By Gareth Aird and Stephen Wu at CBA

Key Points:

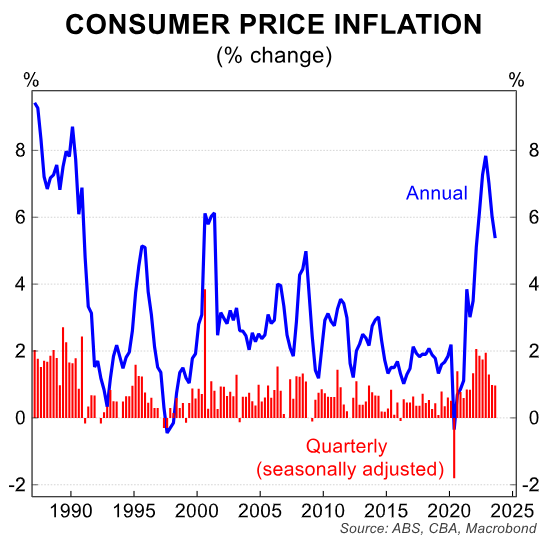

- The headline CPI rose by 1.2%/qtr in Q3 23 and the annual rate dipped to 5.4%.

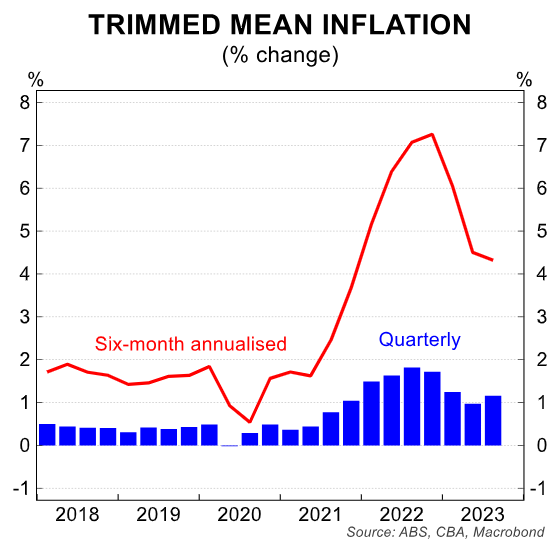

- The RBA’s preferred measure of underlying inflation, the trimmed mean, increased by a solid 1.2%/qtr and the annual rate stepped down to 5.2% (from 5.9% in Q2 23).

- We expect the RBA to act on their hiking bias and raise the cash rate by 25bp at the November Board meeting to 4.35%.

Headline and core inflation stronger than consensus and the RBA’s expectations:

Two weeks ago, we stated that the November Board meeting was ‘live’. And we ascribed a 40% chance to a rate increase on Melbourne Cup day.

At the time the market had priced a 20% chance of a rate hike in November. Our November ‘on hold’ call was underpinned by a 1.0%/qtr increase in the Q3 23 trimmed mean CPI.

The data on Wednesday printed stronger than our expectation (note we flagged the risk to our inflation forecast was to the upside).

The 1.2%/qtr lift in underlying inflation over the September quarter was also firmer than the market and RBA anticipated. The market median forecast for the Q3 23 trimmed mean CPI was 1.0%/qtr. And the RBA had forecast a 0.9%/qtr lift in the August Statement on Monetary Policy (SMP).

Headline inflation also came in a little stronger than the market and RBA anticipated. But it is the core read that will cause the RBA Board some anxiety.

The RBA has a hiking bias. And on Tuesday night, RBA Governor Bullock stated, “the Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation”.

We are not sure what constitutes a ‘material upward revision’ to the RBA’s inflation forecasts. But we consider the lift in underlying inflation over Q3 23 to be sufficiently strong for the RBA to act on their hiking bias at the upcoming Board meeting.

The RBA tends to place more weight on underlying rather than headline inflation. And their preferred measure of underlying inflation is the trimmed mean.

The annual rate of both headline and underlying inflation came down over Q3 23. But it is the quarterly pulse of underlying inflation that matters most at this juncture for monetary policy.

The 1.2%/qtr increase in trimmed mean inflation over Q3 23 was stronger than the upwardly revised 1.0%/qtr lift in Q2 23 (previously reported as 0.9%/qtr).

The six month annualised pace of core inflation is 4.3%. We believe that pace is sufficiently firm to cause the Board some discomfort given the RBA has recently upped its rhetoric on the importance of keeping inflation expectations anchored.

