DXY sagged Friday night:

That was enough for AUD upleg:

CNY is stalled:

Gold up, oil down:

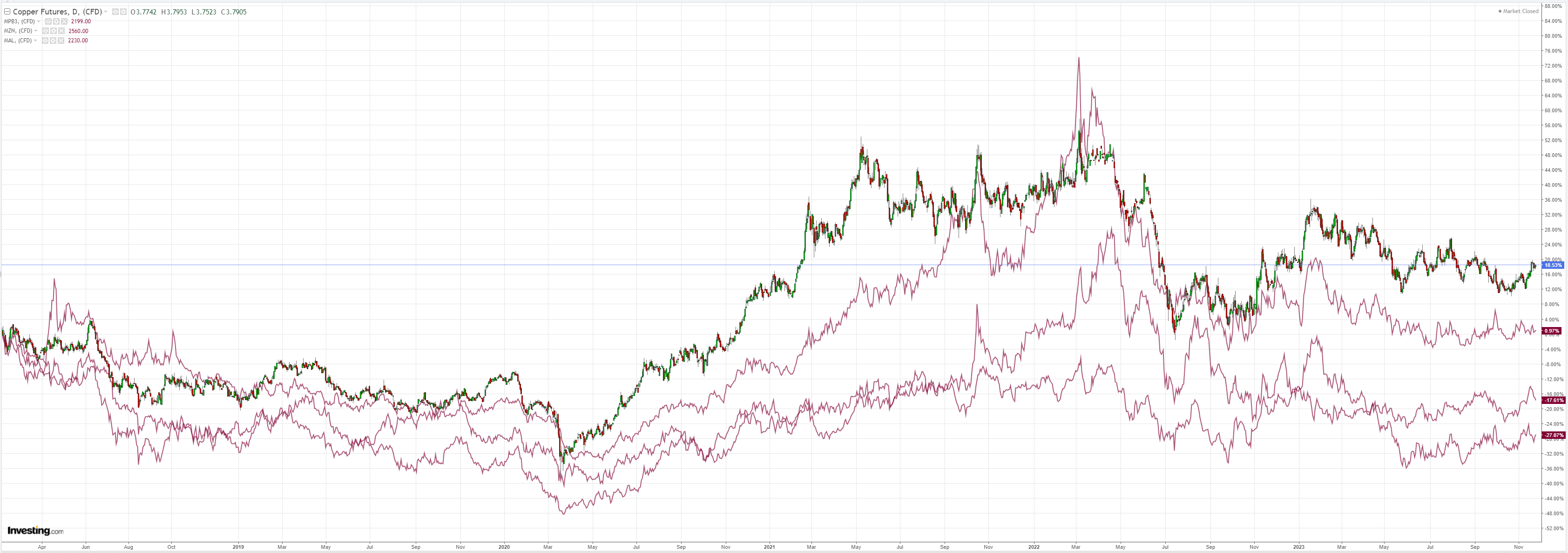

Dirt is in the great sideways:

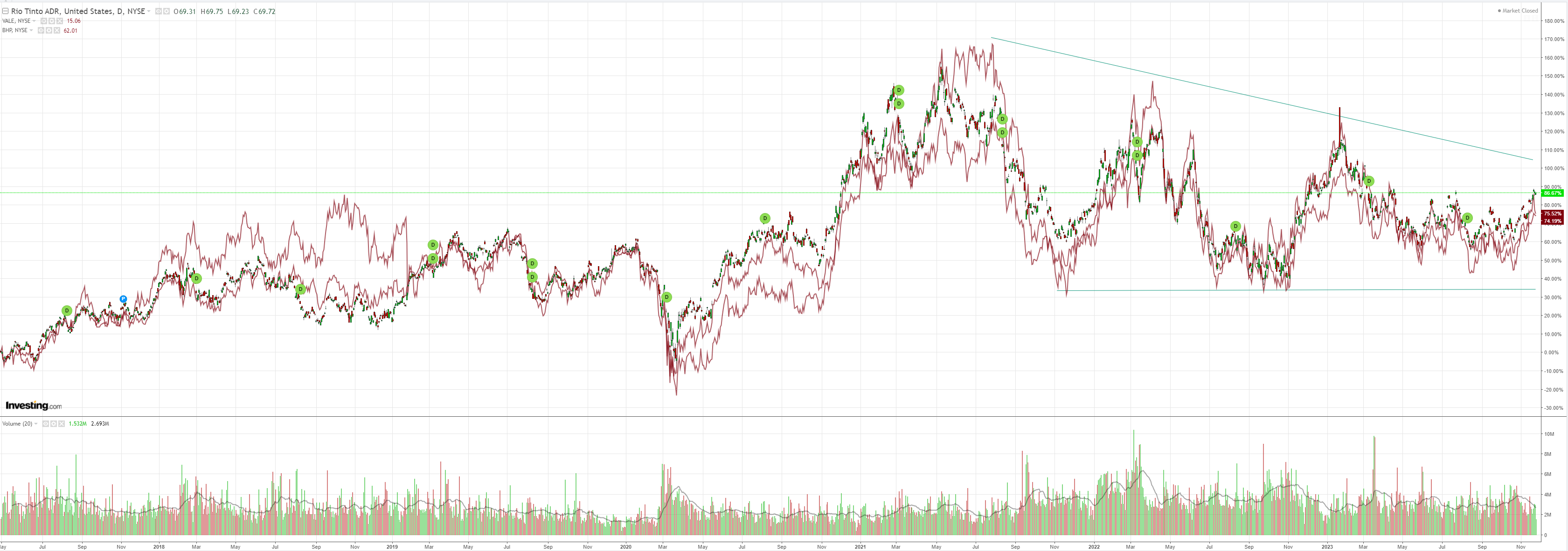

Miners are going to be a nice short soon:

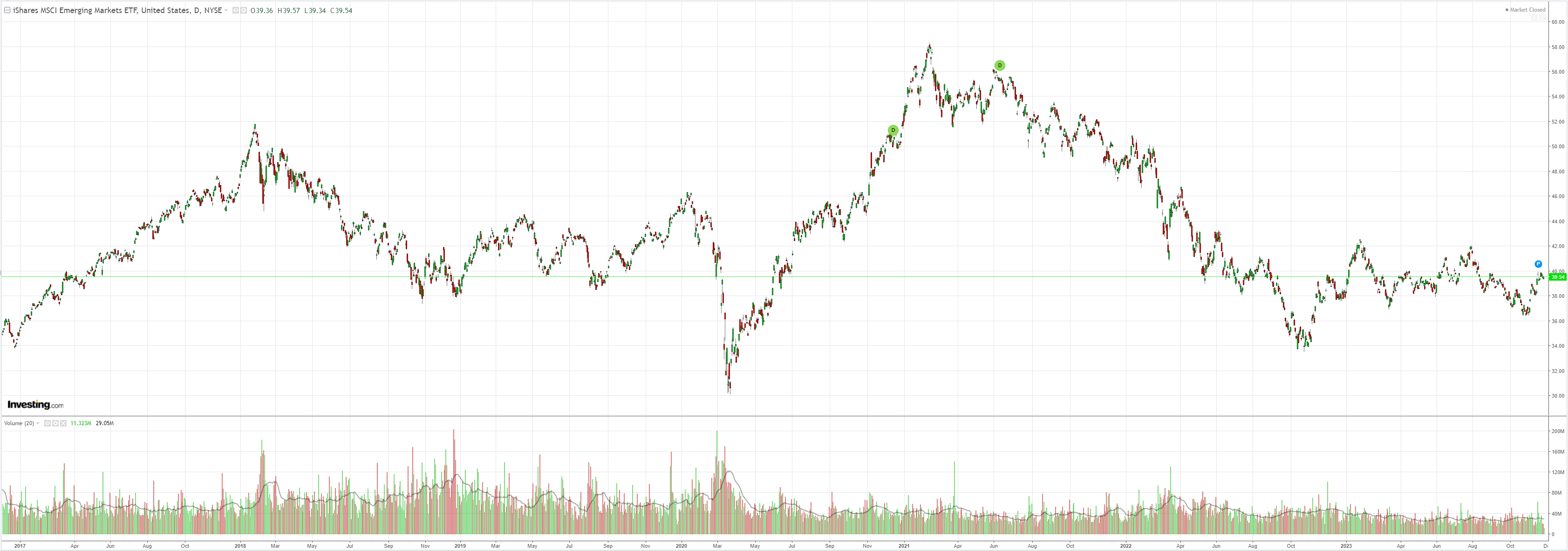

EM faded:

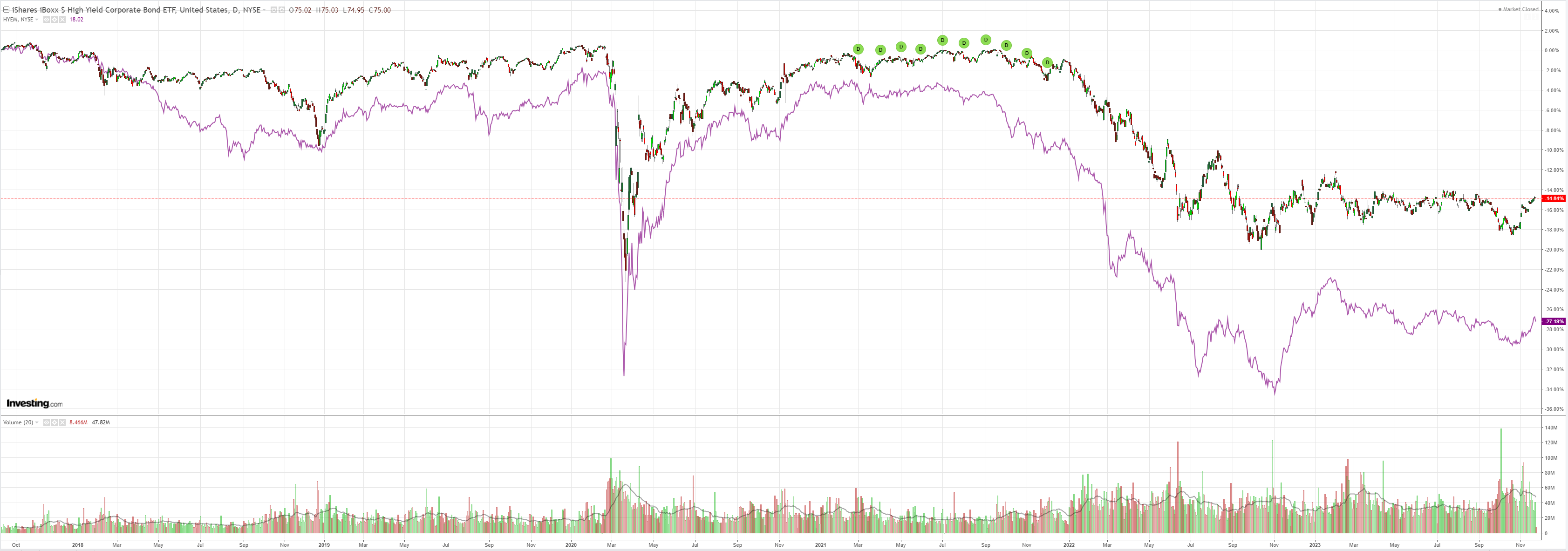

Junk rolled:

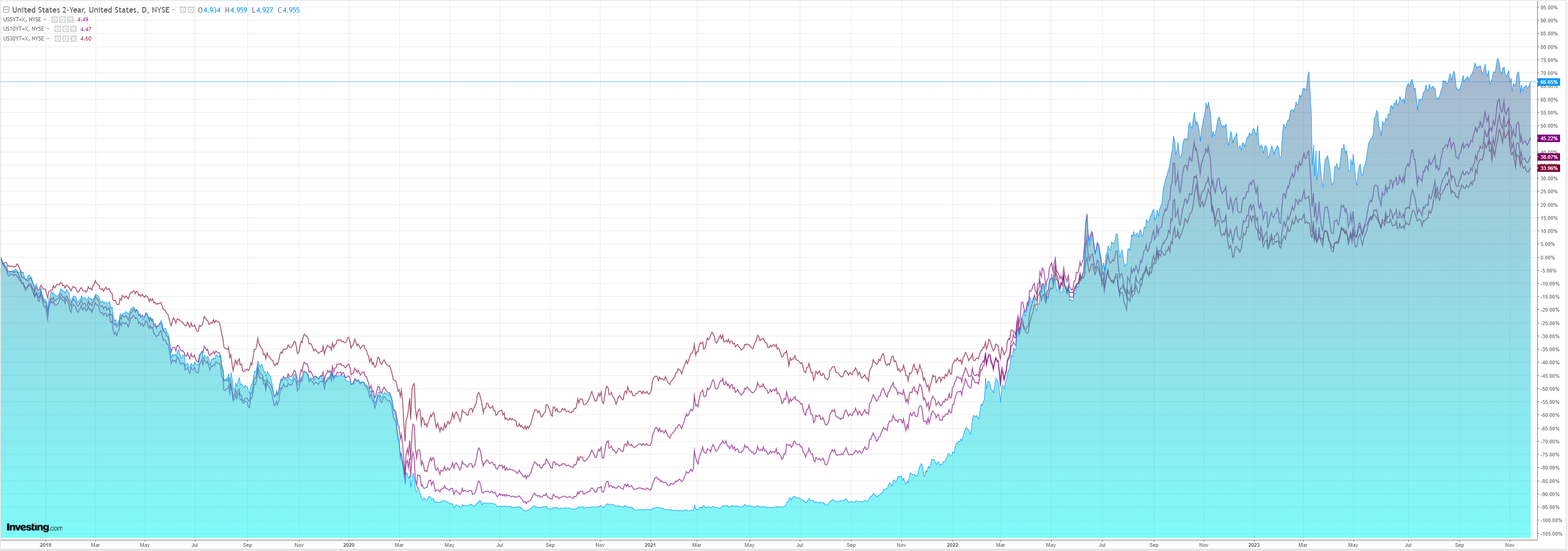

As yields popped:

