By Gareth Aird, head of Australian economics at CBA:

Key Points:

- We have upwardly revised our near-term inflation forecasts and by extension modified our profile for the RBA cash rate following the Q3 23CPI.

- As noted on Wednesday, we now expect the RBA to take monetary policy further into restrictive territory with a 25bp rate hike at the November Board meeting, which would take the cash rate to 4.35%.

- Our base case sees the RBA hold the cash rate at 4.35% until Q3 24, when we look for an easing cycle to commence.

- Monetary policy is unlikely to return to a more neutral setting until mid-2025 (we see the cash rate at ~2.85% by mid-2025).

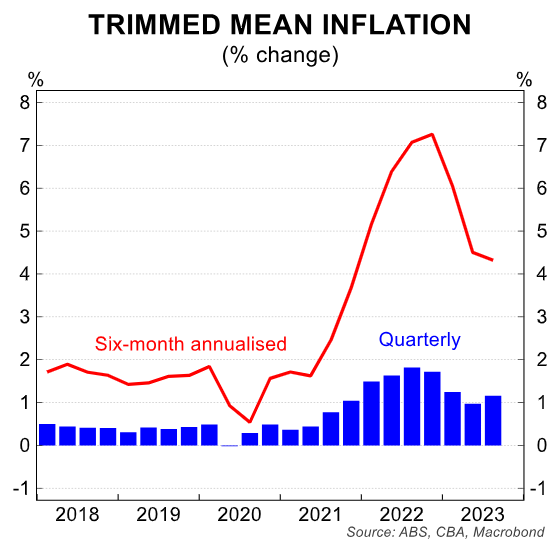

Both the headline and underlying Q3 23 CPI came in firmer than our forecast and market expectations.

The September quarter inflation report was also stronger than the RBA forecasts from the August Statement on Monetary Policy (SMP).

As a result, we shifted our call for the upcoming November Board meeting from ‘on hold’ to a 25bp rate hike, taking the cash rate to 4.35%.

Regular readers will note that prior to the inflation print we were very much open to the idea that the RBA would hike the cash rate in November. And we had ascribed a 40% chance to a rate increase. We now put the probability of a 25bp rate increase on Melbourne Cup day at 70%.

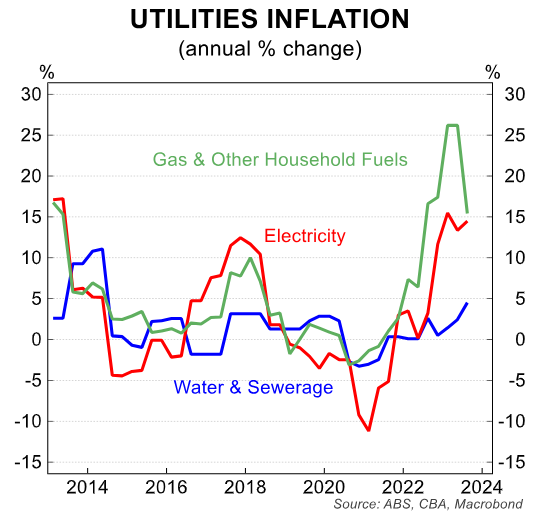

There are many components of the CPI basket that are running hot, but are largely beyond the control of the RBA. In particular, strong price rises for petrol, rent and utilities cannot be muted by a higher cash rate.

This means monetary policy must run harder against the components of the CPI basket that it more directly influences.

The upshot is that the cash rate is likely to stay at a restrictive level for longer to pull inflation down to the desired level.

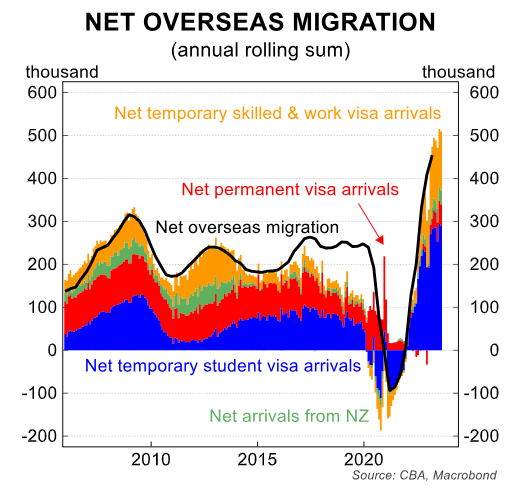

We have upwardly revised our near-term inflation forecasts. The changes incorporate the latest inflation print and stronger than anticipated population growth.

