DXY resumed its crash Friday night:

AUD is lagging but still ready to go higher:

Even the peg is up:

Oil recovered some poise:

Dirt firmed:

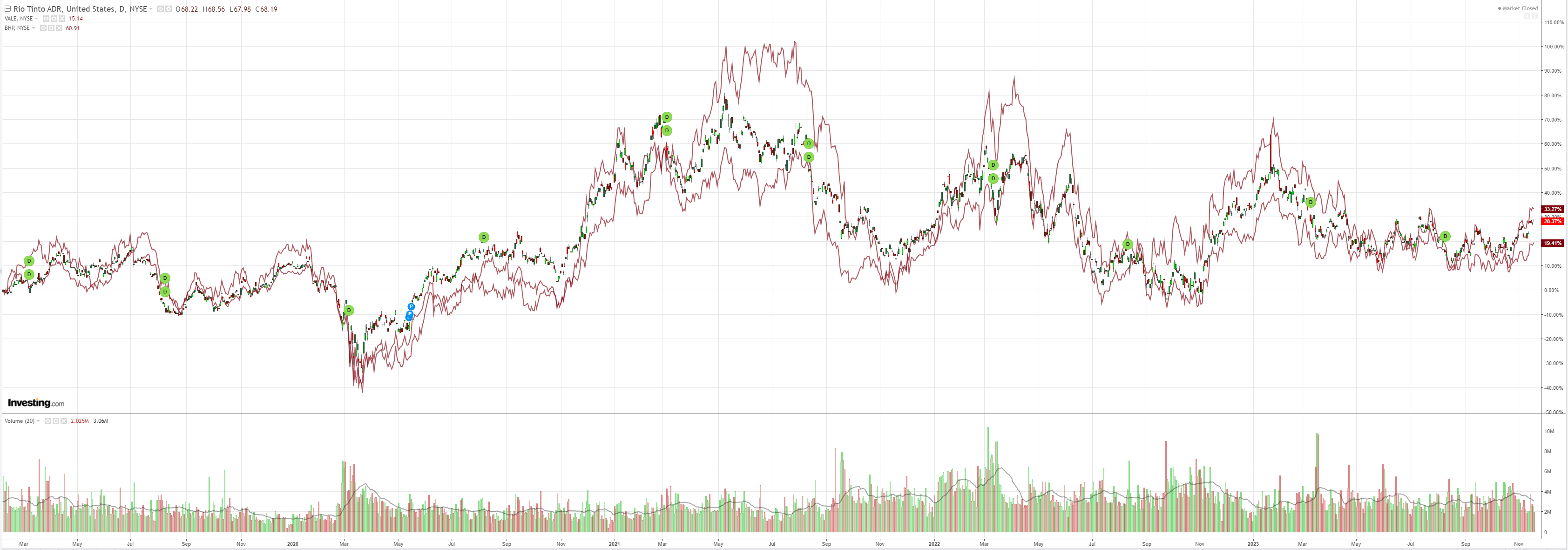

Miners meh:

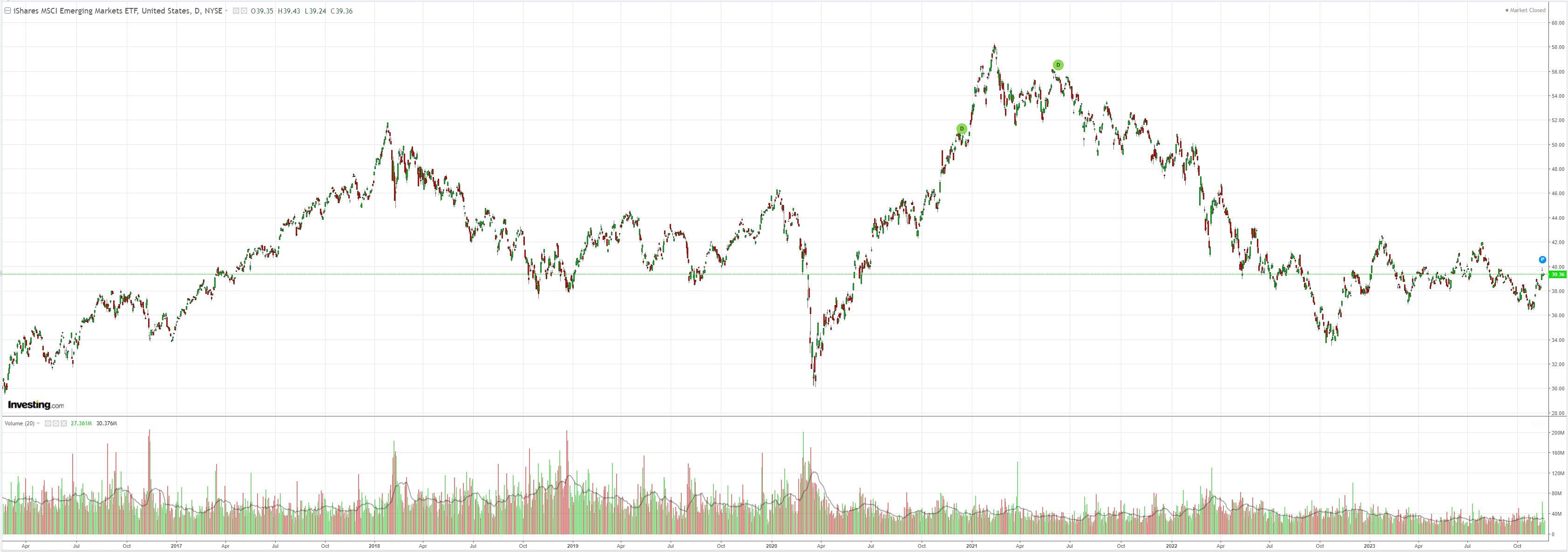

EM meh:

