Westpac with the note.

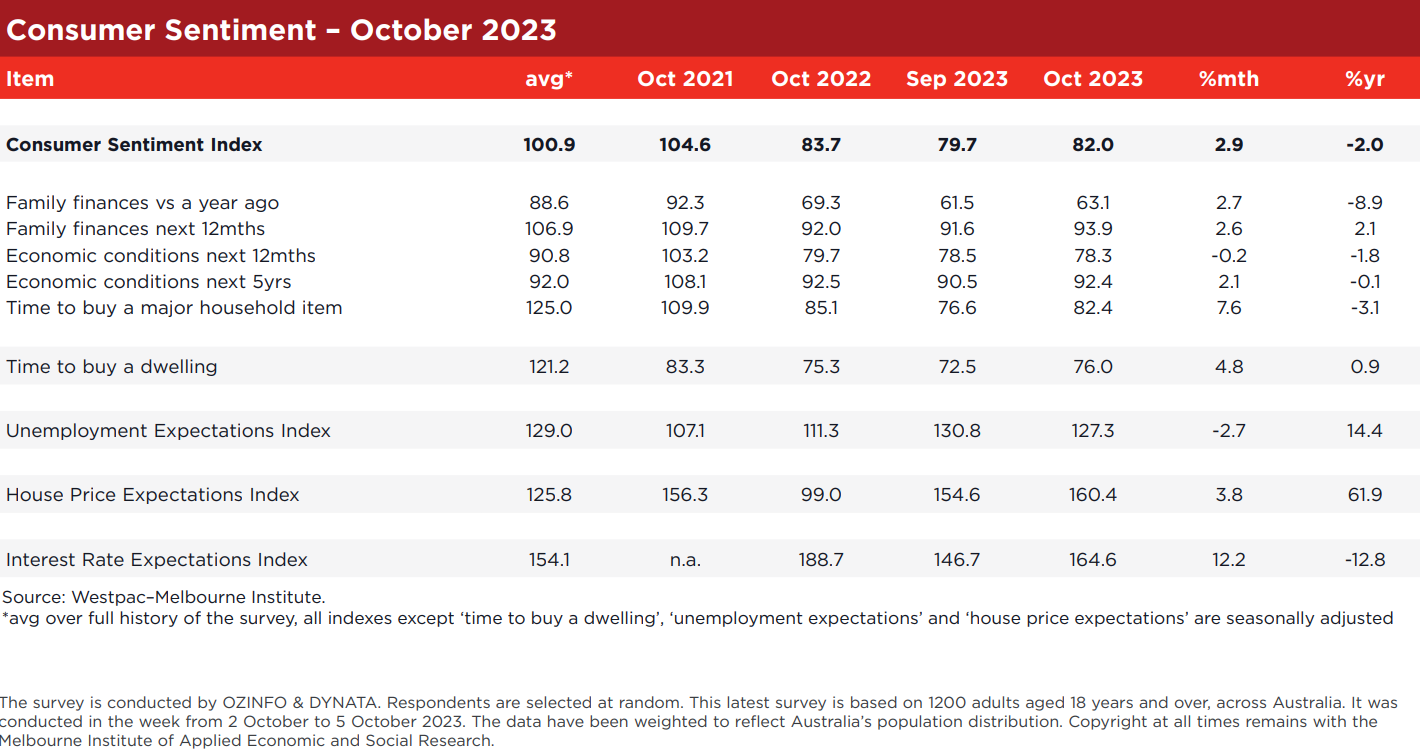

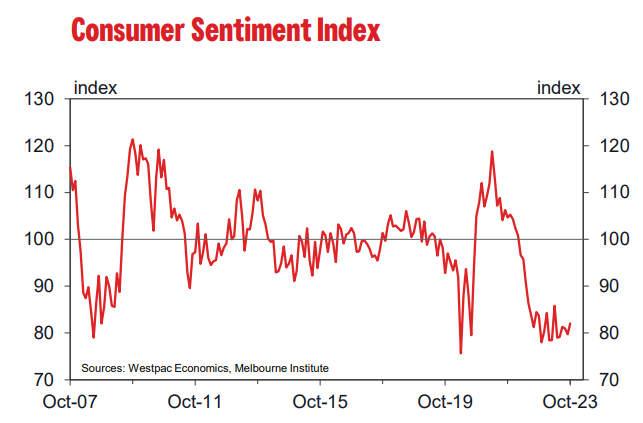

The Westpac-Melbourne Institute Index of Consumer Sentiment rose 2.9% to 82 in October, up from 79.7 in September.

The consumer mood has improved slightly but optimism remains in extremely short supply. At 82, the latest Index read is still in deeply pessimistic territory, consistent with a continuation of the contraction in per capita spending seen since late last year.

While there are some faint glimmers of hope around family finances and the outlook for jobs, these are being overshadowed by still high inflation and renewed rate rise concerns.

