Australia’s economy seems to be headed for a period of stagflation, characterised by soft growth and stubbornly high inflation.

In the below note, CBA’s head of Australian economics, Gareth Aird, explains that forward-looking indicators are pointing to a slowdown in growth at the same time as inflationary pressures remain elevated, risking further monetary tightening next year.

In a quiet week we look at some timely second tier data:

The domestic economic data was particularly light this week. Indeed there was no ‘tier one’ releases. But the Judo Bank November ‘flash’ PMIs were published and the output data was sobering.

The PMIs in Australia tend to fly under the radar as the data has only been published since 2016. But the Judo Bank Purchasing Managers’ Index (PMIs) are part of the S&P Global PMIs and the survey methodology is sound.

The Global PMI series have been around a long time. They are closely-watched offshore and can be market-moving economic indicators in other jurisdictions.

They cover more than 30 advanced and emerging economies worldwide and provide one of the more timely indicators of the pulse of activity in the private sector. A host of offshore PMIs were released overnight.

In a week of little activity data in Australia we take a closer look at the domestic PMIs today given the recent reads have been particularly soft.

Output contracts, again:

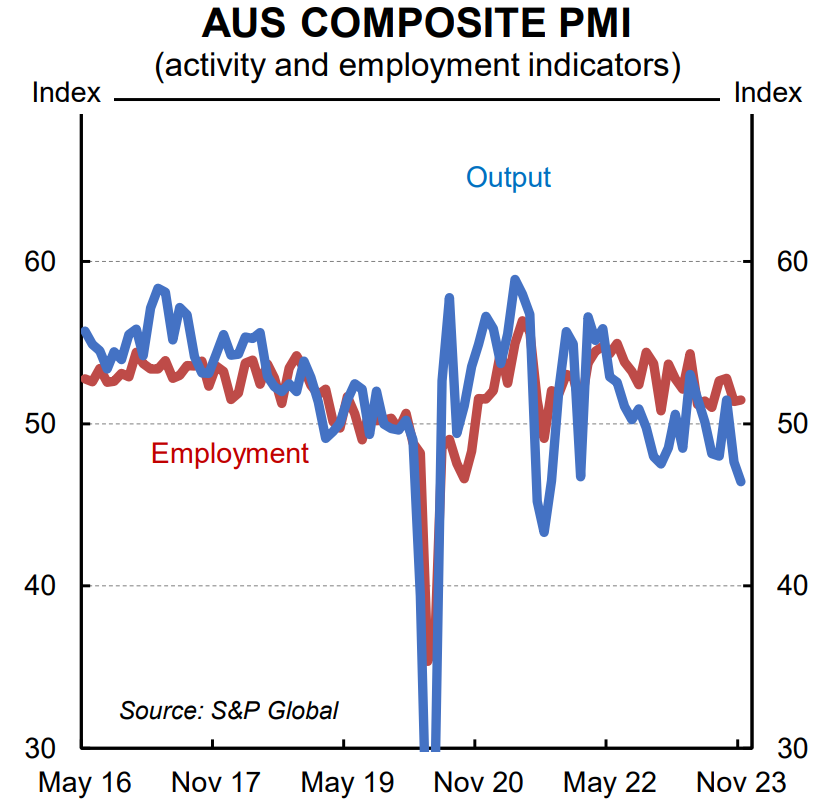

The Judo Flash Australia Composite PMI printed at 46.4 in November. In October the index sat at 47.6. Both of these outcomes are soft and indicate a contraction in business activity over October and November.

For context, the domestic PMIs averaged 49.21 in Q3 23 and 51.6 in Q2 23.

For readers unfamiliar with the PMIs we note that they are diffusion indices. A reading >50 indicating an overall increase compared to the previous month and <50 an overall decrease.

The Judo PMI report contained some colour on what has so far occurred in the December quarter.

