Below is an extract of a note on the October CoreLogic dwelling value results by Gareth Aird, head of Australian economics at CBA:

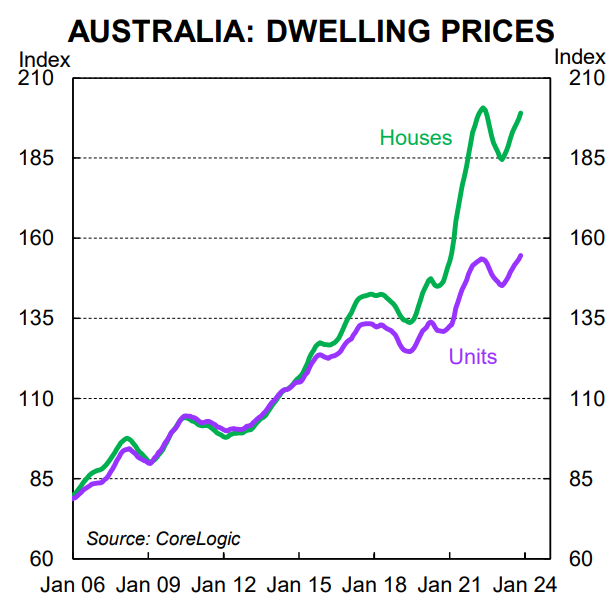

According to CoreLogic, Australian property prices rose for a ninth consecutive month in October.

The 0.9% increase in the 8 capital city benchmark index over the month followed similar increases over the previous three months.

The turnaround in property prices since February has been quite remarkable.

Indeed, the lift in housing values occurred in the midst of the RBA’s tightening cycle (recall that the RBA increased the cash rate by 25bp in February, March, May and June 2023).

The RBA’s 400bp of tightening since May 2022 has reduced home borrower capacity by ~30%. But property prices are now back to their previous peak (reached in April 2022 – on the eve of the commencement of the RBA’s tightening cycle).

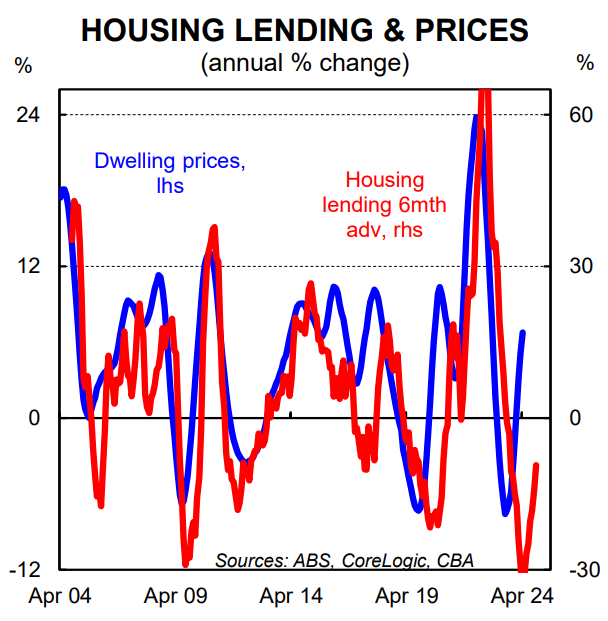

Housing affordability has declined significantly. The usual relationship between new lending and home prices has broken down (see below chart).

Housing loan commitments have fallen by around 30% since May 2022. A decline of this magnitude would ordinarily be expected to be accompanied by an ongoing decline in home prices. But these are extraordinary times.

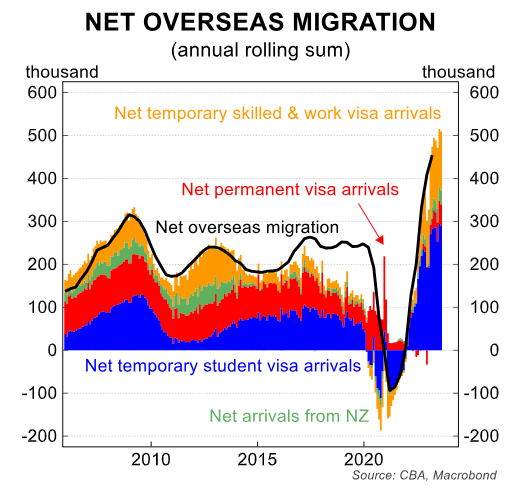

Australia’s population growth has surged over the past year. And home building has not kept pace.