The RBA will publish an updated set of economic forecasts in the November SMP (to be released on 10/11). The Bank will upwardly revise their near term inflation profile based on today’s outcome.

But as we noted two weeks ago, we expect the RBA will retain its central scenario in the November SMP that inflation will return to the target band in late 2025.

This may seem an odd statement to make. But it’s always important to remember that policymakers can shape economic outcomes. The actions of the RBA influence their forecasts.

The RBA’s job is to use monetary policy to manage demand in the economy and by extension inflation. A November rate hike will enable the RBA to retain its central scenario for inflation to return to the target band by late 2025.

Of course, a rate hike in November is not guaranteed. And the Board may judge that keeping policy on hold for another month is the appropriate response while it gathers more information on the economy.

Of note will be the Q3 23 read on the Wage Price Index released on 15/11.However, we don’t judge it likely that the Board will wait another month before pulling the rate hike trigger.

We ascribe a 70% chance to a 25bp rate increase in November and a 30% chance to on hold.

Focus for RBA watchers quickly shifts to Governor Bullock’s appearance on Thursday before the Senate Economics Legislation Committee (Supplementary Budget Estimates) in Canberra. The Governor will be joined by Assistant Governor Christopher Kent.

The Governor will have the opportunity to opine on today’s CPI and the potential impacts for monetary policy.

That said, the Governor may wish to play a ‘straight bat’ and not pre-empt what the Board may decide at the November meeting.

See below for our full take on the September quarter CPI

The detail

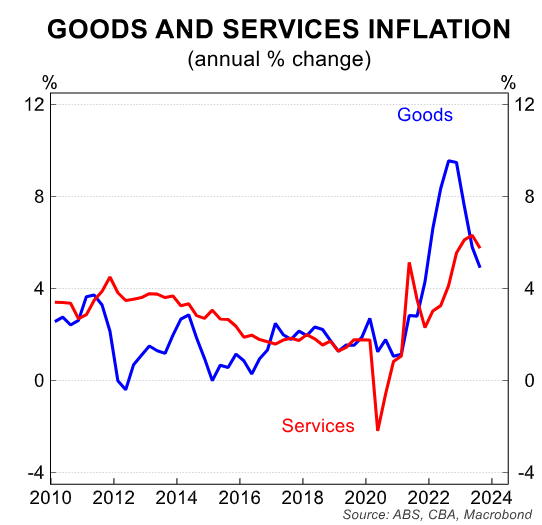

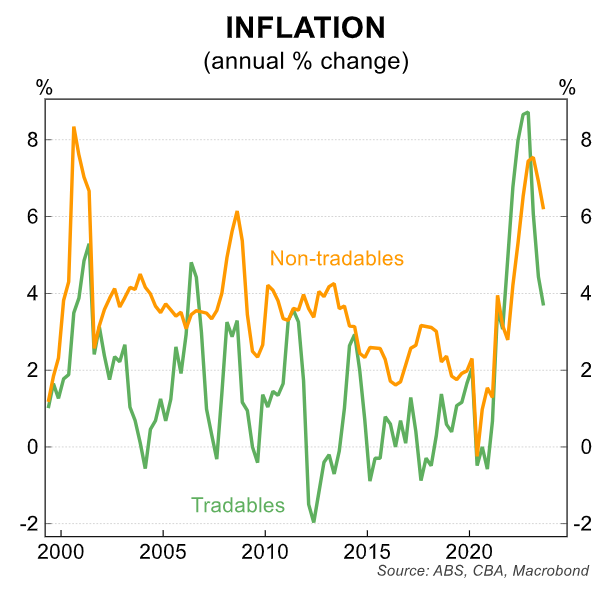

Goods prices rose by 1.2%/qtr, with the annual rate decelerating to 4.9%/yr. That was a slower-than-expected pace of disinflation.

That mainly reflected stronger fuel, new dwelling construction, motor vehicle, and water & gas price rises.

Services prices rose by 1.0%/qtr, and the annual rate stepped down to 5.8%/yr, from 6.3%/yr previously. While broadly in line with our forecast, this reflected offsetting factors.

Stronger-than-expected rises in several services items were offset by slightly softer rents and education inflation, which were depressed by government policies.

