By Gareth Aird, head of Australian economics at CBA:

Key Points:

- The already released prices data for October suggest that inflationary pressures have cooled over the early part of Q4 23.

- Price measures in the NAB Business Survey, JudoBank PMIs and the MI Inflation Gauge all eased in October.

- The private survey data reduces the probability of an upside surprise on Q4 23 CPI relative to the RBA’s latest forecasts in the November Statement on Monetary Policy (SoMP).

- The official ABS October monthly CPI indicator is due on 29 November.

Overview:

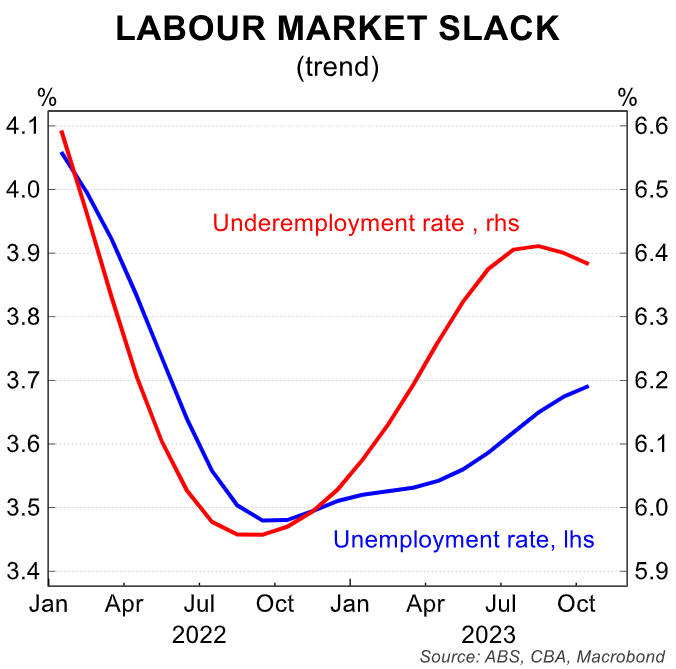

The RBA’s December Board meeting is not currently ‘live’. The Q3 23 WPI printed largely in line with the RBA’s latest forecasts. And the unemployment rate ticked up by 0.1ppt in October to 3.7%.

Both of these outcomes support no change in the cash rate at the December Board meeting (to be held on 5 December).

The monthly CPI indicator for October is due on 29 November. But it’s only a partial read on inflation over the month. The ABS does not survey all of the components of the inflation basket each month.

Indeed, the CPI indicator for the first month of each quarter contains more price updates for goods relative to market services. These are typically measured only once a quarter –in the second month of the quarter.

The RBA’s concerns on the inflation front are skewed towards the market services side. As such, we must wait until the November monthly CPI indicator prints for a more comprehensive official update on how services prices are tracking.

That said, the ABS monthly CPI indicator is not the only measure of price changes in the domestic economy. There are other ‘second tier’ private surveys that provide timely updates on the inflation pulse, which includes market services.

The already released prices data for October in the NAB Business Survey, Judo Bank Purchasing Managers’ Index (PMIs) and Melbourne Institute Inflation Gauge suggest that inflationary pressures have eased over the early part of the December quarter. This is important. And also encouraging.