Stocks meh:

Nothing is going anywhere unless or until Treasury yields fall further, taking DXY.

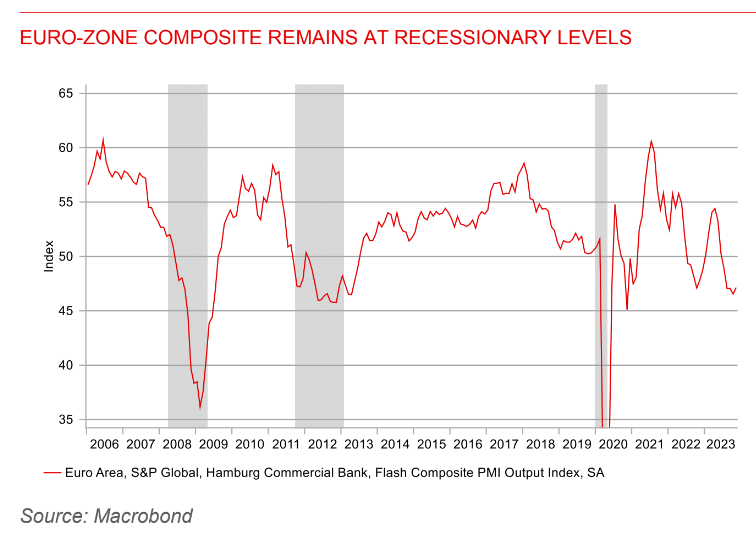

The problem is even a sowing US economy is still better that Europe where recession stalks. MUFG:

The US Thanksgiving holiday means the FX market moves were relatively modest yesterday and with the UST bond market closed there was a lack of direction.

The UKGilt market is where we saw the biggest move with the fallout from the AutumnStatement extending into yesterday and helped by the PMI data which advanced more than expected–the Composite Index crept above the 50-level (50.1) for the first time since July.

The UK 10-year breakeven rate jumped 3bps explaining some of the Gilt10yr yield move as the National Insurance Contribution cut was larger than expected and the benefits payments inflation adjustment was also the larger of the two options thought to have been considered (6.7% vs 4.6%) while the government maintained its pension striple-lock commitment with an increased pension payment of over 8.0% and the national living wage was increased by over 10%.

Over the near-term investors fear it may change the dial on another BoE rate hike. The jump in German government bond yields yesterday was much more muted and for good reason.The PMI data in Germany and in the euro-zone did improve but the improvements were pretty modest underlining the still weak with the euro-zone readings for manufacturing and services well below UK levels and still in contraction territory.

The news from Germany that it plans to suspend its constitutional debt brake for a fourth consecutive year to us underlines the lack of fiscal space Germany will have going forward and reinforces the downside risks to growth.

Suspending the debt brake was forced upon the government by the Constitutional Court decision on bringing back on balance sheet certain expenditures that were not included.

Certain expenditure projects related to say for example greening the German economy may now be shelved which would have a negative impact on growth going forward.

A signal of the changing balance of macro risks was underlined by the release of the ECB minutes which look to us to indicate a stronger prospect of rate cuts possibly coming sooner than expected.

The comments in the minutes on inflation were positive with the minutes noting that the “‘Persistent & Common Component of Inflation’ was now close to 2%”.

The minutes also continued to acknowledge that “most of the impact” from the monetary tightening had yet to materialise.

Still, there was also a desire to stress the continued need to keep rates “at sufficiently restrictive levels for as long necessary” which could imply risks of the ECB being slow to respond to worsening economic conditions that could materialise sooner.

We have been keen to stress that while the window for dollar appreciation back to the highs set in October and/or beyond may now have closed, the growth outlook in the euro-zone does not point to much upside scope for EUR/USD either.

Likewise, China has crossed the event horizon of a property black hole that will take decades to close. This si will require endless easing.

DXY can only fall so far when the global economy is such an unattractive place to be.

AUD follows wherever EUR and CNY go.