The big lift in net overseas migration is alleviating wage pressures in some industries that had been experiencing significant labour shortages. But it is also putting upward pressure on some components of the CPI basket.

In the April RBA Board Minutes earlier this year it was noted that, “the net effect of a sudden surge in population growth could be somewhat inflationary for a period.” The latest inflation report indicates the observation from the April Board Minutes was correct.

A surge in rental inflation, in particular, is directly related to the supply and demand mismatch for housing. Residential construction has not kept pace with population growth.

As a result, vacancy rates sit at record lows across many parts of the country and this is putting upward pressure on rents.

We do not see that situation changing in the near term as population growth shows no signs of abating.

We forecast the annual rate of headline inflation to be 4.3% in Q4 23 and 3.0% in Q4 24. The annual rate of trimmed mean inflation is expected to be 4.4% in Q4 23 and 2.9% in Q4 24.

Our inflation forecasts incorporate a revised profile for the cash rate. Our base case looks for a peak in the cash rate of 4.35% (to be achieved at the upcoming November Board meeting). We see policy remaining at that level until September 2024, when we have pencilled in the start of an easing cycle.

The RBA Board meeting schedule shifts from 11 meetings a year to 8 meetings a year from 2024. There is a Board meeting scheduled for 23-24 September.

At this meeting the Board will have the June quarter 2024 CPI, WPI and national accounts as well as the August labour force survey. Our base case is that there will be sufficient evidence in this slew of data for the RBA to commence an easing cycle.

Note that we don’t expect the annual rate of inflation to be back to the RBA’s target band by the September 2024 Board meeting. But at that point we think that the Board will assess the pulse of underlying inflation on a six-month annualised basis.

Our base case looks for 75bp of easing in late 2024 for an end year cash rate of 3.60% (25bp rate cuts in September, November and December).

We have a further 75bp of easing pencilled in over H1 2025 (February, March and May), which would take the cash rate to 2.85%.

In February 2023, then RBA Governor Lowe stated that monetary policy was restrictive. At the time the cash rate was 3.35%. Therefore an expected peak in the cash rate of 4.35% is at least 100bp in restrictive territory based on former Governor Lowe’s remarks.

On that basis, policy remains in restrictive territory on our forecast profile for the cash rate until 2025.

Risks

There are a lot of moving parts to the economic landscape at present, which adds to uncertainty around the economic outlook and the path of monetary policy.

In the near term, the balance of risks sits with a higher terminal cash rate than 4.35%. If the Board raises the cash rate to 4.35% in November, as we expect, then we would anticipate they retain their hiking bias. This means any further upside surprises to the inflation outlook could see the RBA pull the rate hike trigger again.

Looking further out the risks become more evenly balanced.

If population growth remains elevated or consumption strengthens due to rising home prices, it could make the RBA’s job of returning inflation to target more difficult. In such a scenario, the cash rate may sit at its peak in the cycle for longer than we currently anticipate.