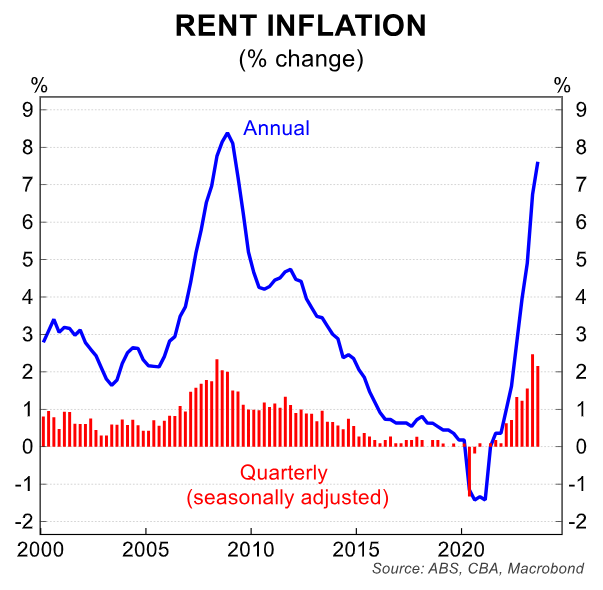

As has been the case for some time, the Housing component of the CPI basket remained the largest contributor (+0.47ppts) to the rise in inflation.

Increases in both rents (+2.2%/qtr) and new dwelling construction costs (+1.3%/qtr) contributed around a quarter point to quarterly inflation.

Rents are rising strongly because of low rental vacancy rates. The slight decline in the pace of rental increase was due to changes to Commonwealth Rental Assistance (CRA). The CRA increased rent assistance by 15% and affects around 1 million households and began on 20 September.

Absent this, rents would have lifted by 2.5%, a further acceleration.

New dwelling construction costs increased (+1.3%/qtr). The ABS notes that builders continue to pass on labour and material costs.

But there were also large price rises for property rates & charges (+4.4%/qtr), which saw the biggest price rise in eight years. And various utilities prices also experienced large increases.

The well-document increase in electricity prices was broadly as expected. Government rebates are working to reduce the extent of price rises, and we expect this to continue into the December quarter.

Water & sewerage rose by more than expected (+4.7%/qtr), as did gas & other household fuels (+1.4%/qtr).

Higher operating costs and wholesale prices for utilities are being passed onto consumers.

The Transport group in the CPI was the next largest contributor to quarterly inflation. The significant rise in automotive fuel (+7.2%/qtr) alone contributed a quarter point to inflation.

Recent supply shocks have seen global oil prices rise. The RBA’s current forecasts are underpinned by a technical assumption of Brent oil at $US80/bbl; this will likely need to be updated in light of these global developments.

Motor vehicle prices rose by 0.5%/qtr, reversing the decline experienced in the June quarter. Services relating to motor vehicles increased sharply (+3.2%/qtr) owing to higher fees and charges, and the sharpest rise since 2014.

Insurance & financial services inflation (+1.4%/qtr) was roughly in line with our expectations. The largest driver was insurance (home & home contents and motor vehicles, +2.8%/qtr) and we saw an expected moderation in financial services inflation (+0.8%/qtr).

Communications prices rose by 2.1%/qtr, driven by a sharp 1.9%/qtr rise in telecommunications equipment & services. While only a fairly small component of the CPI basket, this has been a source of deflation in the years leading up to the pandemic. But price rises for mobile and internet plans have contributed to the largest quarter increase since 2000.

Recreation & culture inflation rose to 0.2%/qtr. Many of the services components of this group saw elevated inflation pressures.

‘Other recreational, sporting & cultural services’ were up by 3.4%/qtr. And vet services rose by 2.4%/qtr. Offsetting strength in these services inflation was a quarterly decline in domestic travel & accommodation prices (-2.5%/qtr).

But international travel & accommodation rose slightly (+0.5%/qtr). Prices for both domestic and international travel remain very elevated and was stronger in September.

Furnishings, household equipment & services (-0.8%/qtr) fell by less than expected. That was driven by a smaller decline in childcare prices than we had expected.

Childcare prices fell by 13.2%/qtr, smaller than the 20% decline we expected. Large fee increases meant that the increase in the childcare subsidy had a smaller impact on families out-of-pocket costs.

Food and alcohol in the CPI basket were broadly as expected. Food & non-alcoholic beverages prices rose by 0.6%/qtr.

There were welcome price declines in red meat, and in fresh fruit & vegetables. Dairy continued to experience strong price rises.

And, as seen in the August CPI indicator, restaurant meals and take away food saw a solid 2.1%/qtr rise.

Alcohol & tobacco price rises (+1.4%/qtr) were generally as expected, as the increase in taxes flowed through to consumer prices.

And clothing & footwear (+0.4%/qtr) saw some softness owing to discounting activity by retailers.