Two pieces of data suggest that New Zealand households are struggling in the face of record (5.25%) interest rate hikes from the Reserve Bank.

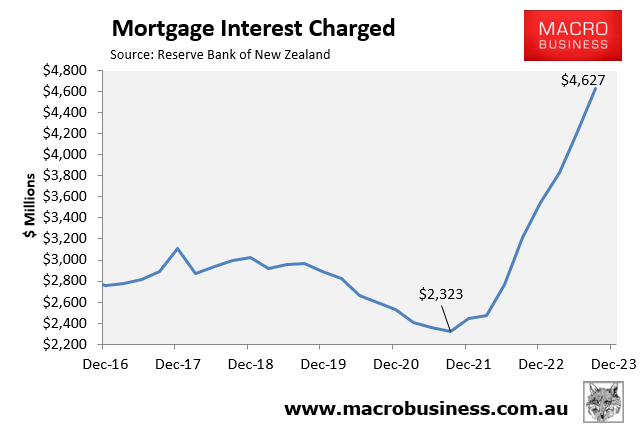

First, new quarterly data shows that the aggregate amount of mortgage interest paid by Kiwi households has doubled since the Reserve Bank began its interest rate hiking cycle in late 2021:

As you can see, aggregate mortgage interest charged fell to a low of $2,323 million in the September quarter of 2021, but had doubled to $4,627 million just two years later in September 2023.

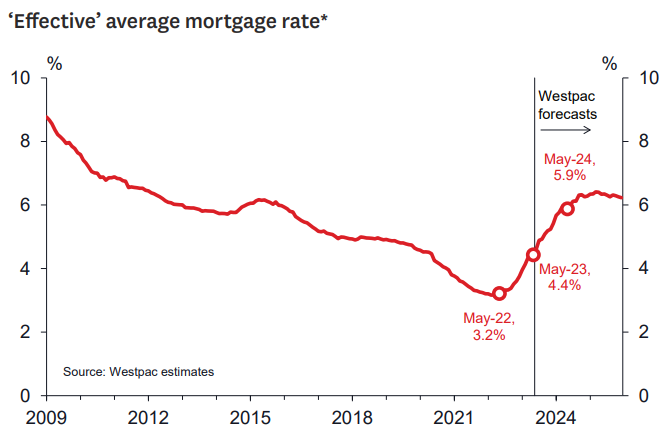

Moreover, the average interest charged will continue to rise into 2024 even if the Reserve Bank keeps the official cash rate on hold at 5.50%.

This is because there are still large numbers of Kiwi households on cheap pandemic fixed rate mortgages of whom will roll over to more expensive rates over the coming 12 months:

Therefore, there is significant monetary tightening ‘built in’ to New Zealand’s economy, which will continue to whack households with mortgages.

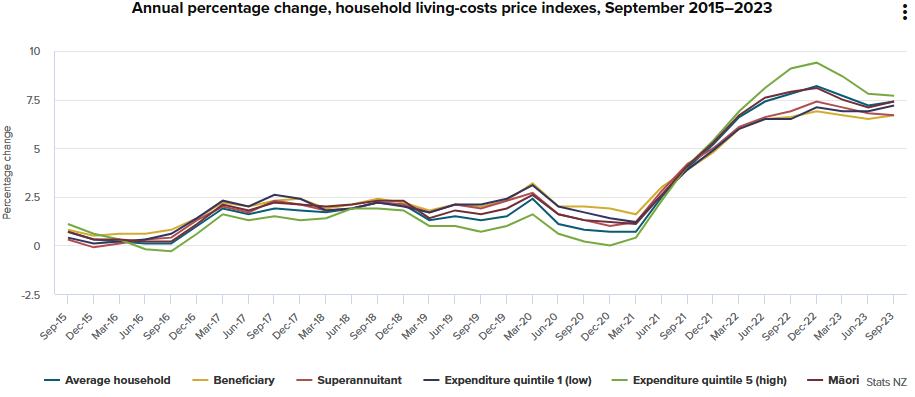

Second, Statistics New Zealand released its cost-of-living indices for the September quarter, which showed a reacceleration in living costs for the average Kiwi household:

Source: Statistics NZ

Living costs for the average household increased by 7.4% in the 12 months to the September 2023 quarter, up from the 7.2% annual increase recorded for the year ended 30 June 2023.

The rise in living costs comes despite falling CPI inflation, which moderated to an annual rate of 5.6% for the September quarter from 6.0% in the June quarter.

The key factor driving the divergence is that mortgage interest payments are not included in CPI inflation but are included in the measurement of household living costs.

Therefore, the 27.3% annual growth in mortgage interest payments added directly to household cost-of-living but not CPI inflation.