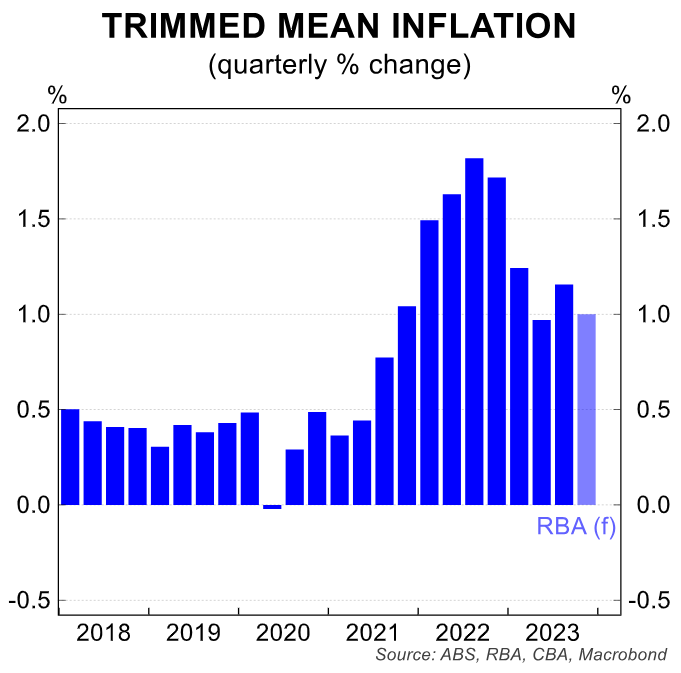

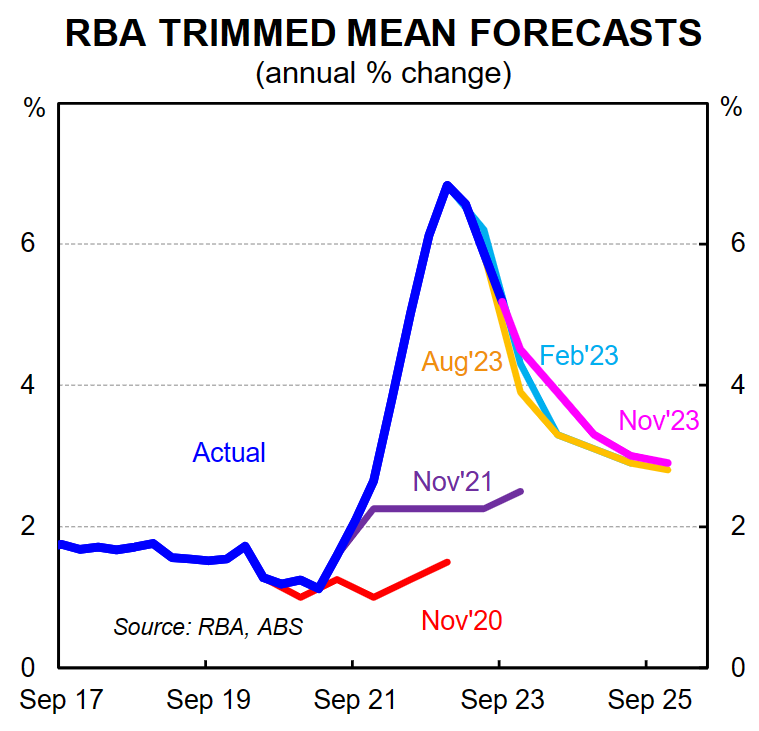

The RBA’s forecast for headline CPI to be 4.5%/yr in Q4 23 means that the RBA expects a ~1.0%/qtr outcome in the December quarter.

For trimmed mean inflation, the more important measure for monetary policy, the RBA has forecast 4.5%/yr in Q4 23. This means they expect a ~1.0%/qtr outcome.

The RBA will almost certainly leave the cash rate on hold in February 2024 if core inflation prints at or below their forecast.

Conversely, the RBA will likely tighten policy again if the inflation data comes in stronger than their forecast, as they did in November.

With inflation the main game in town we are monitoring all of the available prices series to better understand how inflation is tracking ahead of the official data.

We go through the recent prices gauges in the key private surveys.

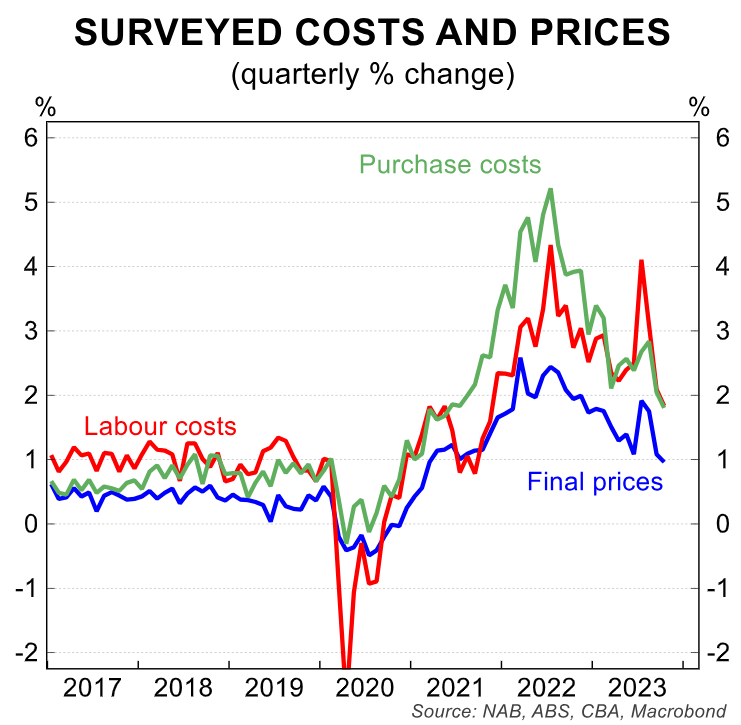

NAB Business Survey:

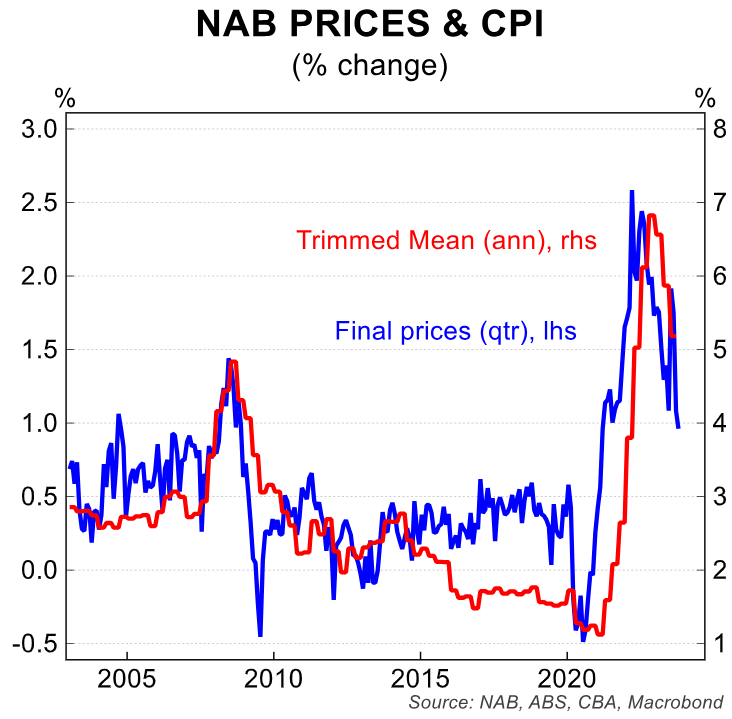

The October NAB Business Survey, released 14/11, indicated price and cost growth slowed in the month.

Final prices growth, which is most closely correlated with consumer prices, eased to 1.0% (quarterly rate). This was the slowest pace of growth since July 2020.

Growth in final prices was still firm, but the direction of travel was encouraging. Both growth in labour costs and purchase costs also cooled.

The anomaly in the trend over the past year was in July. Labour costs and final prices both spiked. But this is primarily because of the big lift in the minimum and award wage which kicked in at the start of the 2023/24 financial year.

The sharp increase in the award wage saw labour costs and final prices jump by more than is seasonally usual in July.

It appears that firms, where possible, responded to the lift in labour costs in July by raising consumer prices straight away.

The official data supports this idea given that the Q3 23 WPI rose by a big 1.3%/qtr and Q3 23 trimmed mean CPI popped by 1.2%/qtr after a 1.0%/qtr lift in Q2 23.

The good news is that the downward trend in labour costs and final price growth in the NAB Business Survey has been restored.

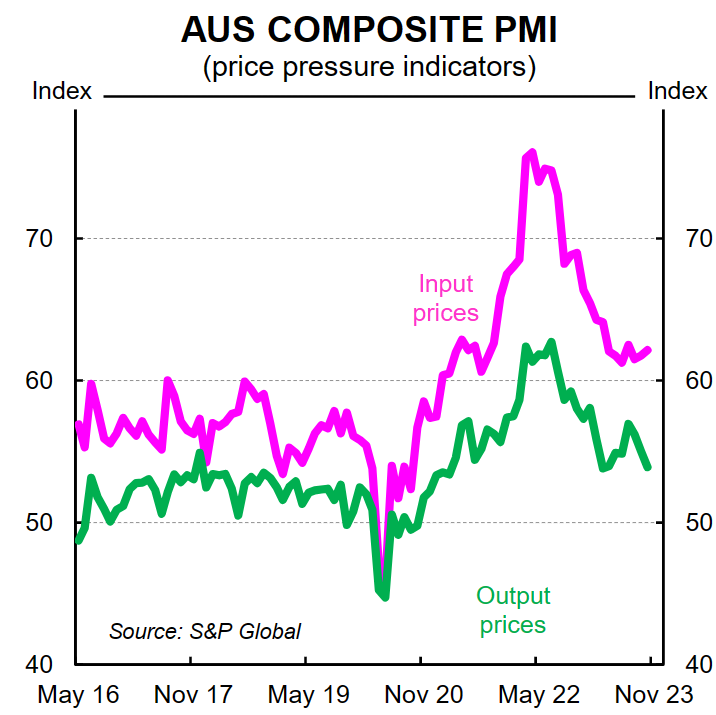

Judo Bank PMIs

The October Judo Bank PMIs paint a similar picture on the prices side of the economy to the NAB Business Survey (the Judo Bank PMI is part of the S&P Global suite of PMIs).

