By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Our central scenario has the RBA on hold from here and we continue to look for an easing cycle to commence in mid-2024.

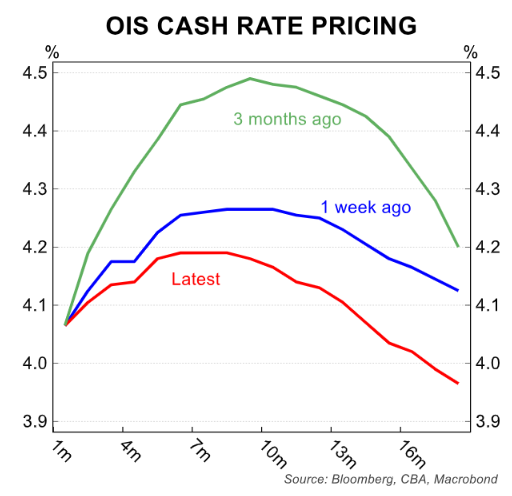

- But there is a clear near-term risk that the RBA delivers on its long-held hiking bias and increases the cash rate by 25bp at either the November or December Board meetings (we assess the probability of rate hikes at both meetings to be low).

- There are three key data releases for markets before the Melbourne Cup day Board meeting: September labour force survey (19/10), Q3 23 CPI(25/10) and September retail trade (30/10). The inflation report is the most important of these economic publications.

- Our preliminary forecast for the Q3 23CPI is broadly similar to the RBA’s implied profile. We believe this is consistent with monetary policy on hold in November.

- But the monthly CPI indicator means there is upside risk to our Q323 CPI forecast. As such, we currently consider the November Board meeting to be ‘live’.

The RBA’s reaction function has not changed:

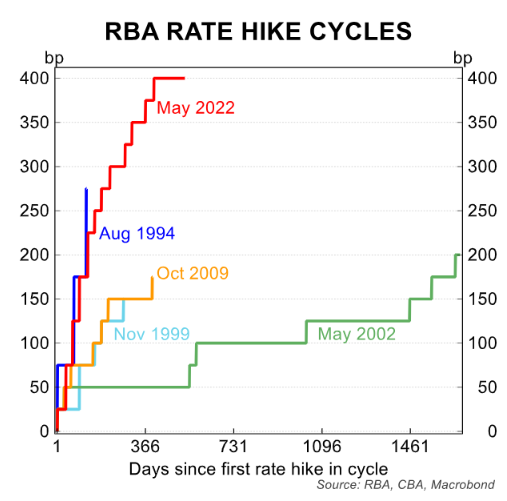

The RBA left the cash rate on hold at the last four monthly Board meetings. Recall that the last move in the cash rate was a 25bp increase in June, which took the cash rate target to 4.10%.

The forward guidance from the RBA since the last rate increase has been clear and consistent – “some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks.”

Indeed that message was not modified or tweaked in October, despite the change of RBA Governor. New Governor Michele Bullock had the opportunity to alter the language and tone in her Statement accompanying the on-hold decision in October.

But instead the Governor made minimal changes to the Statement that accompanied the September Board meeting –former Governor Philip Lowe’s last one.

The decision not to shift the language in the statement accompanying the October Board decision was significant. It sent a clear signal to markets that the RBA’s reaction function and forward guidance has not changed under the new Governor.

Our take on the RBA’s forward guidance is straight forward. The Board is willing to raise the cash rate again in this cycle. But another rate increase would require the economic data, particularly around inflation, consumer spending and the labour market, to come in stronger than the RBA’s forecasts.

Our base case for policy to remain on hold from here is premised largely on one assumption. Namely that the RBA will not pull the rate hike trigger again provided they remain confident that inflation will return to target by late 2025 without further tightening.

That confidence could be tested in the wake of the upcoming Q3 23 CPI. As such, we currently categorise the November Board meeting as ‘live’.