The RBA’s extended pause on rate hikes continues to see only a muted lift in sentiment. The headline Index is up only 3.7% since the last rate rise in June, and sentiment amongst households with a mortgage is only up 5.9%.

Consumers remain wary of the potential for more rises in the months ahead. Amongst those surveyed after the October RBA decision, 63% still expect mortgage interest rates to rise over the next year, up sharply from 48% in September (albeit below the 70-80% reads seen when the RBA was actively hiking).

Only 7% of consumers expect rates to be cut over the next year, down from 15% in September.

Some of the increase in this expectation likely relates to the surprise jump in the monthly CPI indicator, which showed annual inflation moving back above 5% in August.

However, the detailed survey responses point to a slightly more nuanced picture here. Across sub-groups, the latest increase in interest rate expectations has been driven by freehold homeowners and older households rather than households with a mortgage.

As such, it may be more about hopes of improved returns for the ‘deposit belt’ than fears of further rate hikes for the ‘mortgage belt’.

The component sub-indexes were again a mixed bag in the month, with family finances still clearly under intense pressure despite a marginal improvement, and no change in downbeat near-term expectations for the economy. Labour market conditions remain a notable source of support.

Assessments of ‘family finances’ showed improvements in line with the headline result but continue to point to intense cost-of-living pressures.

The sub-index tracking assessments of ‘finances vs a year ago’ – a particularly important indicator for spending activity – rose 2.7% in October but at 63.1 remains at extremely weak levels, below the levels seen mid-year.

The sub-group detail suggests some of the latest improvement may relate to recent increases in minimum wage and Award rates, inflation indexation adjustments to welfare rates, and improved interest returns for retirees.

The sub-index tracking expectations for ‘finances next 12 months’ is showing a more promising improvement, up 2.6% to 93.9 in the October month and up 11.8% since June.

The pause in the interest rate tightening cycle has seen a sharp improvement for households with a mortgage, with expectations up 20% since June. The improvement more broadly likely reflects an expectation that cost-of-living pressures will ease as we move into 2024.

Perhaps the most promising shift however is around assessments of ‘time to buy a major household item’. This sub-index surged 7.6% in October.

Buyer attitudes have been markedly weaker over the last year compared with previous economic cycles, and look to be capturing the direct effects of higher prices. If sustained, the lift may be signalling that the inflation situation for consumers is starting to improve.

However, that is a very big ‘if’. At 82.4, the sub-index is still at extreme lows (in the bottom 2.5% of observations since the survey began). We have also seen a few false starts, most notably the 9.5% rise in April that unwound in the months that followed.

Consumers remain less upbeat about near-term prospects for the economy. The ‘economic outlook, next 12 months’ sub-index dipped 0.2% to 78.3.

The medium-term view is less pessimistic though: the ‘economic outlook, next five years’ sub-index is up 2.1% to 92.4, in line with\ the long-run average of 92. This suggests consumers remain confident that the current cost of living problems will eventually be brought under control.

Labour markets also remain a source of support for consumers.

The Westpac-Melbourne Institute Unemployment Expectations Index declined 2.7% to 127.3 in October, dipping back below the long-run average of 129 (recall that lower index reads mean more consumers expect unemployment to fall in the year ahead).

The index has been chopping around a flat trend since June, suggesting labour market conditions have softened but that the unemployment rate is expected to hold flat rather than rise materially – a notable contrast to most economists’ forecasts.

On housing, we continue to see a mix of very weak consumer assessments of ‘time to buy’ and very bullish expectations for prices. Both measures improved a touch in October.

The ‘time to buy a dwelling’ index posted a 4.8% rise in October, but at 76 remains at extremely low levels by historical standards.

The Westpac Melbourne Institute House Price Expectations Index rose a further 3.8% to 160.4, hitting yet another new cycle high. Just under 70% of consumers now expect prices to rise over the next 12 months.

Notably, the state breakdown shows much stronger improvements in Queensland and Western Australia for both homebuyer sentiment (up 13.6% and 29% respectively) and price expectations (up 10.7% and 12.2% respectively). October saw the same measures broadly unchanged for NSW and Victoria.

The Reserve Bank Board next meets on November 7. It is set to be very revealing in terms of both how the Bank is reviewing the outlook – a revised set of RBA forecasts due to be released with the November Statement on Monetary Policy a few days later – and how its assessment of the balance of risks may be shifting.

Today’s release again highlights the main negative at play: intense pressures bearing down on the Australian consumer pointing to continued weak spending in the near term.

Against this is a more troubling inflation situation with surging fuel prices, a lower AUD and evidence of more persistent price rises in the services sector.

While the RBA may need to revise its near-term forecasts for headline inflation up, on its own this will probably not be enough to trigger a further rate rise.

If, however, there are further surprises in the September quarter CPI, due October 25, the next few meetings could be a little more live than the one in October.