Note that the PMIs are diffusion indices, with a reading >50 indicating an overall increase compared to the previous month and <50 an overall decrease.

Output prices in the Composite PMI rose at their slowest monthly pace in October since March 2023 (53.9 in October vs 53.8 in March – the difference is trivial).

And the March 2023 reading was the lowest since March 2021. The Composite PMI is weighted based on contributions to GDP, so the services component is much more important than the manufacturing one.

Average selling prices on the services side increased at the softest pace in seven months in October –a welcome development.

To be clear, the growth in prices is still robust. But the direction of travel is desired. Indeed, we take additional comfort from the PMIs on the inflation front given they exclude the retail sector where price rises have been less strong recently.

The November Judo Bank ‘Flash’ Composite PMI is set for release this week (23/11). It will provide a timely update on consumer price changes in the economy for the first three weeks of November.

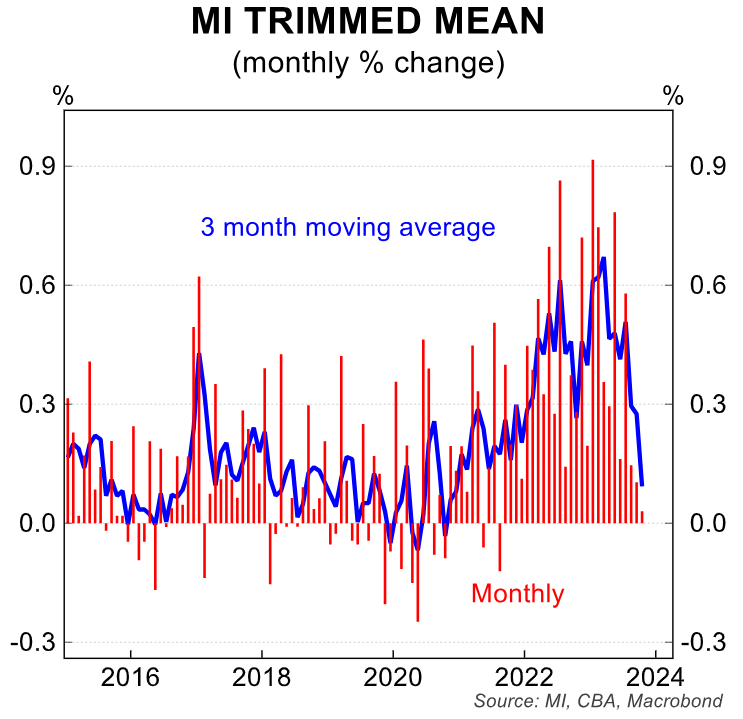

Melbourne Institute (MI) Inflation Gauge:

The MI Inflation Gauge was particularly soft in October. The headline gauge declined by 0.1%/mth.

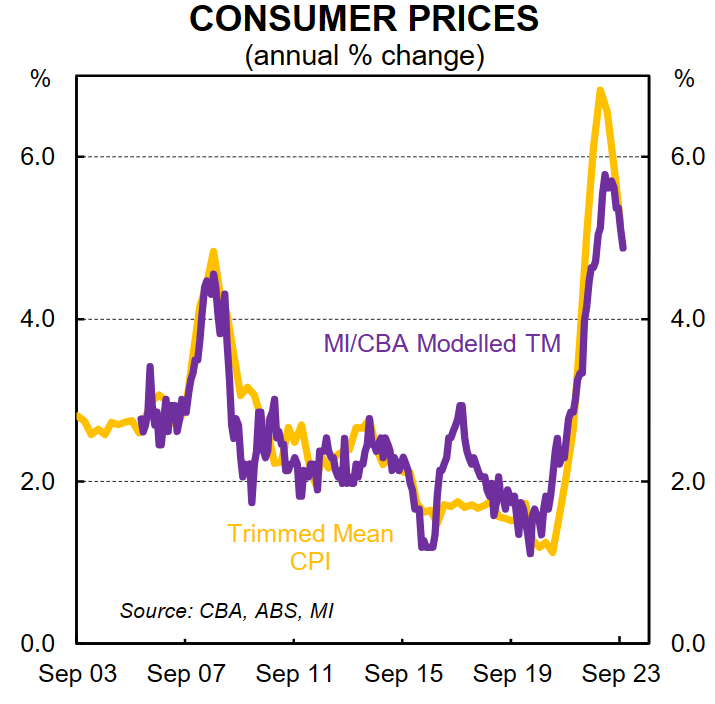

The more policy relevant trimmed mean was flat over the month. The relationship between the MI trimmed mean Inflation Gauge and the official trimmed mean is not perfect. And there are often times when the two series don’t quite marry up.