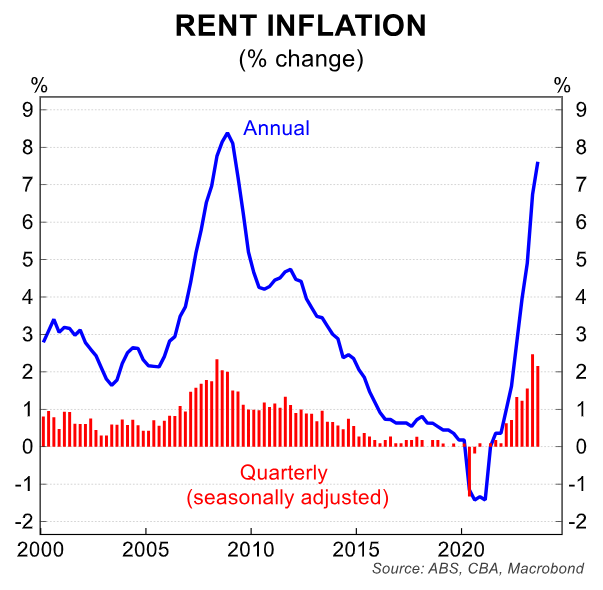

As a result, vacancy rates have dropped to record lows in most capital cities and the rental market is hot. This has put upward pressure on home prices.

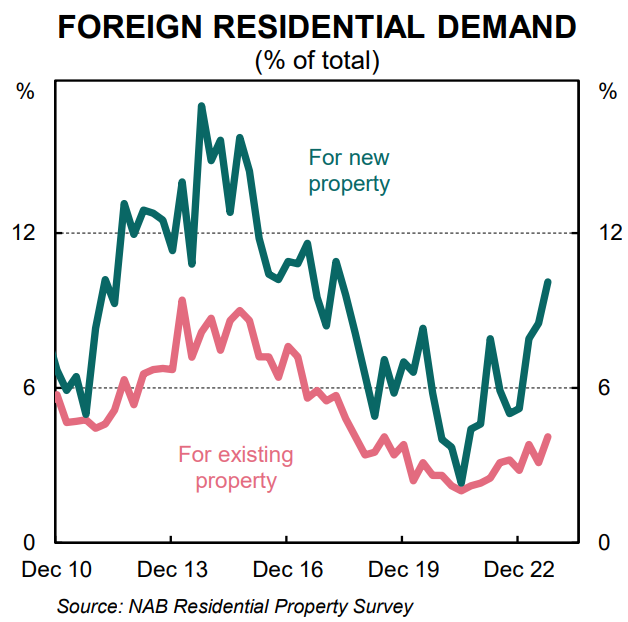

Foreign buyers are also more active in the market. According to the latest NAB residential property survey the share of total market sales to foreign buyers in new housing markets increased for the fourth straight quarter.

New sales to foreign buyers hit a 5½-year high of 10.1% in Q3 23.

Put simply there is a supply/demand imbalance in the housing market. Potential entrants into the housing market and renters feel the impact of this mismatch most acutely.

Meanwhile, many home borrowers with a mortgage are also feeling the pain of significantly higher mortgage rates.

We expect a 25bp rate increase at the November RBA Board meeting, which would take the cash rate to 4.35%.

A Cup Day rate increase may weigh on near term sentiment in the housing market. But overall we expect the underlying demand for housing to remain firm against a backdrop of constrained supply and strong rental growth.