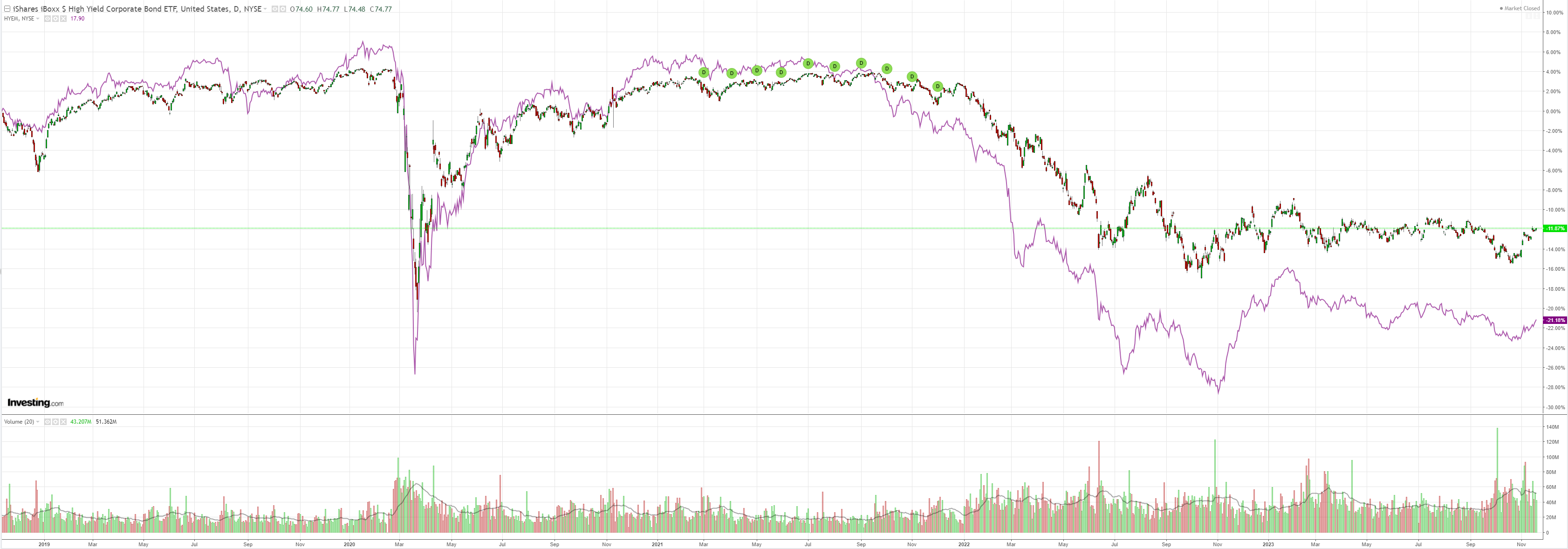

Junk is showing some promise:

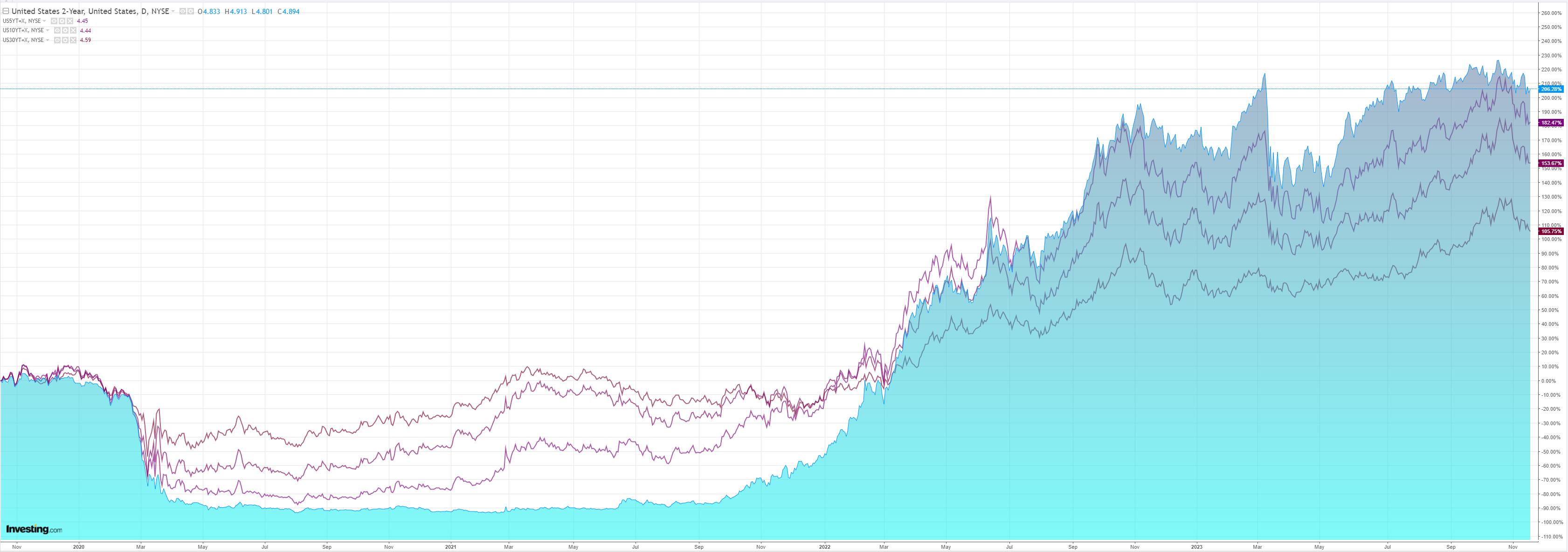

AS yields hit new lows:

Stocks are stuck:

Goldman has more.

USD: Sharp or Shallow redux.

The reaction to this week’s combination of softer US inflation data and some signs of slower consumer spending is reminiscent of the price action following the first lower inflation print over the summer.

That first weaker inflation report helped the market relax after a string of upside surprises, and this one should similarly calm fears that seasonal distortions might create unflattering optics into the December FOMC.

The substantial FX market reaction is understandable because this helps truncate the upside risk in yields and opens the possibility of earlier, non-recessionary rate cuts in the US, which is the key downside risk to our “stronger for longer” Dollar outlook.

Evidence that the US economy does not require this level of restriction would provide welcome relief to the rest of the world, where the pass-through from higher yields has been more challenging.

And FCI shifts led by data should add some durability to the rhetoric-based easing following the last FOMC meeting.

That said, for FX in particular, we still think it will be hard to erode much more of the Dollar’s appeal at this stage.

First, while the data are encouraging, it is not obvious that the outlook has swung so far towards earlier cuts.

Inflation is still at or above target on a sequential basis, and our GDP tracking has gone up, not down, following the data this week.

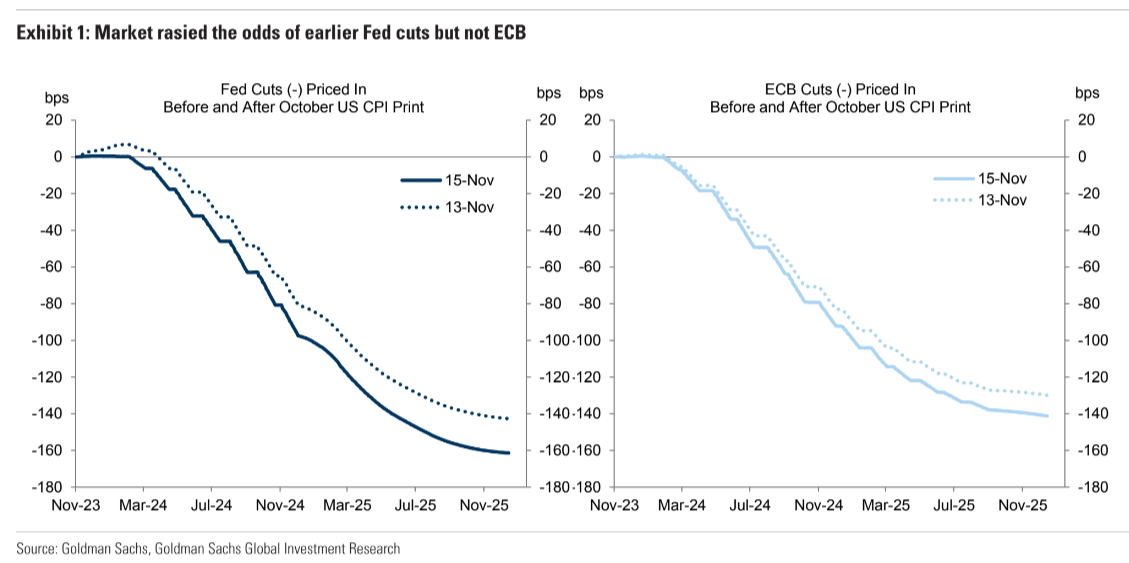

Second, we still believe that relative return prospects in the Dollar “challengers” are not particularly appealing, and still find it difficult to be more constructive after the substantial market reaction this week and front-end G10 yields mostly moving together in an environment where cyclical trajectories are still quite different (Exhibit 1).

Our 2024 Outlook calls for trend-like US growth, elevated US real rates, and a slow recovery in Europe and China—both with the aid of some policy support. That baseline is most consistent with relatively constrained FX volatility and only a gradual, bumpy decline in the US Dollar.

I am more bearish on US, European and Chinese growth but agree with the relativity argument.

AUD to grind higher not roar.