All eyes on the Q3 23 CPI:

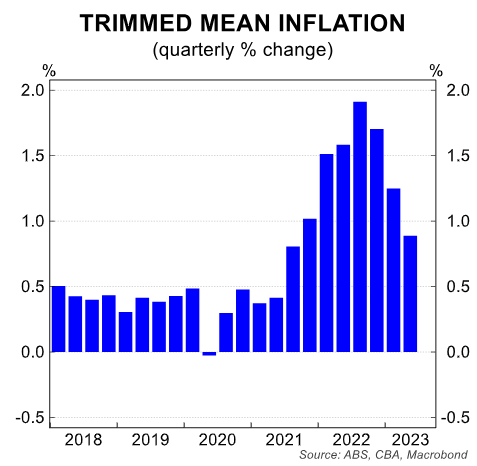

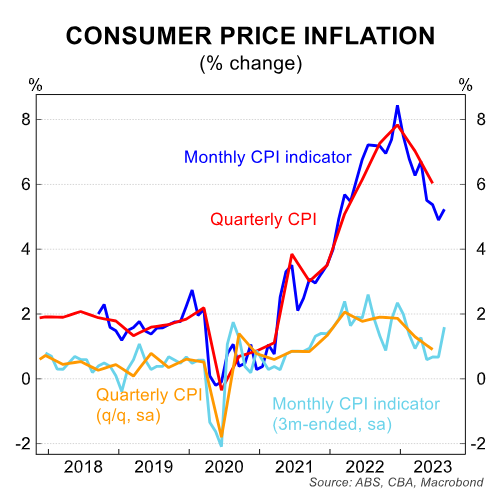

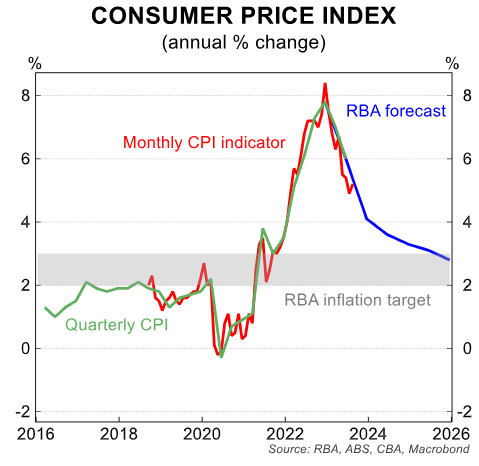

The August monthly CPI indicator means we think the balance of risks sit with a Q3 23 trimmed mean outcome that is stronger than the RBA’s implied profile.

The RBA’s inflation forecasts in the August Statement on Monetary Policy (SMP) suggest the central bank expects the Q3 23 trimmed mean CPI to be ~0.9%/qtr (4.8%/yr).

It is possible the RBA’s forecasters have upwardly revised their Q3 23 trimmed mean CPI estimate following the August monthly CPI data. But we can’t be sure.

Certainly there was no indication in the Governor’s Statement last week that the Bank has changed their assessment on the outlook for inflation. Indeed there was no explicit mention of the August monthly CPI in the Statement.

Our preliminary forecast for the Q3 23 trimmed mean CPI is ~1.0%/qtr (4.9%/yr). This is a touch above the RBA’s forecast. In isolation this is an outcome that could likely cause the RBA some discomfort.

But the read on headline inflation also matters. We forecast the headline Q3 23 CPI to print a touch below the RBA’s forecast from the August SMP (CBA +0.9%/qtr and 5.1%/yr compared to the RBA’s forecast of 1.0%/qtr and 5.2%/yr).

If headline inflation prints a little lower than the RBA forecast and underlying a touch firmer the Board would likely leave policy on hold in November. But the decision would be finely balanced.

Other data on the economy released over the month of October would feed into policy deliberations.

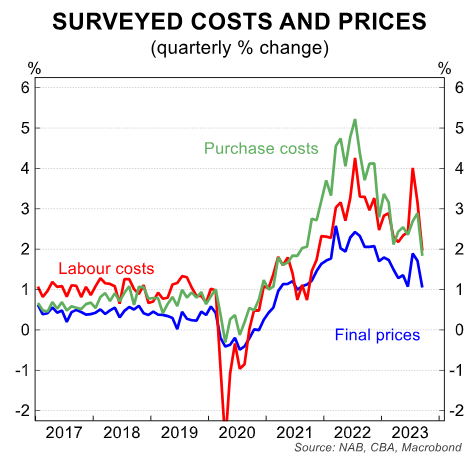

Earlier this week the September NAB Business Survey was published. It contained a welcome set of gauges on input and output prices, as well as labour costs. The gauges all moved down, the desired direction at this juncture.

But the inflation data from our official statistician, the ABS, always trumps the business survey data. That is why markets will be firmly focused on the quarterly inflation report, which prints on Wednesday 25 October.

