DXY was smashed last night:

AUD launched:

Even the peg moved a bit:

Gold up, oil down:

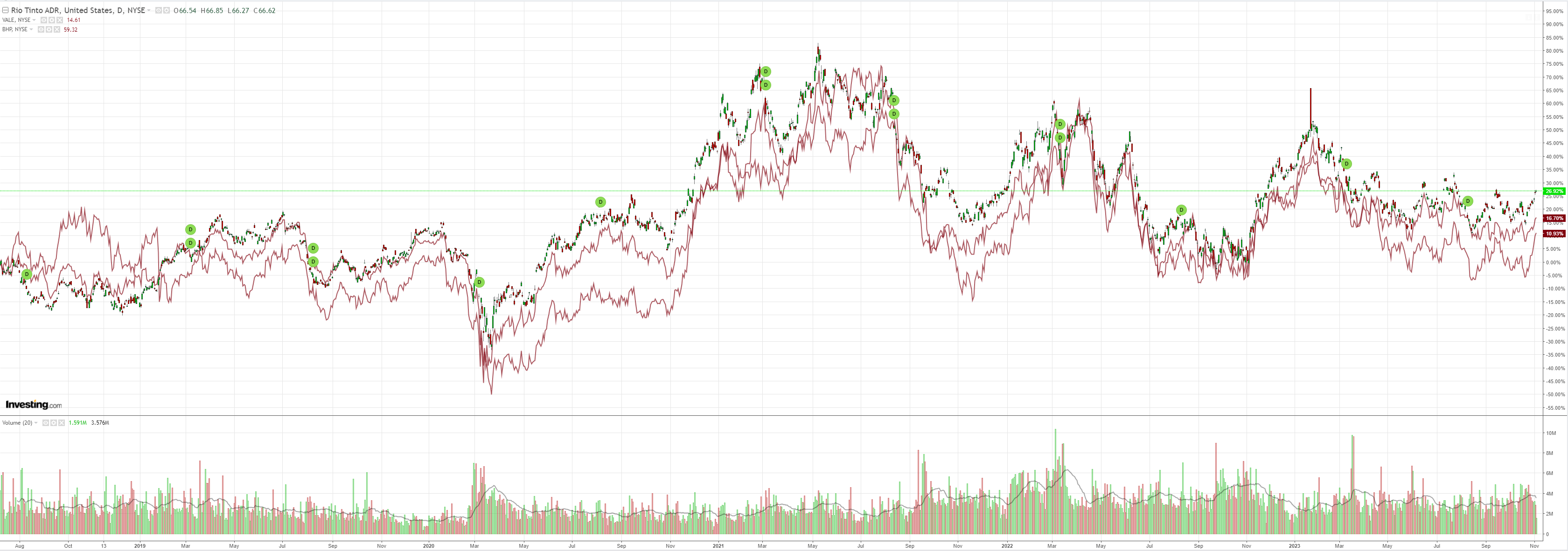

Dirt firmed:

Miners did OK:

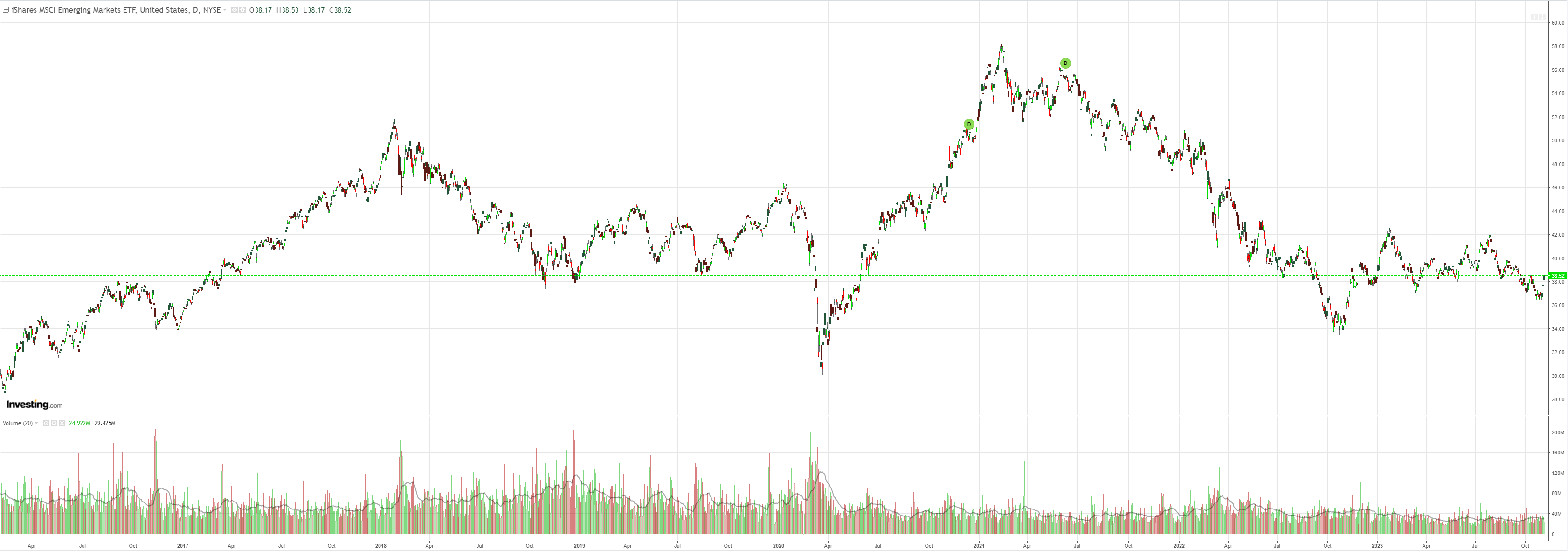

EM is back from the dead:

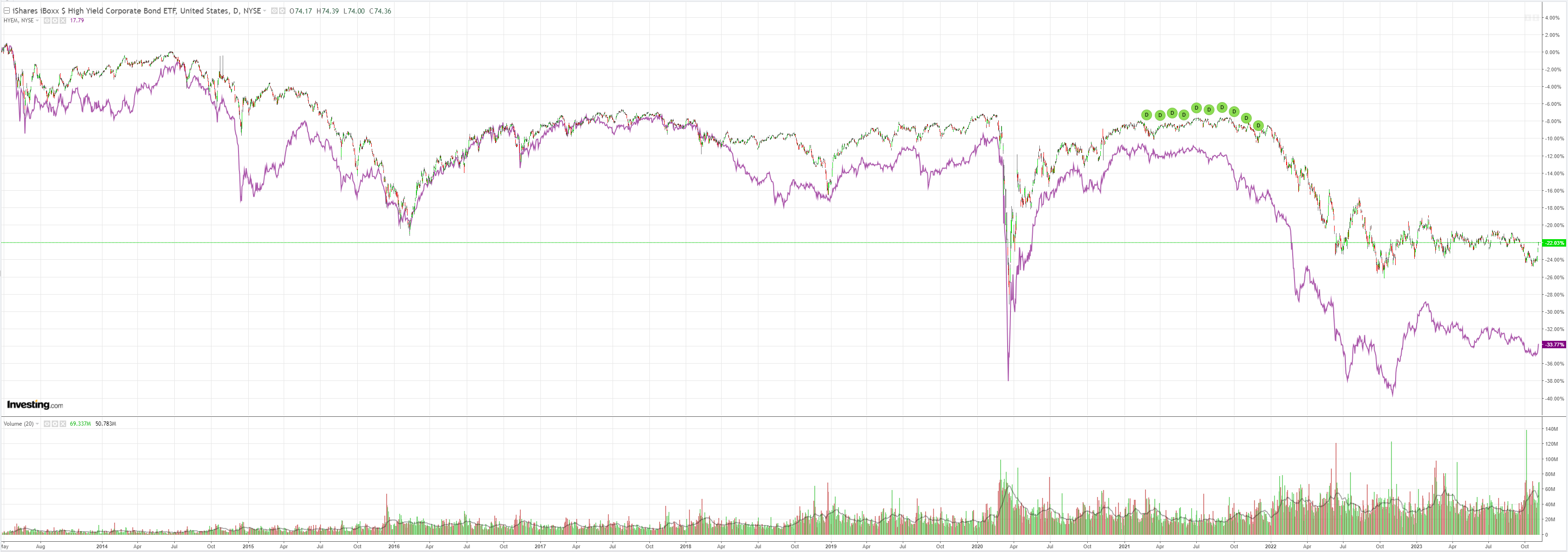

Junk joined in:

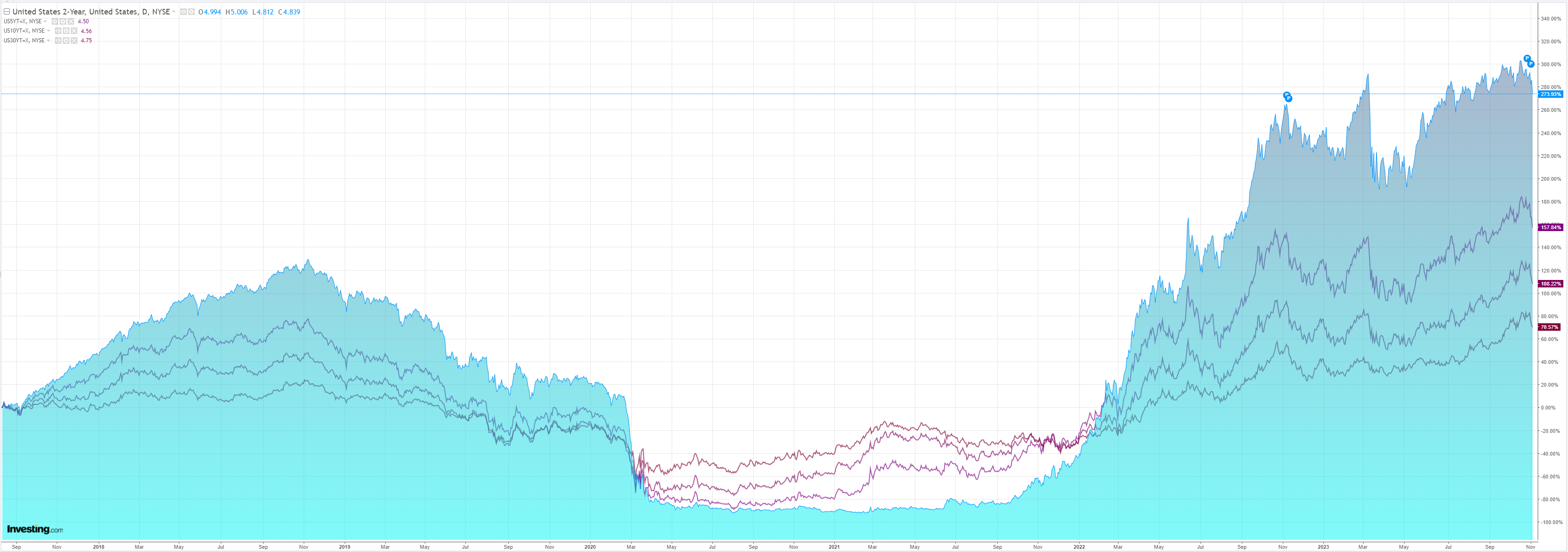

As yields fell off the proverbial:

Stocks roared:

The US landing is here, soft or hard. Goldman:

Nonfarm payrolls rose 150k in October—or 180k excluding the temporary drag from striking auto workers—missing consensus by 30k and lowering the three-month average to +204k from +266k as previously reported (following -101k of downward revisions to prior months). Healthcare (+89k) and government (+51k) payrolls drove the majority of hiring in the month, and indeed the breadth of job gains was the weakest since the 2020 lockdowns (payrolls diffusion index 52.0% compared to 61.4% in September and 58.4% in the first three quarters of the year).

The household survey was weak. The unemployment rate increased by 0.1pp to 3.9%, reflecting a 348k decline in household employment partially offset by a 201k decline in the labor force (labor force participation rate decreased by 0.1pp to 62.7%).

Average hourly earnings increased by 0.21% in October (mom sa), below consensus expectations. The September pace was revised up by 0.12pp to 0.33%.

The year-over-year rate declined by 0.2pp to +4.1% (vs. consensus 4.0%), and the 3-month annualized rate declined by 0.8pp to +3.2%.

Wages for production and non-supervisory workers increased 0.34% mom, or +4.4% from a year ago.

Average weekly hours and average overtime hours both declined by 0.1 to 34.3 and 2.9, respectively.

The October employment report indicated slowing job growth and additional progress on labor market rebalancing, further validating the FOMC’s dovish tilt at the November meeting. We continue to believe that the hiking cycle is done.

The ISM services index decreased by 1.8pt to 51.8 in October, below expectations for a smaller decrease.

The underlying composition was mixed, as the new orders (+3.7ptto 55.5) component increased while the business activity (-4.7pt to 54.1) and employment (-3.2pt to 50.2) components both decreased.

The supplier deliveries component decreased by 2.9pt to 47.5 (nsa) and the new export orders index dropped 14.9pt to 48.8 (nsa). The prices paid measure ticked down by 0.3pt to 58.6 (sa).

Markets are not standing on ceremony waiting to see if it is a soft landing or hard. They are bid big which increases the prospects of soft landing as wealth effects add to the case.

That credit has joined the rally is very bullish. But I would like to see junk form a more convincing bottom before signalling the all-clear. US inflation is still not convincingly headed to 2%.

AUD is a rocket ship in this environment. If the RBA hikes next week, the odds favour the bottom being in.