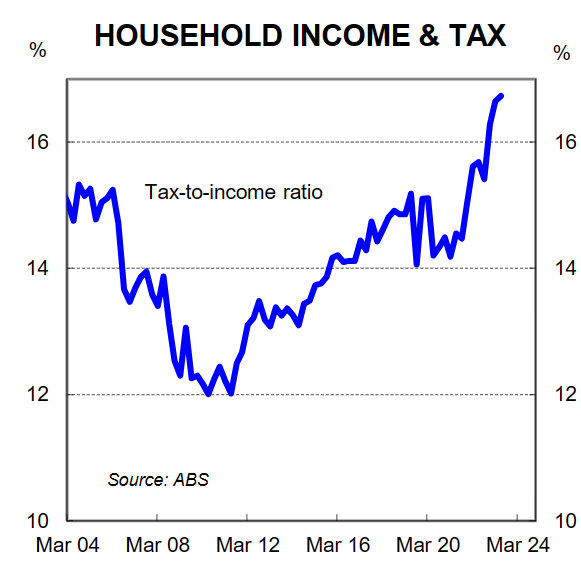

Fiscal policy is also a key source of uncertainty. Any loosening in fiscal policy at either the state or federal level would put upward pressure on demand and by extension inflation (note that the already legislated 2024 income tax cuts will provide some stimulus to the economy over 2024/25. But the tax cuts are simply reducing bracket creep given the personal tax-to-income ratio has surged over the past decade – see below chart).

Geopolitical uncertainty is also an upside risk to the inflation and rates outlook.

Working the other way is the risk that the lagged impact of interest rate increases weighs more heavily on the consumer in 2024. There is still a lot of organic tightening to come via the ongoing expiry of ultra-low fixed rate loans. And the expected 25bp rate hike next month won’t flow through to higher mortgage repayments for variable-rate borrowers until February next year.

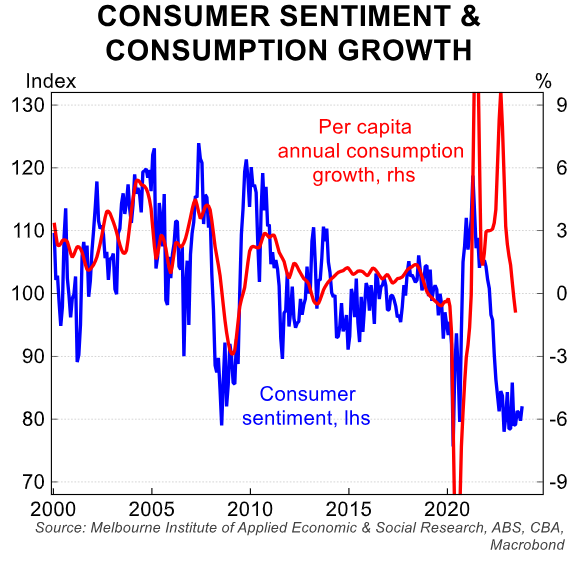

It may be the case that consumer behaviour through next year more closely marries up with how the household sector is feeling. To date, the usual relationship between consumer sentiment and behaviour has not been aligned (see next chart).

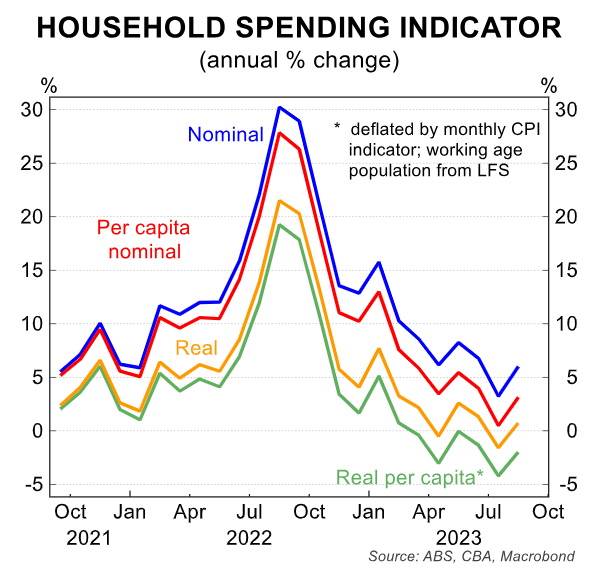

But there is a risk the typical relationship reasserts itself next year and spending slows more quickly. The CommBank Household Spending Insights (HSI) index will be an important source of information on consumer spending activity.

In the near-term the key domestic data to watch from a monetary policy perspective relates to consumer spending, the labour market, prices and wages. The ABS will release September retail trade next week (30/10). Our internal data points to a solid print (we forecast a 0.8% lift in retail sales over September). That is the last major data point before the November Board meeting.

We will publish a full RBA preview next week ahead of the November Board meeting.