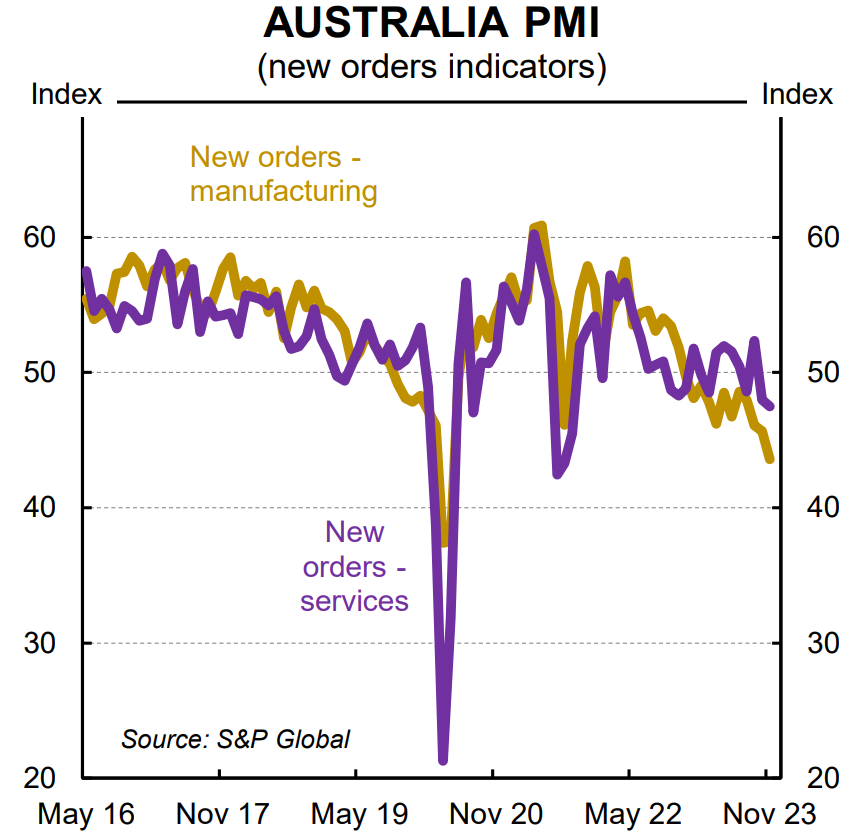

The report noted, “sharper new business downturns in both the manufacturing and service sectors led to the latest fall in output according to panellists. This was amidst widespread reports of softening economic conditions and high interest rates negatively affecting budgets.

“As a result, composite new orders slipped at the sharpest pace since September 2021…….”

“Australian private sector firms worked through their backlogs, leading to the quickest depletion of outstanding work since the initial pandemic period.”

Much has been made of the resilience of the Australian economy through an incredibly aggressive RBA tightening cycle. We can’t argue there. The labour market has remained tight and inflation has been elevated.

But there has been a clear softening in the recent spending data, albeit from lofty levels. Changes in unemployment and inflation lag shifts in consumption growth.

On Wednesday the RBA Governor noted that the recent increase in domestically generated inflation has stemmed from, “aggregate demand exceeding the economy’s potential to meet that demand”.

We don’t dispute that claim. But the statement is backward looking. At this juncture, we are most interested in how the balance of demand and supply is evolving.

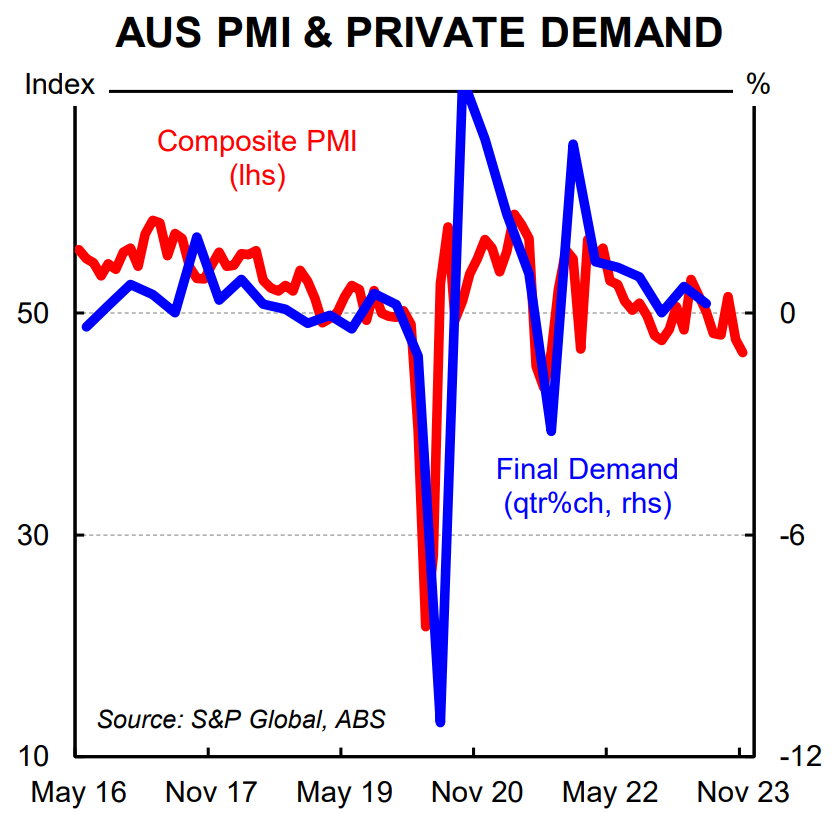

The PMIs suggest that in the December quarter demand growth in the private sector has stepped down at a more material pace than in the September quarter.

