if the RBA continues to lift the official cash rate above its current level of 4.1%.

Therefore, I expect mortgage refinancing activity to remain higher than average next year, despite the end of the fixed rate cliff.

If you are looking to save thousands of dollars in mortgage repayments, try the MB Compare n Save mortgage comparison tool. It takes less than a minute.

And if you choose to refinance, Compare n Save will handle the process.