Goldman with the note.

CNY: Peace Dividend.

The Dollar downdraft post the low US CPI print and less rate pressure last week was somewhat further extended this week by a series of stronger CNY fixes.

After drawing a line in the sand (at around 7.18) for nearly three months when market pressures pushed towards a weaker Renminbi, this move stronger at the first hint of a weaker Dollar is further evidence of the policy preference for reducing depreciation expectations and outflow pressures.

Currency strength has also been bolstered by a constructive summit meeting between Presidents Biden and Xi, which attempted to put some guardrails on the relationship in order to limit geopolitical tail risks (especially related to cross-strait tensions), as well as media reports of additional policy support in the property market.

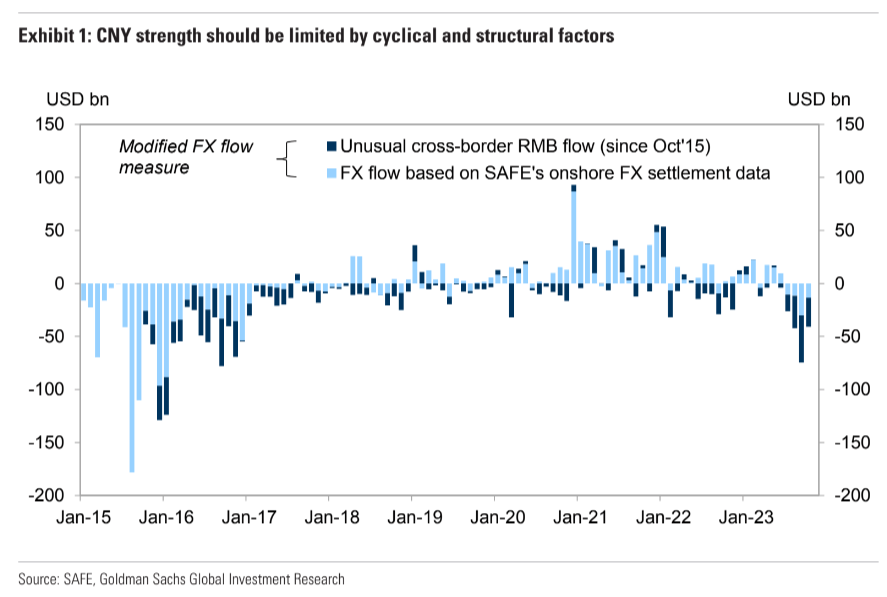

But a more sustained appreciation in the currency would require a more convincing pickup in Chinese growth and improved prospects of asset market outperformance, which still seems harder to envisage (Exhibit 1).

October activity data was mixed, retail sales beat expectations while fixed asset investment missed.

House priced at a suggest the weighted average property price in the primary market fell in October, and the headline CPI inflation also fell to negative territory again in October.

So even as policy-driven daily fixes may attempt to direct the currency somewhat stronger from here, and shake-out anyaccumulated short positioning, there will eventually be limits given our view of strong activity growth in the US in contrast to a more tepid profile in China, and a continued interest rate differential.

It is not China’s choice to slow the CNY depreciation. It is a necessity as the impossible trinity breaks around the property black hole. If it allows capital outflow to accelerate, its banks will go under as well.

But, a lower CNY is the only lever China has left to grow so do not expect the strength to last.

Ditto AUD.