Notwithstanding, there is a good relationship between the two series over an extended timeframe, particularly when we run it through our own model.

The upshot is that the MI trimmed mean gauge is sending a similar signal to the business surveys, albeit the signal is a little stronger.

Namely that the inflation pulse has cooled in the early part of the December quarter compared to the September quarter.

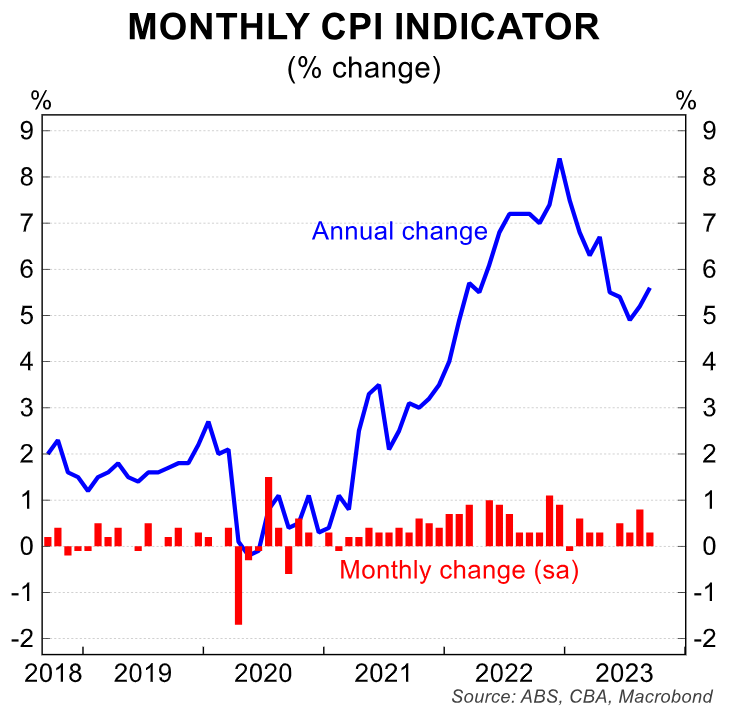

The October monthly CPI indicator:

The official October monthly CPI indicator will print on 29 November. We expect to see inflation ease in the month after firming in August and September.

Here we note that the methodology used by the ABS means that the lift in services inflation that would have occurred in July due to the big increase in the minimum and award wage would have been largely captured in the August monthly CPI indicator rather than the July data.

Our forecast for the October monthly CPI indicator is a flat outcome on the month and for the annual rate to dip to 5.2% (from 5.6% in September).

My colleague Stephen Wu notes that key drivers of easing inflation in October will be: a temporary softer read on rents, owing to the impact of the increase in the Commonwealth Rent Assistance scheme; a decline in electricity prices as newly eligible households receive the government’s energy rebate; and a decline in petrol prices somewhat offset by higher diesel prices.

Discounting in the retail sector and an earlier start to sales events will also play a role.

Expected to be working the other way is continued price pressures from new dwelling construction costs and higher health insurance premiums.

Some health insurance providers delayed price increases, which typically occur in April.

Implications for the RBA:

The RBA has a hiking bias. But they are almost certain to leave the cash rate on hold at the December Board meeting, following the November 25bp rate increase.

There was nothing in the Q3 23 WPI or October labour force survey to see the RBA pull the rate hike trigger again in December.

And there is simply not enough other economic information ahead of the December meeting for the Board to move rates higher.

Our internal data points to a fall in retail trade of 0.6%/mth in October (due for release on 28 October). Therefore we think it would take something extraordinary in the October monthly CPI for the December Board meeting to be ‘live’.

Looking further ahead, the November monthly CPI indicator will be an important print for markets (due 10 January).

It will provide an official update on how market services prices are tracking in the December quarter.

And importantly it will allow analysts to compare how the prices data in Q4 23 is tracking against the RBA’s expectations.

At this stage we expect Q4 23 trimmed mean CPI to be 0.9%/qtr and 4.4%/yr. Our forecast is just below the RBA’s expectations of 1.0%/qtr and 4.5%/yr.

As such, we don’t have a February rate hike in our profile (our base case has 4.35% as the peak in the cash rate). But as the RBA rightly notes that there are both upside and downside risks to the inflation outlook.

And the RBA assesses that upside risks to inflation have increased (we are not as convinced given our expectations for the economy to slow more than the RBA anticipates in 2024).

The RBA’s assessment of the inflation risks mean that the Board is likely to have very little tolerance for an upside surprise in the Q4 23 CPI (due 31 January).

As such, markets are right to price the chance that policy is tightened again in February.