The risk to our Q3 23 CPI inflation forecasts are to the upside. As such, we put the probability of a November rate increase at this stage at around 40%.

The tightening cycle may not be over despite monetary policy being left on hold at each of the last four meetings.

Other near term data to watch:

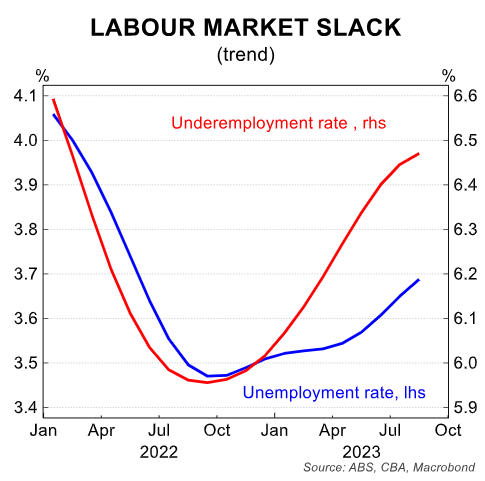

The September employment report is due on Thursday 19 October. The RBA sees a further loosening in the labour market as a necessary condition for inflation to return to target by late 2025.

Most economists would agree that the key barometer of tightness in the labour market is the unemployment rate. And the RBA subscribes to this view.

The trend unemployment rate has edged up over the past year, but only very modestly. For context, the trend unemployment rate rose by 0.2ppts over the year to be 3.7% in August.

We have been surprised that the jobless rate has not moved a little higher given the decline in real consumer spending per capita. But other indicators of the labour market have softened more in line with our expectations.

Job vacancies continue to trend lower. And according to Seek the number of applicants per job advertisement is higher than its pre-pandemic average:

The underemployment rate has also increased by more than the lift in the unemployment rate:

So underutilisation, the broadest measure of labour market slack, has increased by more than the lift in the unemployment rate.

Underutilisation has had a stronger correlation with wages outcomes compared to the unemployment rate over the past two decades. We consider it an important metric to monitor.

Measures of labour market slack in the upcoming labour force survey are the ones to watch from a monetary policy perspective. The RBA Board will put less weight on the change in employment.

Finally September retail trade prints on Monday 30 October. At that point market, analysts will have firmed up their November rate hike call. And it would take a brave forecaster to shift their RBA call at the eleventh hour.

In any event, there is only a small chance that the retail trade data would shift the dial one way or the other. That said, if the other already published data leaves the November Board meeting in coin toss territory, a rouge retail trade report (either strong or weak) may not be discounted by markets.

Our internal data suggests retail trade was buoyant in September.

The RBA will continue to forecast inflation back to target by end 2025

The RBA’s forecast from the August SMP is for the annual rate of headline inflation to return to the target band by late 2025 (Q4 25 forecast at 2.8%). The trimmed mean CPI is forecast to be within target by mid-25 (Q2 25 forecast at 2.9%).

It is worth noting here that whilst the trimmed mean is the RBA’s preferred measure of inflation, the inflation target is headline CPI.

The RBA have stated that, “the central forecast is for CPI inflation to continue to decline and to be back within the 2–3 per cent target range in late 2025.”

The RBA is willing to take a little longer than other central banks to return inflation to the target band to preserve as many of the gains in the labour market as is possible. But they are not willing to let inflation sit above the target band for too long.

We expect inflation to recede more quickly than the RBA. But what we forecast for inflation over coming years does not matter for the November Board meeting.

The RBA Board will not accept leaving the policy rate at its current level if the Q3 23 CPI casts sufficient doubt in their minds that inflation will return to target by late 2025 (note that we expect it to be back within the target band by H2 24).

We expect the RBA will retain its central scenario that inflation will return to the target band in late 2025 following the November Board meeting irrespective of an upside surprise in the upcoming inflation report.

This may seem an odd statement to make. But it’s always important to remember that policymakers can shape economic outcomes. The actions of the RBA influence their forecasts.

The RBA’s job is to use monetary policy to manage demand in the economy and by extension inflation.

In short, the RBA will hike the cash rate in November if the Board believes a rate increase is necessary to forecast a central scenario for inflation to return to the target band by late 2025.

As such, we currently assess the November Board meeting as ‘live’.

