As we know, Mad Albo and Chicken Chalmers have already delivered the worst real income shock in modern Australian history:

Thanks in large part to two major macro blunders.

The first was doing nothing to prevent energy cartels from gouging Australia during the Ukraine War, delivering the most significant utility bill shock in history.

The second was tearing down the border with India such that the nation lost control of mass immigration, delivering the most significant people inflows and rental shock in history.

These two immense blunders comprise what we call “Alboflation”.

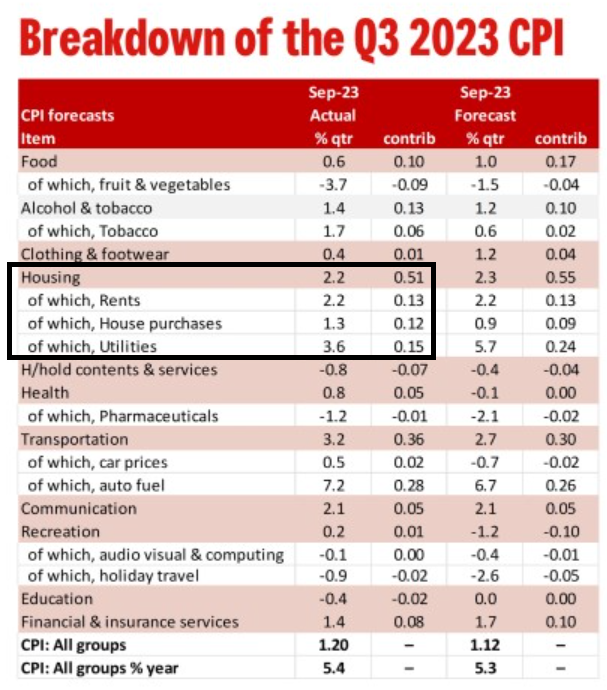

They now make up 43% of the CPI directly, and because energy is an input into everything, they also contribute to wider category inflation, notably in services:

Thus, it is fair to say that half the current inflation surge is directly attributable to Albanese Government mismanagement.

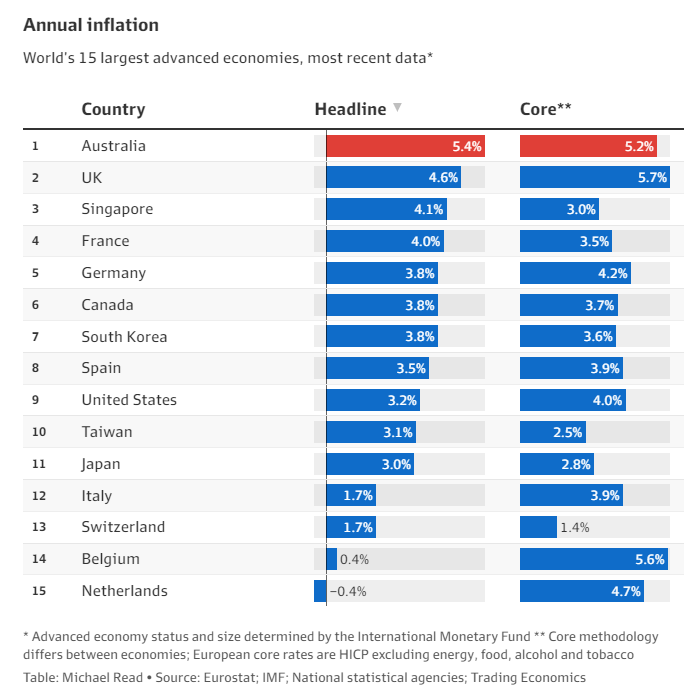

These are world-beating stuff-ups:

It takes spectacularly poor policymaking to outdo European inflation when it was the epicentre of the most significant energy shock in fifty years, and we have the cheapest energy resources in the world.

And consider, without Alboflation, Australian price rises would look more like the US. Instead of an interminable per capita recession, the central bank would be moving towards rate cuts and a new growth cycle.

What are the prospects of undoing the errors of Alboflation?

On the energy front, there is hope if it is a long way off. Albo’s failure to contain gas prices continues, but wholesale power prices have normalised.

The problem is that lower wholesale prices take multiple quarters to flow through to retail bills. We are still seeing the price hikes of 2022 flow through now.

The next major price reset via the AEMO’s default market offer is not until July 1, 2024. After that, utility bills will fall, but only if governments sustain the bill subsidies, which currently prevent an even worse outcome.

On mass immigration and housing price pressures, there is no relief in sight. Mad Albo and Chicken Chalmers haven’t even recognised their mistake.

When they do, they will discover that they cannot cut the flow of people from India even if they want to. At least not without trashing their labour market and migration deals with the Modi Government.

Worse, the scandal that has engulfed Indian immigration into Canada will boost Australian flows even more.

An unprecedented 600k migrants this year could rise even more in 2024.

The debacle is complete when one considers that interest rate hikes triggered by Alboflation suppress any supply-side response in property markets.

Only a screwball government could twist the economy so that monetary policy tightening becomes pro-cyclical.

Australian inflation is the highest in the world owing to the self-evident failings of Alboflation, but the government does not appear cognisant of it.

Ergo, there is no interest rate relief in sight for Aussie households.