The AFR has finally caught on to the fact that the Albanese government’s unprecedented immigration program is lifting inflation and means the RBA will need to keep interest rates higher for longer:

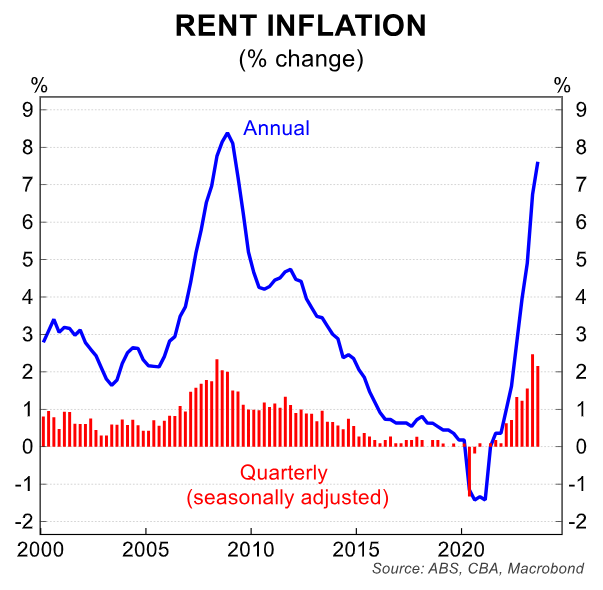

“Low housing starts are also feeding directly through to higher house prices (which the RBA worries will push up consumption via a wealth effect) and to surging rents, which are a key component of the services inflation that the RBA is particularly concerned about”.

“More and better government action could help to alleviate the inflationary pressures from housing. But instead, the federal government is exacerbating the problem by turbocharging immigration, which is currently running at an annualised rate of 500,000, and which HSBC chief economist Paul Bloxham has rightly described as a true shock to the Australian economy”.

“And federal and state governments are further crowding out housing investment – and putting upwards pressure on prices for labour and materials – by unleashing a wave of infrastructure spending at what is arguably the wrong time”.

Alan Kohler made similar arguments in the New Daily:

“The reason the RBA lifts interest rates is to reduce aggregate demand by increasing the debt repayments of borrowers and therefore reduce their demand”.

“How can the Reserve Bank be expected to slow demand when there are half a million more mouths to feed?”

“Or to be more accurate how can the pain and cutbacks by Australia’s borrowers be expected to slow the demand enough to bring down inflation when 152,200 more people showed up here in the three months to March?”

“Net overseas migration is running at an annual rate of more than 600,000. The annual growth rate from migration is 2.3%. With the 29,400 births in the March quarter, population growth represented an annual growth rate of 2.8%”.

“This is causing a massive shock, and changing everything about the economy producing a rebound in house prices, despite the huge increase in interest rates”.

“It is also leading to stronger than expected top-line economic growth, at the same time as a “per capita recession”: that is, GDP grew by 0.4% in the March and June quarters but on a per head basis it contracted by 0.3% in both”.

“GDP and aggregate demand would be falling if it wasn’t for 2.8% population growth, and interest rates would be on hold or even getting cut, not increased”.

The Albanese government’s unprecedented immigration has both state governments and the RBA caught between a rock and a hard place.

As noted by Infrastructure Partnerships Australia chief executive Adrian Dwyer this week, record population growth necessarily means that infrastructure needs to be built, otherwise congestion will increase and productivity will stall:

“You have to build the infrastructure for the economy you want, not the one you’ve got. The population growth is coming”, he said.

Meanwhile, the RBA is fighting against population-driven inflation, most notably in the rental market:

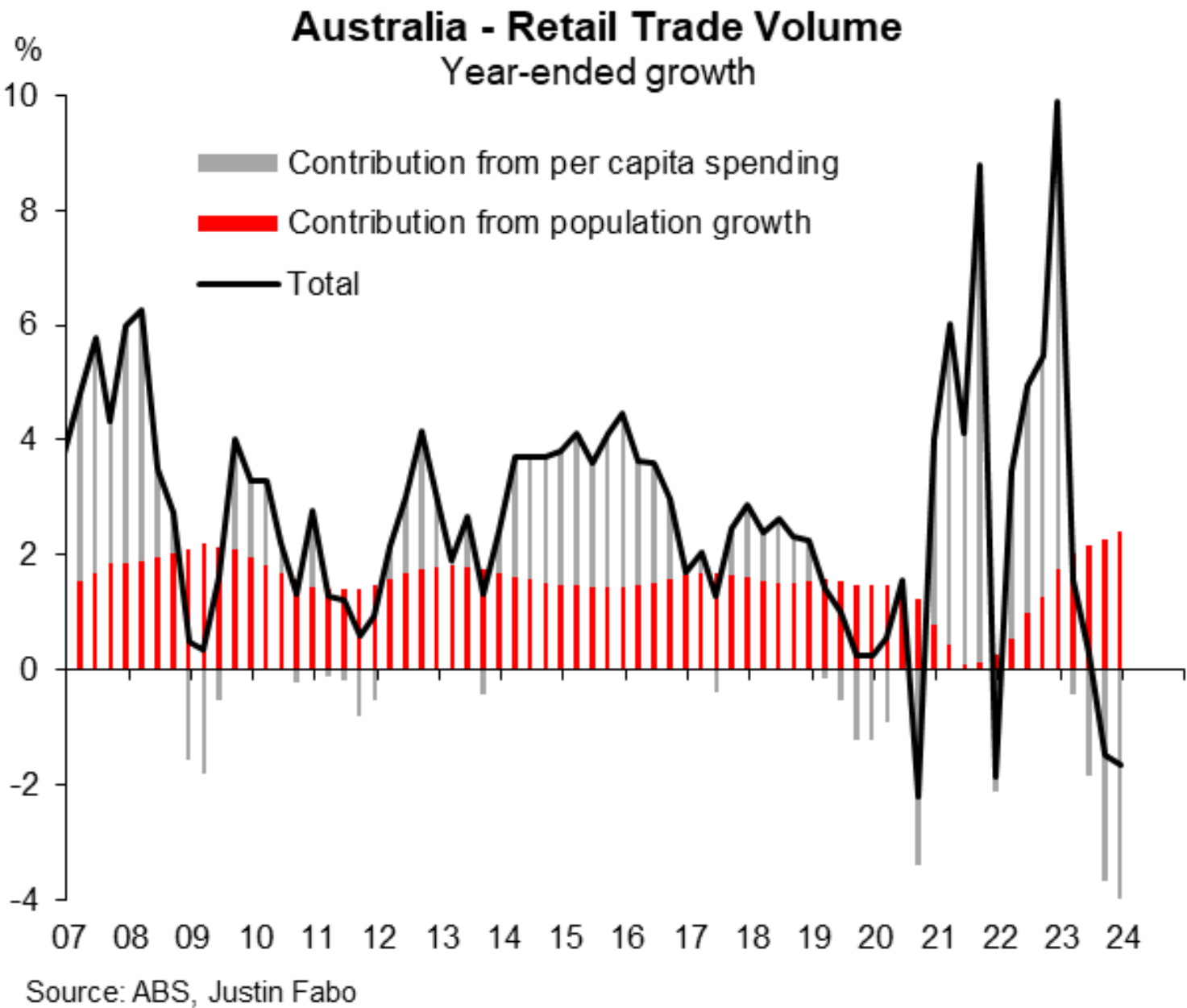

While the RBA’s aggressive rate hikes have worked to reduce spending across individual households, the rapid growth in the number of households amid record immigration means that overall household spending continues to rise.

This was highlighted by last week’s September quarter retail sales data from the ABS, which showed that sales volumes rose by 0.2% over the quarter in aggregate, but fell by around 0.4% when adjusted for population growth (annual chart shown below):

So basically, the RBA is engaged in a tug-of-war with the Albanese government’s record immigration program.

The RBA is desperately trying to slow the economy and inflation via rate hikes, while the Albanese government is juicing both by sheer population growth.

The end result is that the RBA will have to retaliate by lifting rates further, which will land directly on the one-third of Australians carrying mortgages.

The obvious solution is for the Albanese government to temper immigration flows to a level below the nation’s capacity to supply new housing and infrastructure, along with business investment.

This would take the steam out of inflation, lift productivity, and improve the lives of mortgage holders and renters.