Concluding thoughts on population growth and inflation

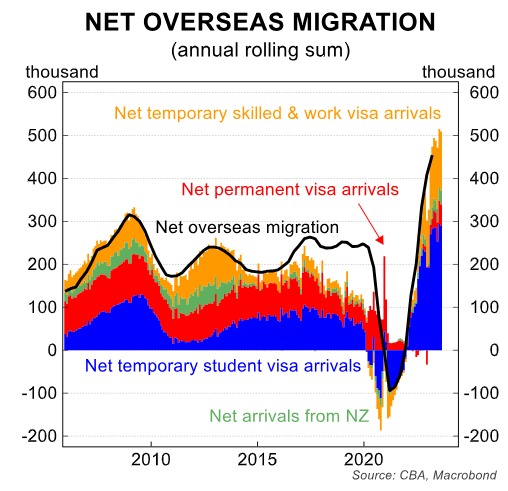

The surge in Australia’s population over the past year has been extraordinary. It has been significantly stronger than the Government forecast.

For context, Australia’s population jumped by 0.7%/qtr in Q1 23. And growth in the working age population from the labour force survey was 2.8%/yr in September.

The facing chart highlights the massive recent lift in the population compared to pre-pandemic levels. The surge in population growth has boosted aggregate demand in the economy.

In turn this has somewhat masked the per capita decline in real consumer spending.

More importantly from a monetary policy perspective, there are implications for inflation. Higher than expected immigration is alleviating wage pressures in some industries that had been experiencing significant labour shortages.

In turn that should dampen inflation outcomes over the medium term as growth in input costs slow (labour is a key input in the cost of production, particularly in the services sector).

But in the short run we believe the rapid increase in population contributes to a firmer inflationary pulse. The RBA shares this view, albeit they have not commented a lot about it more recently.

The stronger than expected lift in the population was apparent in the arrivals data earlier this year. And the RBA first mentioned the link between population growth and inflation in the April Board Minutes.

Specifically it was stated that, “members noted that the net effect of a sudden surge in population growth could be somewhat inflationary for a period.”

Since then population growth has continued to be stronger than both the Government and the RBA expected, particularly since the May 2023 Budget.

Indeed we could not foresee the extraordinary lift in the population occurring either. Our methodology has always been to simply use the Government’s population projections as an underpinning assumption in our economic forecasts.

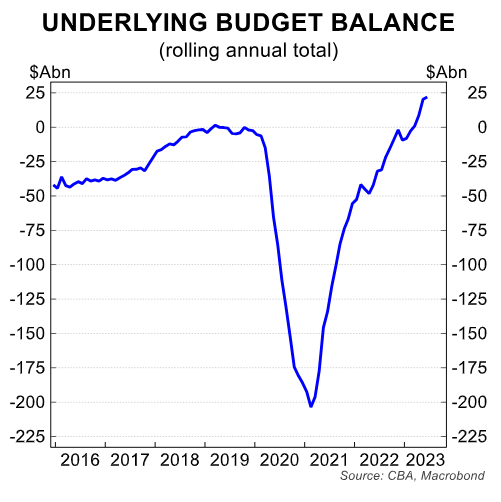

Fiscal and monetary policy are broadly working in tandem in Australia when assessing the stance of fiscal policy from a budgetary perspective.

In 2022/23, the Australian Government recorded an underlying cash surplus of $A22.1 billion (0.9% of GDP). The news was good.

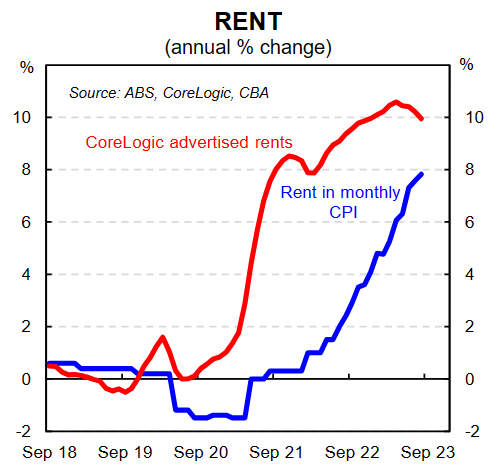

But the massive lift in population has contributed to a greater increase in some components of the CPI basket than would have otherwise been the case–particularly rents, which have risen very significantly over the past year.

There is a risk that the tightening cycle is extended if Australia’s population continues to swell at its current rate.

In addition, it could mean interest rates stay higher for longer, which delays the start of an easing cycle.