Our internal spending data for October supports this notion. It points to a contraction in spending over the month, after a more robust September quarter.

Our forecast for October retail trade based on our internal data, which prints next week (28/11), is -0.6%/mth.

The Judo PMIs don’t capture the retail sector. But the broad signal they are sending aligns with our data for overall consumption in October.

We are yet to see a cut of our spending data in November given the month is not yet over. But the Judo PMIs suggest the weakness we observed in October extended into November.

Indeed private demand could post a contraction over Q4 23 if the PMIs have accurately captured what has so far occurred.

It would likely take a decent uptick in activity in December for the private economy to expand in the December quarter.

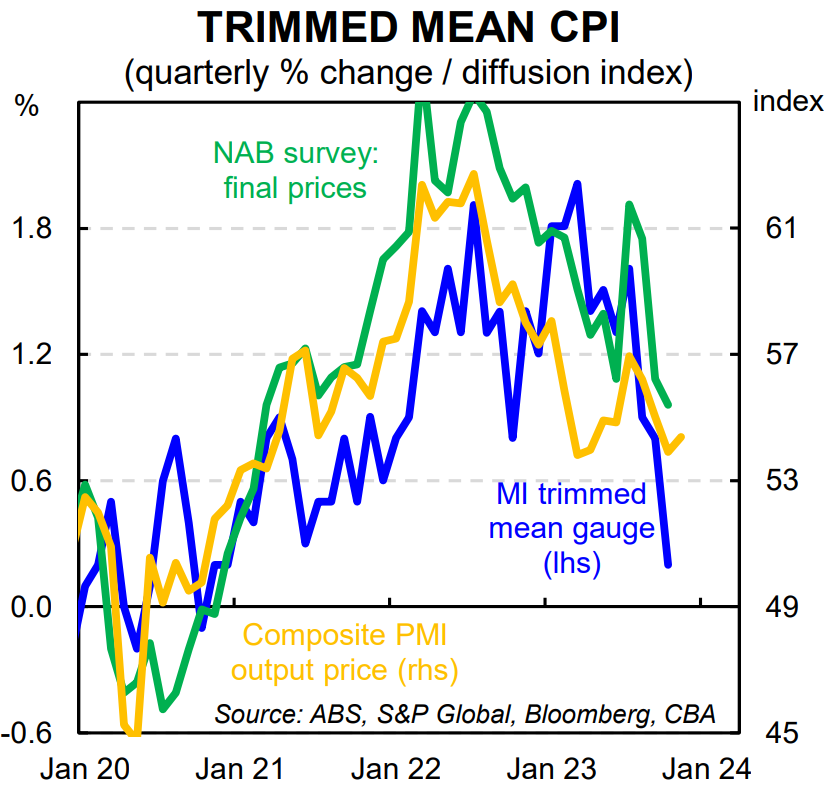

Prices growth still elevated, but has moderated:

As we noted earlier in the week, the already released private prices gauges for October are encouraging. They suggest the pace of inflation has stepped down in Q4 23.

My colleague Stephen Wu published our preview for the October monthly CPI indicator on Thursday.

We expect the official measure of inflation in the October monthly CPI indicator to print flat on the month, which would see the annual rate drop from 5.6% to 5.2%. This data is due for release on 29 November.

The Judo Flash PMI suggests inflationary pressures lifted a touch in November compared with October. The key output prices gauge lifted from 53.9 in October to 54.4 in November. But this is still well below the 56.1 level that the index averaged over Q3 23.

As such, we remain comfortable with our call that the Q4 23 trimmed mean CPI will not print above the RBA’s forecast of ~1.0%/qtr. This underpins our view that the cash rate is at its peak for this cycle.

The RBA’s assessment of the inflation risks mean that the Board is likely to have very little tolerance for an upside surprise in the Q4 23 CPI (due 31 January).

So while we don’t expect that upside surprise to materialise, markets are right to price the chance that policy is tightened again in February 2024.