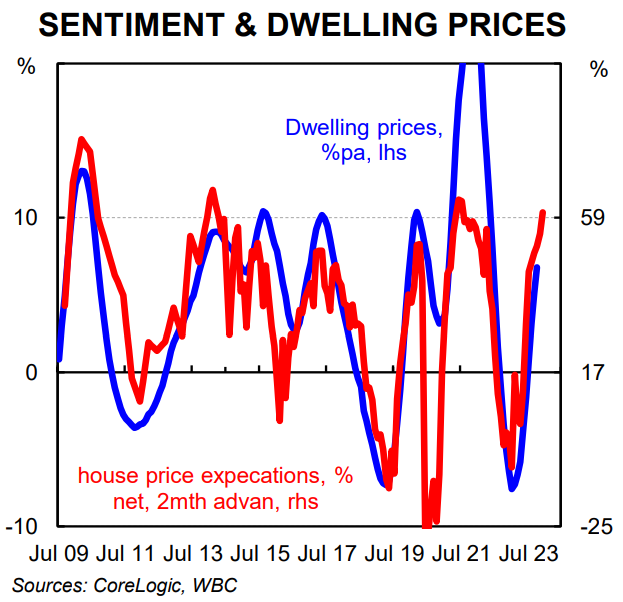

Here we note that households on average expect home prices to continue to lift. The Westpac MI house price expectations index from their monthly consumer sentiment survey rose a further 3.8% to 160.4 in October.

The index printed at another new cycle high in the month. The WBC/MI home price expectations index has historically had a close leading relationship with price outcomes.

On the supply side CoreLogic notes the flow of new capital city listings has picked up through winter and spring to be almost 12% higher than a year ago.

But total listings (ie new listings plus re-listings) remain lower than this time last year and below the previous five-year average.

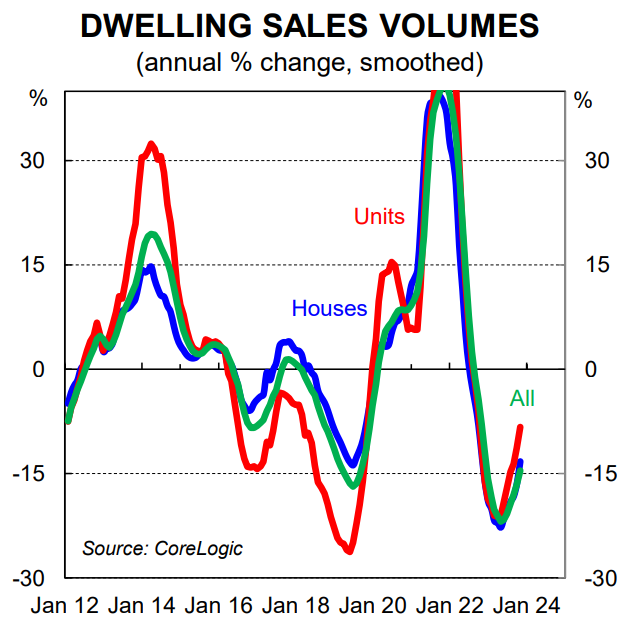

The upshot is that home sales are tracking only slightly above the five year average. By extension home buyer activity is not expected to be a tailwind on consumer spending.

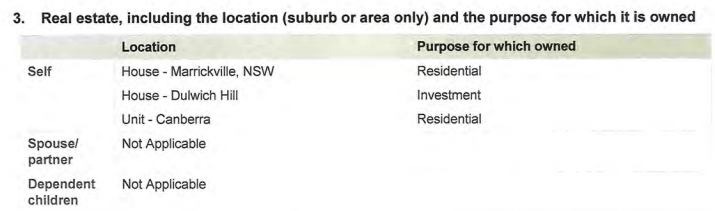

I will add that Prime Minister Anthony Albanese, like most politicians, has an extensive property portfolio:

Prime Minister Anthony Albanese’s real estate holdings (Source: APH).

Therefore, Albo’s record immigration program is enriching himself and his parliamentary colleagues by pumping up both values and rental returns.

Always back self-interest…